Investors at banks are commonly referred to as depositors or account holders when they place funds in savings, checking, or certificate of deposit (CD) accounts, as these individuals are essentially lending money to the bank in exchange for interest. However, when discussing investors in the context of bank ownership or equity, they are often called shareholders or stockholders, as they own a portion of the bank’s equity by purchasing its shares. Additionally, high-net-worth individuals or institutions investing in bank-offered financial products, such as mutual funds, bonds, or structured products, may be termed clients or wealth management investors. The specific title depends on the nature of their investment relationship with the bank.

Explore related products

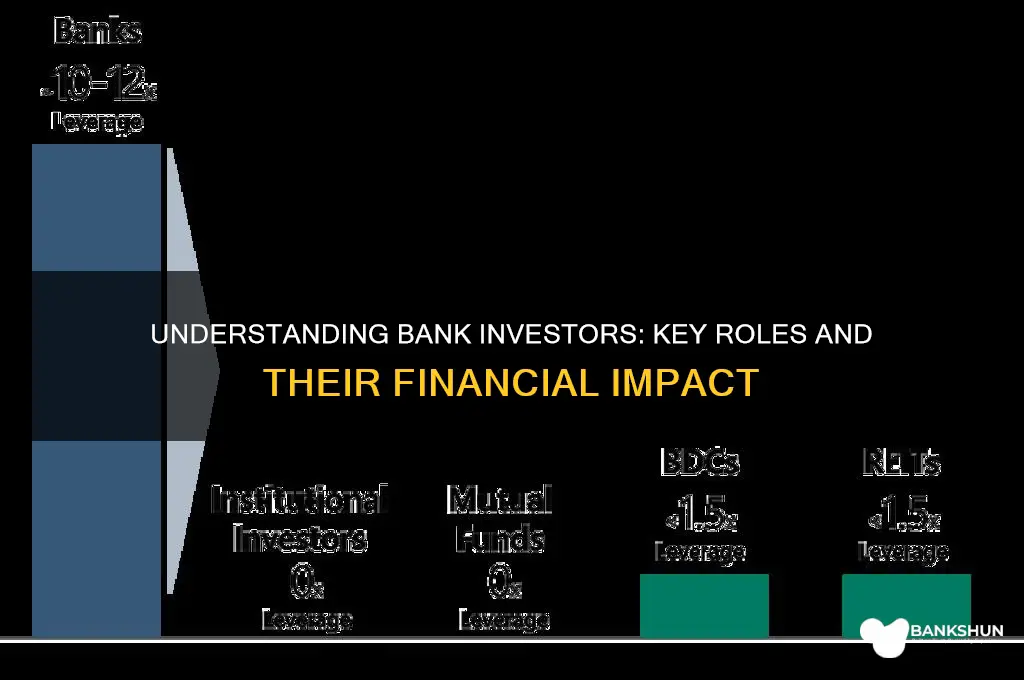

What You'll Learn

- Angel Investors: High-net-worth individuals providing capital for startups in exchange for equity or convertible debt

- Venture Capitalists: Firms investing in early-stage, high-potential companies for significant returns

- Institutional Investors: Organizations like pension funds, insurance companies, or mutual funds investing in banks

- Private Equity Investors: Firms buying stakes in banks to restructure and sell for profit

- Retail Investors: Individual investors purchasing bank stocks or bonds through public markets

![]()

Angel Investors: High-net-worth individuals providing capital for startups in exchange for equity or convertible debt

Angel investors are a distinct breed in the financial ecosystem, often operating outside the traditional banking sector yet playing a pivotal role in nurturing early-stage startups. Unlike institutional investors or venture capitalists, angel investors are typically high-net-worth individuals who invest their personal funds, driven by a mix of financial return and a passion for innovation. Their involvement goes beyond mere capital infusion; they often provide mentorship, industry connections, and strategic guidance, making them invaluable to fledgling businesses. This dual role of financier and advisor sets them apart from the more transactional relationships often seen in bank investments.

Consider the mechanics of their investments. Angel investors typically provide capital in exchange for equity or convertible debt, a structure that aligns their interests with those of the startup. Equity investments give them a stake in the company’s future success, while convertible debt allows them to convert their loan into equity at a later stage, often at a discounted rate. This flexibility is particularly appealing for startups that may not yet have a clear valuation or revenue stream. For instance, an angel investor might invest $500,000 in a tech startup in exchange for 10% equity, betting on the company’s potential to scale exponentially.

However, engaging with angel investors requires careful navigation. Startups must demonstrate not only a compelling business model but also a clear vision and scalability. Angel investors are selective, often investing in industries they understand or have a personal interest in. A biotech entrepreneur, for example, might target angel investors with a background in pharmaceuticals or healthcare. Additionally, startups should be prepared for due diligence, as angels will scrutinize financial projections, market potential, and the founding team’s capabilities. A well-crafted pitch deck and a solid business plan are non-negotiable.

One of the most significant advantages of angel investors is their accessibility compared to institutional funding. While banks and venture capital firms often have rigid criteria and lengthy approval processes, angel investors can make decisions more swiftly. This speed is critical for startups that need immediate capital to capitalize on market opportunities or overcome operational hurdles. However, this accessibility comes with a trade-off: angel investors expect higher returns to compensate for the risk they undertake by investing in unproven ventures.

In conclusion, angel investors occupy a unique niche in the investment landscape, bridging the gap between personal wealth and entrepreneurial ambition. Their willingness to take risks on early-stage companies, combined with their hands-on approach, makes them a vital resource for startups. For entrepreneurs, understanding the dynamics of angel investing—from structuring deals to crafting compelling pitches—can be the difference between securing funding and missing out on a transformative opportunity. While they may not be directly associated with banks, their impact on the startup ecosystem is undeniable, making them a critical player in the broader financial spectrum.

The Rise of Banking Giants: How Banks Became Too Big to Fail

You may want to see also

Explore related products

![]()

Venture Capitalists: Firms investing in early-stage, high-potential companies for significant returns

Venture capitalists are the high-stakes gamblers of the financial world, betting on early-stage companies with the potential to disrupt industries and deliver outsized returns. Unlike traditional bank investors who prioritize stability and incremental growth, VCs seek exponential gains by identifying and nurturing startups with innovative ideas, scalable business models, and ambitious founders. Their playbook involves taking calculated risks, often investing in sectors like technology, biotechnology, and clean energy, where the potential for 10x or even 100x returns exists. For instance, firms like Sequoia Capital and Andreessen Horowitz have turned modest initial investments into billions by backing companies like Google and Airbnb in their infancy.

To understand the VC approach, consider their investment lifecycle. It begins with due diligence, where VCs scrutinize a startup’s team, market opportunity, and competitive edge. Once invested, they actively participate in shaping the company’s strategy, often taking board seats to guide decision-making. This hands-on involvement distinguishes them from passive investors. VCs also leverage their networks to open doors for portfolio companies, connecting them with talent, customers, and strategic partners. However, this high-touch model comes with a cost: VCs typically expect a 20-30% internal rate of return (IRR) to compensate for the risk of backing unproven ventures.

A critical aspect of VC investing is the fund structure. VCs raise capital from limited partners (LPs), such as pension funds, endowments, and high-net-worth individuals, and deploy it across a portfolio of startups. A typical VC fund has a 10-year lifecycle, with the first 4-5 years dedicated to investing and the remainder for exits. Exits, whether through IPOs or acquisitions, are the ultimate goal, as they crystallize returns for both the VC firm and its LPs. For example, when Uber went public in 2019, early investors like Benchmark saw their stakes multiply manifold, validating the VC model’s potential for transformative wealth creation.

Despite the allure of massive returns, VC investing is not without pitfalls. The failure rate of startups is staggering, with studies suggesting that 75-90% of VC-backed ventures fail to deliver a positive return. VCs mitigate this risk through diversification, spreading their capital across 20-30 companies in a single fund. They also employ rigorous portfolio management, doubling down on winners while cutting losses on underperformers. Aspiring entrepreneurs should note that VCs are not just providers of capital but partners in growth, and alignment on vision and strategy is crucial for a successful relationship.

For banks and traditional investors, understanding the VC ecosystem offers valuable insights into fostering innovation and managing risk. While banks often focus on lending to established businesses, they can explore partnerships with VCs to co-invest in high-growth sectors or create corporate venture arms. For instance, Goldman Sachs’ Principal Strategic Investments group has backed startups like Robinhood and Stripe, blending traditional banking expertise with VC-style risk-taking. Such hybrid models demonstrate how the worlds of banking and venture capital can converge to drive economic growth and technological advancement.

HDFC Bank Recruitment: Exam Requirements and Application Process Explained

You may want to see also

Explore related products

$10.45 $19.99

![]()

Institutional Investors: Organizations like pension funds, insurance companies, or mutual funds investing in banks

Institutional investors, such as pension funds, insurance companies, and mutual funds, play a pivotal role in the banking sector by providing substantial capital and influencing market dynamics. These organizations are not individual investors but rather large entities that pool money from various sources to invest in banks and other financial instruments. Their scale allows them to wield significant influence over the institutions they invest in, often shaping strategic decisions and governance practices. For instance, a pension fund managing billions in assets can hold a sizable stake in a bank, giving it a voice in shareholder meetings and the power to push for changes in management or policy.

Consider the mechanics of how these institutional investors operate. Pension funds, for example, collect contributions from employees and employers over decades, investing these funds to grow them for retirement. A portion of this capital often finds its way into bank stocks or bonds, providing banks with long-term financing. Insurance companies, on the other hand, invest premiums to generate returns that help pay out claims and grow their business. Mutual funds, which pool money from individual investors, offer a diversified portfolio that frequently includes bank securities. Each of these entities has distinct investment horizons, risk tolerances, and regulatory requirements, but they all share a common goal: maximizing returns while managing risk.

One critical aspect of institutional investors’ involvement in banks is their role in corporate governance. Unlike retail investors, who may lack the resources or interest to engage with bank management, institutional investors actively monitor their investments. They often participate in proxy voting, advocate for transparency, and push for sustainable practices. For example, a mutual fund might vote against a bank’s executive compensation plan if it deems it excessive or misaligned with performance. This oversight helps align the interests of bank management with those of shareholders, fostering accountability and long-term value creation.

However, institutional investors’ influence is not without challenges. Their size and market power can sometimes lead to herd behavior, where multiple funds make similar investment decisions, amplifying market volatility. Additionally, their focus on short-term returns can conflict with banks’ need for long-term stability. Regulators must strike a balance between encouraging investment and preventing systemic risks. For banks, attracting and retaining institutional investors requires not only strong financial performance but also robust risk management and clear communication of strategic goals.

In practical terms, banks seeking institutional investment should focus on three key areas: transparency, sustainability, and performance. Regular, detailed disclosures about financial health and risk exposure build trust. Embracing ESG (Environmental, Social, and Governance) principles demonstrates a commitment to long-term value creation. Finally, consistent financial performance, underpinned by sound strategy, ensures that banks remain attractive investment opportunities. By understanding and catering to the needs of institutional investors, banks can secure the capital necessary for growth while fostering a healthier financial ecosystem.

Does the US Fund the World Bank? Unraveling Financial Contributions

You may want to see also

Explore related products

![]()

Private Equity Investors: Firms buying stakes in banks to restructure and sell for profit

Private Equity (PE) firms have emerged as key players in the banking sector, strategically acquiring stakes in financial institutions with a clear objective: to restructure and sell for profit. Unlike traditional investors who seek steady dividends or long-term growth, PE firms operate with a finite timeline, typically 5–7 years, during which they implement operational, financial, and strategic overhauls to maximize returns. This approach, often referred to as "buy-to-sell," leverages the firms’ expertise in turnaround management and their ability to inject capital into underperforming banks. Examples include Blackstone’s investment in Deutsche Bank’s real estate division and Apollo Global Management’s acquisition of banks during the 2008 financial crisis, both aimed at revitalizing assets for lucrative exits.

The process begins with due diligence, where PE firms assess a bank’s strengths, weaknesses, and potential for improvement. Key areas of focus include cost-cutting, technology modernization, and portfolio optimization. For instance, a PE firm might streamline a bank’s branch network, invest in digital banking platforms, or divest non-core assets to improve efficiency. These interventions are designed to enhance profitability and attract higher valuations when the bank is sold. However, this model is not without risks. PE firms must navigate regulatory scrutiny, market volatility, and the challenge of aligning short-term goals with long-term banking stability.

Critics argue that PE firms’ profit-driven approach can prioritize financial gains over customer interests or systemic stability. For example, aggressive cost-cutting might lead to reduced services or job losses, while rapid restructuring could undermine a bank’s risk management frameworks. To mitigate these concerns, regulators in jurisdictions like the EU and the U.S. have introduced stricter oversight for PE investments in banks, including capital adequacy requirements and transparency mandates. Despite these challenges, the PE model has proven effective in revitalizing struggling banks, as seen in KKR’s turnaround of Spanish lender Bankia, which was later merged with CaixaBank.

For banks, partnering with PE firms can provide much-needed capital and expertise, particularly in times of financial distress. However, banks must carefully negotiate terms to ensure alignment with their long-term vision. PE firms, on the other hand, must balance their profit motives with sustainable banking practices to maintain credibility and regulatory compliance. Practical tips for banks considering PE investment include conducting thorough due diligence on potential partners, negotiating clear exit strategies, and ensuring that restructuring plans prioritize both financial health and customer trust.

In conclusion, private equity investors play a unique and transformative role in the banking sector, offering a blend of capital, expertise, and strategic vision. While their buy-to-sell model can yield significant returns, it requires careful execution and regulatory vigilance to avoid unintended consequences. As the financial landscape evolves, the interplay between PE firms and banks will continue to shape the industry, offering both opportunities and challenges for stakeholders.

Exploring Fidelity Bank's Network: Total Number of Branches Revealed

You may want to see also

Explore related products

$89.69 $119.99

$41.99

![]()

Retail Investors: Individual investors purchasing bank stocks or bonds through public markets

Retail investors are the backbone of public markets, and their role in the banking sector is both significant and multifaceted. These individuals, often referred to as "main street investors," purchase bank stocks or bonds through public exchanges, becoming partial owners or creditors of financial institutions. Unlike institutional investors, who manage large pools of capital, retail investors typically operate with smaller portfolios, yet their collective impact on bank capitalization and market liquidity cannot be overstated. For instance, during the 2020 market volatility, retail investors accounted for nearly 25% of trading volume in bank stocks, showcasing their growing influence.

Investing in bank stocks or bonds is not a one-size-fits-all strategy. Retail investors must consider their risk tolerance, financial goals, and time horizon. Bank stocks, such as those of JPMorgan Chase or Wells Fargo, offer potential for capital appreciation and dividends but are subject to market fluctuations and economic cycles. Bonds, on the other hand, provide steady income through fixed interest payments and are generally less volatile, making them suitable for conservative investors. A practical tip for beginners is to start with a diversified portfolio, allocating no more than 10-15% of their investment capital to a single bank to mitigate risk.

One of the key advantages of retail investing in banks is accessibility. With the rise of online brokerage platforms like Robinhood, Fidelity, and Charles Schwab, individuals can buy bank securities with as little as $100. These platforms often offer educational resources, real-time market data, and fractional shares, lowering barriers to entry. However, investors should be cautious of transaction fees, which can erode returns over time. For example, a $5 trading fee on a $100 investment represents a 5% immediate loss—a critical consideration for small-scale investors.

Comparatively, retail investors differ from institutional investors in their approach and resources. While institutions rely on sophisticated analytics and large-scale trading strategies, retail investors often depend on public information, financial news, and personal research. This disparity highlights the importance of staying informed. Retail investors should monitor bank earnings reports, regulatory changes, and macroeconomic trends to make informed decisions. For instance, understanding how interest rate hikes affect bank profitability can guide investment choices in a rising-rate environment.

In conclusion, retail investors play a vital role in the banking ecosystem by providing capital and driving market activity. Their ability to participate in public markets democratizes investing, but it also requires diligence and strategy. By focusing on diversification, leveraging accessible tools, and staying informed, individual investors can navigate the complexities of bank stocks and bonds effectively. Whether aiming for long-term growth or steady income, retail investors have the power to shape their financial futures—one trade at a time.

Appraisers and Home Inspections: What You Need to Know

You may want to see also

Frequently asked questions

Investors at banks who provide capital are often referred to as institutional investors or bank shareholders, depending on their level of involvement and the type of investment.

Individuals or entities investing in bank-issued securities or funds are commonly called bondholders, shareholders, or fund investors, depending on the specific investment vehicle.

Investors partnering with banks for large-scale projects are often referred to as syndicate members, co-investors, or limited partners, depending on the structure of the financing arrangement.