Swiss banks are renowned for their robust capital allocation strategies, which are designed to balance profitability, risk management, and regulatory compliance. These institutions allocate capital across a diverse portfolio of assets, including traditional banking activities such as loans and mortgages, investment banking operations, and wealth management services. A significant portion of their capital is directed toward low-risk, high-liquidity assets like government bonds and cash reserves, ensuring stability and compliance with stringent Swiss and international banking regulations. Additionally, Swiss banks invest in innovative financial products and technologies to maintain their competitive edge in the global market, while also setting aside substantial capital for contingency planning and risk mitigation. This disciplined approach to capital allocation underscores their reputation for financial security and prudence.

Explore related products

What You'll Learn

- Core Tier 1 Capital Allocation: Swiss banks prioritize capital for risk-weighted assets, ensuring regulatory compliance and financial stability

- Loan Portfolio Investments: Capital is allocated to mortgages, corporate loans, and personal lending, driving economic growth

- Treasury and Trading Activities: Funds support bond trading, currency exchange, and proprietary investments for profit generation

- Operational Risk Management: Capital buffers are maintained to cover operational risks, fraud, and compliance failures

- Digital Transformation Funding: Investments in fintech, cybersecurity, and digital banking infrastructure enhance competitiveness and efficiency

![]()

Core Tier 1 Capital Allocation: Swiss banks prioritize capital for risk-weighted assets, ensuring regulatory compliance and financial stability

Swiss banks are renowned for their meticulous approach to capital allocation, particularly when it comes to Core Tier 1 Capital. This high-quality capital, primarily composed of common equity and retained earnings, serves as the bedrock of a bank's financial resilience. At the heart of their strategy lies a focus on risk-weighted assets (RWAs), a critical metric that quantifies the capital required to absorb potential losses from various banking activities. By prioritizing capital for RWAs, Swiss banks not only adhere to stringent regulatory requirements but also fortify their financial stability in an increasingly volatile global market.

Consider the Basel III framework, which mandates that banks maintain a minimum Core Tier 1 capital ratio of 4.5% of RWAs, with an additional 2.5% buffer for systemically important banks. Swiss regulators often impose even stricter standards, reflecting the country’s commitment to financial prudence. For instance, UBS and Credit Suisse, two of Switzerland’s largest banks, consistently maintain Core Tier 1 ratios above 13%, significantly exceeding regulatory minima. This conservative approach ensures that capital is allocated to cover potential risks from loans, investments, and other assets, weighted according to their inherent risk profiles. A mortgage, for example, might carry a lower risk weight (e.g., 35%) compared to corporate loans (100%) or derivatives (higher multiples), guiding banks to allocate capital proportionally.

The allocation process is both art and science, requiring banks to balance profitability with risk management. Swiss banks employ sophisticated models to assess RWAs, factoring in macroeconomic trends, credit quality, and market volatility. For instance, during the 2008 financial crisis, Swiss banks’ robust capital buffers allowed them to weather the storm better than many peers. Today, with rising interest rates and geopolitical uncertainties, banks are further stress-testing their portfolios to ensure capital is adequately allocated to higher-risk assets. This proactive stance not only safeguards the banks but also protects depositors and investors, reinforcing Switzerland’s reputation as a global financial safe haven.

A practical takeaway for financial institutions is to emulate Swiss banks’ disciplined approach to Core Tier 1 capital allocation. Start by conducting a thorough risk assessment of your asset portfolio, assigning appropriate weights based on Basel guidelines or local regulations. Regularly update these weights to reflect changing market conditions. Next, establish a capital buffer above regulatory minima to absorb unexpected shocks. Finally, invest in advanced risk modeling tools to enhance the accuracy of your RWA calculations. By prioritizing risk-weighted assets in capital allocation, banks can achieve both regulatory compliance and long-term financial stability, lessons Swiss banks have mastered over decades.

How Long Does It Take to Bank a Cheque in New Zealand?

You may want to see also

Explore related products

![]()

Loan Portfolio Investments: Capital is allocated to mortgages, corporate loans, and personal lending, driving economic growth

Swiss banks, renowned for their stability and discretion, strategically allocate capital to loan portfolio investments, a cornerstone of their operations. This allocation fuels economic growth by channeling funds into mortgages, corporate loans, and personal lending. Each category serves distinct purposes, catering to diverse borrower needs while generating returns for the bank.

Mortgages, a significant portion of Swiss bank loan portfolios, provide long-term financing for individuals and families to purchase homes. This not only fulfills a fundamental societal need but also stimulates the construction and real estate sectors, creating jobs and driving economic activity. Swiss banks meticulously assess borrower creditworthiness and property value to mitigate risk while ensuring responsible lending practices.

Corporate loans form another vital component, enabling businesses to expand operations, invest in innovation, and navigate economic cycles. Swiss banks tailor loan structures to meet specific corporate needs, whether for working capital, equipment purchases, or mergers and acquisitions. By supporting businesses, banks contribute to job creation, technological advancement, and overall economic productivity.

Personal lending, encompassing credit cards, auto loans, and personal lines of credit, empowers individuals to manage expenses, pursue education, or consolidate debt. While smaller in scale compared to mortgages and corporate loans, personal lending plays a crucial role in consumer spending and financial inclusion. Swiss banks employ rigorous risk assessment models to ensure responsible borrowing and minimize defaults.

The allocation of capital to loan portfolios is a delicate balance between risk and reward. Swiss banks leverage sophisticated risk management frameworks, leveraging data analytics and economic forecasting to optimize portfolio performance. This strategic approach ensures sustainable growth, safeguards depositor funds, and maintains the banks' reputation for financial stability. By effectively managing loan portfolios, Swiss banks not only generate profits but also act as catalysts for economic development, fostering prosperity for individuals, businesses, and the nation as a whole.

Vinton County Bank Login Issues: What’s Happening and How to Fix

You may want to see also

Explore related products

![]()

Treasury and Trading Activities: Funds support bond trading, currency exchange, and proprietary investments for profit generation

Swiss banks, renowned for their precision and discretion, allocate a significant portion of their capital to treasury and trading activities. These operations are not merely ancillary functions but core strategies for profit generation and risk management. By deploying funds in bond trading, currency exchange, and proprietary investments, these institutions leverage market dynamics to enhance returns while maintaining liquidity and stability. This approach underscores the dual mandate of Swiss banks: to safeguard client assets and to capitalize on financial opportunities.

Consider bond trading, a cornerstone of treasury activities. Swiss banks actively participate in both government and corporate bond markets, exploiting yield differentials and interest rate fluctuations. For instance, during periods of economic uncertainty, they may increase holdings in Swiss government bonds (known as Swiss Confederation Bonds) for their safety and stability. Conversely, in bullish markets, they might shift towards higher-yielding corporate bonds to maximize returns. This strategic allocation requires a deep understanding of macroeconomic trends and a nimble response to market shifts, ensuring that capital is deployed efficiently.

Currency exchange is another critical area where Swiss banks allocate capital. Switzerland’s status as a global financial hub, coupled with the Swiss franc’s reputation as a safe-haven currency, positions its banks uniquely in the foreign exchange (FX) market. They engage in spot, forward, and swap transactions, often acting as intermediaries for multinational corporations and institutional clients. Proprietary trading desks further amplify profits by speculating on currency movements, such as the EUR/CHF or USD/CHF pairs. However, this activity is tightly regulated to mitigate risks, with banks adhering to strict capital adequacy ratios under Basel III guidelines.

Proprietary investments represent the most aggressive yet potentially lucrative aspect of treasury and trading activities. Swiss banks allocate capital to proprietary trading desks, which operate independently to pursue profit-making opportunities across asset classes, including equities, commodities, and derivatives. For example, a bank might invest in structured products tied to the performance of the Swiss Market Index (SMI) or hedge against inflation by trading gold futures. While these activities carry higher risks, they are balanced by robust risk management frameworks, including value-at-risk (VaR) models and stress testing.

The takeaway is clear: treasury and trading activities are not just ancillary functions for Swiss banks but strategic imperatives. By allocating capital to bond trading, currency exchange, and proprietary investments, these institutions navigate complex financial markets to generate profits while maintaining stability. This dual focus on safety and opportunity reflects the Swiss banking ethos, blending conservatism with innovation. For investors and clients, understanding these activities provides insight into how Swiss banks create value, even in volatile market conditions.

Step-by-Step Guide to Perform NEFT Transactions Offline at Your Bank

You may want to see also

Explore related products

![]()

Operational Risk Management: Capital buffers are maintained to cover operational risks, fraud, and compliance failures

Swiss banks, renowned for their stability and prudence, allocate a significant portion of their capital to operational risk management. This strategic move is not merely a regulatory requirement but a cornerstone of their risk mitigation strategy. Capital buffers, specifically earmarked for operational risks, act as a financial safety net, absorbing the impact of unforeseen events such as fraud, system failures, or compliance breaches. These buffers are calibrated based on historical loss data, stress testing scenarios, and forward-looking risk assessments, ensuring that the bank remains resilient even in the face of severe operational disruptions.

Consider the practical implementation of these capital buffers. For instance, a Swiss bank might allocate 10-15% of its total capital to operational risk, a figure derived from Basel III guidelines and tailored to its risk profile. This allocation is not static; it is dynamically adjusted based on emerging risks, such as cybersecurity threats or geopolitical instability. Banks employ sophisticated models to quantify operational risk exposure, often using advanced analytics to identify vulnerabilities in their processes, technology, and human resources. By doing so, they not only comply with regulatory standards but also enhance their ability to protect shareholder value and maintain customer trust.

A critical aspect of operational risk management is the integration of fraud prevention and compliance frameworks. Swiss banks invest heavily in anti-fraud technologies, such as AI-driven transaction monitoring systems and biometric authentication tools, to detect and prevent fraudulent activities in real time. Compliance failures, often stemming from regulatory changes or internal oversight lapses, are mitigated through robust governance structures and continuous training programs. For example, a bank might conduct quarterly compliance audits and mandate annual certifications for employees to ensure adherence to both local and international regulations. These measures, combined with the capital buffer, create a multi-layered defense mechanism against operational risks.

However, maintaining capital buffers for operational risks is not without challenges. One of the key dilemmas is balancing the need for sufficient capital with the pressure to optimize returns on equity. Excessive capital allocation can hinder profitability, while insufficient reserves expose the bank to catastrophic losses. To address this, Swiss banks often adopt a tiered approach, prioritizing risks based on their potential impact and likelihood. High-impact risks, such as a major IT outage or a large-scale fraud scheme, are allocated larger portions of the buffer, while lower-impact risks are managed through operational improvements and insurance.

In conclusion, the allocation of capital for operational risk management in Swiss banks is a strategic imperative, not just a regulatory obligation. By maintaining robust capital buffers, investing in advanced risk mitigation technologies, and fostering a culture of compliance, these institutions safeguard their financial health and reputation. For other banks looking to emulate this model, the key takeaways are clear: adopt a data-driven approach to risk assessment, integrate fraud and compliance frameworks seamlessly, and strike a balance between capital preservation and profitability. This holistic approach ensures not only survival but also sustained growth in an increasingly complex and volatile financial landscape.

Seed Banks in California: Where to Find Them?

You may want to see also

Explore related products

![]()

Digital Transformation Funding: Investments in fintech, cybersecurity, and digital banking infrastructure enhance competitiveness and efficiency

Swiss banks are increasingly allocating capital to digital transformation initiatives, recognizing that investments in fintech, cybersecurity, and digital banking infrastructure are no longer optional but essential for survival in a rapidly evolving financial landscape. This strategic shift is driven by the need to enhance competitiveness, improve operational efficiency, and meet the growing demands of tech-savvy customers. By leveraging cutting-edge technologies, Swiss banks aim to streamline processes, reduce costs, and deliver seamless, secure, and personalized banking experiences.

One of the key areas of focus is fintech investments, where Swiss banks are partnering with or acquiring innovative startups to integrate advanced solutions such as AI-driven advisory services, blockchain-based transactions, and open banking platforms. For instance, UBS and Credit Suisse have both launched fintech accelerators to scout and nurture promising technologies. These initiatives not only foster innovation but also enable banks to stay ahead of disruptors. A practical tip for banks considering fintech investments is to prioritize solutions that align with their core business goals, such as improving customer engagement or optimizing risk management, rather than adopting technologies for the sake of innovation alone.

Cybersecurity is another critical component of digital transformation funding. As cyber threats become more sophisticated, Swiss banks are allocating significant resources to fortify their digital defenses. This includes investing in advanced encryption technologies, threat intelligence platforms, and employee training programs. For example, Zurich-based banks have reported allocating up to 20% of their IT budgets to cybersecurity measures. A cautionary note: while investing in cybersecurity is non-negotiable, banks must balance robust protection with user experience to avoid overly complex authentication processes that could deter customers.

The development of digital banking infrastructure is equally vital. Swiss banks are modernizing their core systems to support real-time transactions, mobile banking, and omnichannel integration. For instance, PostFinance has invested heavily in cloud-based infrastructure to enhance scalability and flexibility. Banks should approach this by adopting a phased implementation strategy, starting with high-impact areas like mobile app enhancements, followed by backend system upgrades. This ensures minimal disruption while delivering immediate value to customers.

In conclusion, the allocation of capital to digital transformation is a strategic imperative for Swiss banks. By investing in fintech, cybersecurity, and digital banking infrastructure, they not only future-proof their operations but also position themselves as leaders in a highly competitive market. The key takeaway is that these investments must be purposeful, balanced, and aligned with both customer needs and long-term business objectives. As the financial industry continues to evolve, Swiss banks that embrace digital transformation will be best equipped to thrive in the new era of banking.

Cheque Expiry: Do Bank Cheques Have a Shelf Life?

You may want to see also

Frequently asked questions

Swiss banks allocate their capital primarily to traditional banking activities such as lending, wealth management, and investment services. They also invest in treasury operations, trading activities, and maintain reserves to meet regulatory requirements.

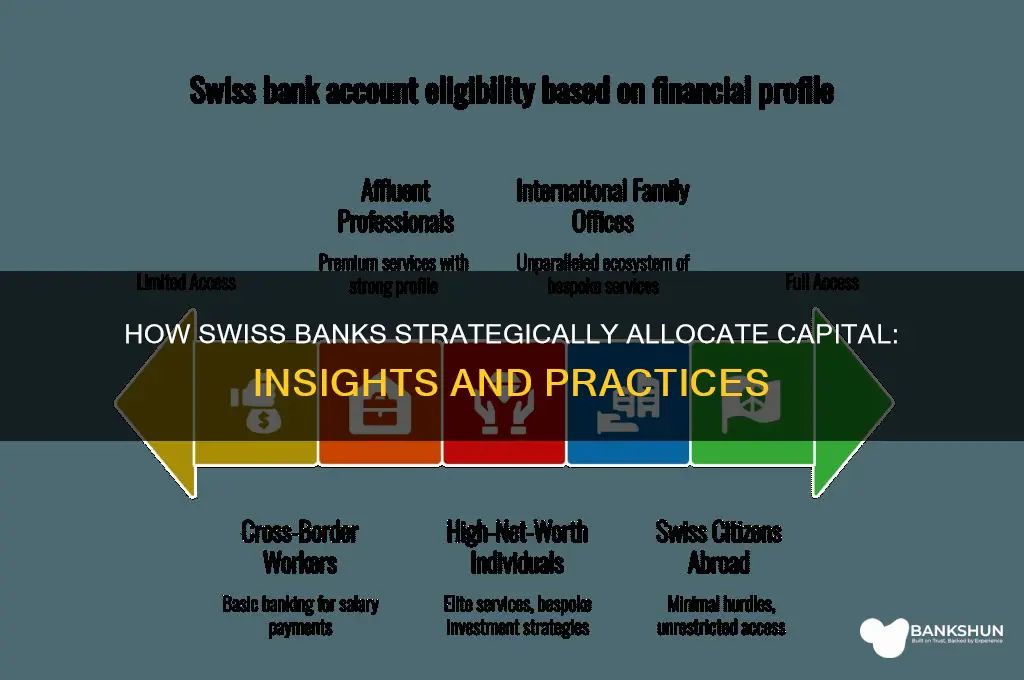

A: Yes, Swiss banks allocate a significant portion of their capital to international markets, particularly in wealth management, private banking, and cross-border financial services. They leverage Switzerland’s reputation as a global financial hub to serve clients worldwide.

A: Swiss banks allocate capital for risk management by maintaining robust reserves, investing in advanced risk assessment tools, and adhering to strict regulatory frameworks like Basel III. This ensures financial stability and protects against potential losses.