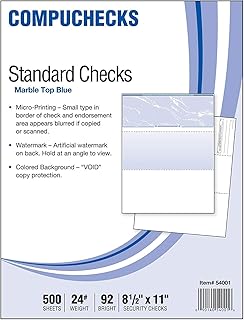

A bank cheque, also known as a cashier's check or teller's check, is a secure payment instrument issued by a bank, guaranteeing the availability of funds. Typically, it features the bank's name and logo prominently at the top, followed by the account holder's details and the payee's information. The cheque includes a unique serial number, a date of issue, and the amount payable, often written in both numerical and word formats to prevent fraud. Security measures such as watermarks, holograms, or microprinting are commonly incorporated to ensure authenticity. The bank's signature or stamp is usually present, along with a designated area for the recipient's endorsement. Its standardized design and robust security features make it a trusted method for large or critical transactions.

| Characteristics | Values |

|---|---|

| Size | Typically 6.125 inches by 2.75 inches (155.575 mm by 69.85 mm) |

| Color | Usually white or off-white, with security features like watermarks or colored backgrounds |

| Layout | Divided into sections: payee line, amount in words, amount in numbers, signature line, date line, bank details, and MICR line |

| Payee Line | Designated area to write the name of the person or entity receiving the funds |

| Amount in Words | Written out in words (e.g., "One Thousand Five Hundred Dollars") |

| Amount in Numbers | Printed or written in numerical format in a designated box |

| Signature Line | Space for the account holder’s signature to authorize the transaction |

| Date Line | Area to write the date the cheque is issued |

| Bank Details | Includes the bank’s name, branch, account number, and cheque number |

| MICR Line | Magnetic Ink Character Recognition line at the bottom containing account, cheque, and bank routing numbers |

| Security Features | Holograms, watermarks, microprinting, UV ink, and security threads to prevent fraud |

| Memo Line | Optional field for noting the purpose of the cheque (e.g., "Rent Payment") |

| Issuer Information | Pre-printed details of the account holder’s name and address |

| Bank Logo | The issuing bank’s logo is prominently displayed |

| Currency | Denoted in the local currency (e.g., USD, EUR, GBP) |

| Perforations | Perforated edges for easy tearing from a cheque book |

Explore related products

What You'll Learn

- Cheque Layout Basics: Standard format, sections, and essential elements like payee line, amount box, and signature area

- Security Features: Watermarks, holograms, microprinting, and UV ink to prevent fraud and counterfeiting

- Bank Details: Bank name, logo, branch info, and account numbers displayed on the cheque

- Cheque Types: Differences between cashier’s, personal, and certified cheques in appearance and use

- Date and Signatures: Proper placement and importance of the date and signature for validity

![]()

Cheque Layout Basics: Standard format, sections, and essential elements like payee line, amount box, and signature area

A bank cheque, at its core, is a standardized financial instrument, and its layout is designed for clarity, security, and ease of processing. The standard format typically follows a horizontal orientation, divided into distinct sections that serve specific purposes. These sections include the payee line, amount box, and signature area, each playing a critical role in ensuring the cheque’s validity and functionality. Understanding these elements is essential for anyone issuing or receiving a cheque, as errors in any section can render the document unusable.

The payee line is arguably the most straightforward yet crucial part of a cheque. Located near the top, it is where the recipient’s name is written. This line must be filled out clearly and accurately, as it specifies who is authorized to deposit or cash the cheque. Banks often reject cheques with ambiguous or altered payee names, so precision is key. For example, if the payee is a business, the full legal name should be used, avoiding abbreviations unless explicitly allowed. This section is also where the phrase "Pay to the Order of" is typically printed, emphasizing the cheque’s purpose.

Next, the amount box is where the numerical value of the cheque is recorded. This box is usually positioned to the right of the payee line and is designed to prevent fraud by providing a clear, unambiguous record of the amount. It’s important to write the amount in numerals, ensuring the numbers are neatly aligned and do not extend beyond the box. For instance, if the cheque is for $150.75, write "150.75" in the box. A common tip is to draw a line after the amount to prevent additional digits from being fraudulently added.

The signature area is located at the bottom right of the cheque and is where the issuer signs to authorize the transaction. This section is critical for security, as the signature must match the one on file with the bank. Without a valid signature, the cheque is invalid. It’s also worth noting that some cheques include a second line for a co-signer, typically used for joint accounts. A practical tip is to sign the cheque in ink, preferably blue or black, to ensure the signature is clear and tamper-evident.

Beyond these essential elements, cheques often include additional sections like the memo line, bank details, and security features. The memo line, usually found on the bottom left, allows the issuer to note the purpose of the cheque (e.g., "Rent for January"). While optional, it can be useful for record-keeping. Bank details, such as the account number and routing number, are pre-printed on the cheque to facilitate processing. Security features, like watermarks, microprinting, or holograms, are incorporated to deter counterfeiting. Together, these elements form a cohesive layout that balances functionality with security, making the cheque a reliable financial tool.

Banking Crisis Update: Tracking Collapsed Institutions This Month

You may want to see also

Explore related products

![]()

Security Features: Watermarks, holograms, microprinting, and UV ink to prevent fraud and counterfeiting

Bank cheques are not just slips of paper; they are fortified documents designed to thwart fraudsters at every turn. One of the most subtle yet effective security features is the watermark. Embedded within the cheque paper, watermarks are visible only when held up to light, revealing a faint, intricate design—often the bank’s logo or a currency symbol. Counterfeiters struggle to replicate this feature because it requires specialized paper-making techniques. For instance, the U.S. Treasury uses a watermark of the respective bill denomination on its currency, a practice some banks have adopted for cheques. To verify a watermark, hold the cheque against a light source and look for consistency in design and clarity—a smudged or missing watermark is a red flag.

While watermarks rely on simplicity, holograms bring a dynamic, high-tech layer to cheque security. These iridescent, 3D images shift appearance when tilted, making them nearly impossible to reproduce accurately. Holograms on cheques often display the bank’s emblem or a security code, and their complexity deters even skilled forgers. For example, the Reserve Bank of India incorporates holographic strips on its high-value cheques, which change color and pattern under different angles. When inspecting a hologram, ensure it’s not a sticker or printed image—genuine holograms are seamlessly integrated into the cheque material.

Microprinting is another stealthy weapon in the fight against fraud. This technique involves printing tiny, often invisible text that can only be read with a magnifying glass. On cheques, microprinting might appear as a line of fine print along the borders or within the signature area. The text is usually a repeated phrase like “VOID” or the bank’s name. Counterfeiters often overlook this detail, resulting in blurred or illegible microprint. To check for microprinting, use a 10x magnifying glass—if the text is sharp and consistent, the cheque is likely authentic.

Rounding out the security arsenal is UV ink, a feature invisible to the naked eye but glowing under ultraviolet light. Banks use UV ink to print hidden symbols, codes, or patterns on cheques. For instance, a UV pen might reveal a bank’s logo or a serial number in a specific area. This feature is particularly effective because UV lights are not commonly available, and replicating UV ink requires specialized knowledge. If you have access to a UV light, scan the cheque for hidden markings—their absence or inconsistency could indicate tampering.

Together, these features—watermarks, holograms, microprinting, and UV ink—create a multi-layered defense system that makes cheques incredibly difficult to counterfeit. Each element serves a unique purpose, from the subtle artistry of watermarks to the high-tech dazzle of holograms. For individuals and businesses, understanding these features is key to spotting fraudulent cheques. Always scrutinize cheques under varying conditions—light, magnification, and UV—to ensure their authenticity. In an era of digital transactions, these physical safeguards remain a critical line of defense against financial fraud.

Reducing Bank Regulations: Unlocking Growth, Innovation, and Financial Stability

You may want to see also

Explore related products

![]()

Bank Details: Bank name, logo, branch info, and account numbers displayed on the cheque

A bank cheque is a formal document, and its design is both functional and secure. At the top, the bank name is prominently displayed, often in bold or stylized font, ensuring immediate identification. Adjacent to this, the bank logo appears, serving as a visual authenticator and reinforcing brand recognition. These elements are not merely decorative; they are critical for trust and verification in financial transactions.

Below the bank name and logo, branch information is typically listed, including the branch name, address, and sometimes a contact number. This detail is essential for tracing the cheque’s origin and resolving discrepancies. For instance, if a cheque is disputed, the branch info provides a direct link to the issuing location. While this section may seem secondary, it plays a pivotal role in the cheque’s operational integrity.

The account number is another cornerstone of a cheque’s design, usually located at the bottom left or right corner. This number is paired with the sort code or routing number, which identifies the specific bank branch. Together, these details enable seamless electronic processing. For security, account numbers are often printed in MICR (Magnetic Ink Character Recognition) font, readable by machines but difficult to replicate fraudulently.

Practical tip: When filling out a cheque, ensure the account number is legible and matches the pre-printed details exactly. Errors here can lead to processing delays or rejections. Additionally, never share your account number or sort code unless absolutely necessary, as this information can be exploited for fraudulent activities.

In comparison to digital payment methods, the physical display of bank details on a cheque serves as a tangible layer of security. While online transactions rely on encryption, cheques use visible and embedded features—like watermarks, holograms, and MICR fonts—to deter fraud. This blend of traditional and modern security measures underscores the cheque’s enduring relevance in financial systems.

Crafting a Thermocol Bank: A Creative DIY Project Guide

You may want to see also

Explore related products

![]()

Cheque Types: Differences between cashier’s, personal, and certified cheques in appearance and use

Bank cheques, though less common in today’s digital age, remain essential for specific financial transactions. Their appearance and use vary significantly depending on the type—cashier’s, personal, or certified. Understanding these differences ensures you choose the right cheque for your needs.

Cashier’s cheques stand out for their security and reliability. Issued by a bank, they are drawn on the bank’s funds, not your personal account. Visually, they often feature the bank’s logo prominently, a pre-printed amount, and a watermark for added security. The recipient’s name is typically filled in by the bank, and the cheque is signed by a bank official. Use these for high-value transactions like purchasing a car or making a down payment on a house, as they are guaranteed by the bank and reduce the risk of bounced payments.

Personal cheques, in contrast, are the most common and user-friendly. They are drawn on your personal bank account and feature your name, address, and account details. The appearance is straightforward: a blank line for the payee’s name, an amount field, and your signature. While convenient for everyday use, they carry higher risk since they depend on sufficient funds in your account. Always ensure your account balance covers the cheque amount to avoid fees or legal issues.

Certified cheques bridge the gap between cashier’s and personal cheques. They are personal cheques verified by your bank, which stamps and signs them to confirm sufficient funds. The appearance is similar to a personal cheque but includes a bank certification mark. Use certified cheques when the recipient requires assurance of payment but doesn’t need the full security of a cashier’s cheque. They are ideal for transactions where trust is a concern but the amount isn’t excessively high.

In summary, the type of cheque you choose depends on the transaction’s nature and the level of security required. Cashier’s cheques offer maximum reliability, personal cheques provide convenience, and certified cheques strike a balance between the two. Always verify the recipient’s requirements and your bank’s policies before selecting a cheque type.

Unlocking Wealth: Strategies to Secure Millions in Bank Financing

You may want to see also

Explore related products

![]()

Date and Signatures: Proper placement and importance of the date and signature for validity

The date on a bank cheque is more than a timestamp—it’s a legal marker that determines the cheque’s validity and processing timeline. Typically placed in the upper right corner, it must be written clearly in the format specified by the bank (e.g., DD/MM/YYYY or MM/DD/YYYY). A post-dated cheque, for instance, cannot be cashed before the indicated date, while a cheque older than six months (in most jurisdictions) is considered stale and may be rejected. Precision here is non-negotiable; even a minor error, like an incorrect year, can render the cheque invalid.

Signatures on a bank cheque serve as the final authorization, confirming the account holder’s consent for the transaction. The signature line is usually located at the bottom right, adjacent to the memo line. It must match the signature on file with the bank; discrepancies can lead to rejection. For joint accounts, both signatories may be required, depending on the account’s terms. A missing or forged signature voids the cheque, emphasizing its role as a security measure. Always sign in ink, as pencil or digital signatures are often unacceptable.

Proper placement of the date and signature is critical for seamless processing. The date must be within the visible area designated by the cheque’s design, ensuring it doesn’t overlap with other fields like the payee line or amount box. Similarly, the signature should fit entirely within the provided space, avoiding smudges or extensions that could obscure adjacent details. Misplacement risks confusion or misinterpretation by bank systems, potentially delaying or halting the transaction.

Beyond placement, the timing of dating and signing matters. A cheque should be dated and signed immediately before issuance to prevent fraud or misuse. For example, signing a blank cheque in advance leaves it vulnerable to unauthorized alterations. Conversely, backdating or predating a cheque can raise legal and ethical concerns, particularly in financial audits. Adhering to these practices ensures the cheque’s integrity and aligns with banking regulations.

In summary, the date and signature on a bank cheque are not mere formalities but essential elements that validate the instrument. Their correct placement, format, and timing safeguard against errors, fraud, and legal complications. By understanding their significance and adhering to best practices, cheque writers can ensure smooth transactions and maintain financial security. Treat these details with the same care as the amount itself—they are the linchpins of a cheque’s legitimacy.

Mastering Bank Fishing on the Sacramento River: Tips and Techniques

You may want to see also

Frequently asked questions

A bank cheque typically features a rectangular piece of paper with the bank's name, logo, and contact information printed at the top. It includes fields for the date, payee's name, amount in numbers and words, and the account holder's signature.

Bank cheques often have a standardized color scheme, usually in shades of blue, black, or green. They may include security features like watermarks, holograms, or microprinting to prevent fraud.

The account and routing numbers are usually found at the bottom of the cheque, printed in MICR (Magnetic Ink Character Recognition) font. The routing number is on the left, followed by the account number, and then the cheque number.

Yes, bank cheques are typically standardized in size, measuring approximately 6.14 inches by 2.75 inches (156 mm by 70 mm). They follow a uniform layout to ensure compatibility with banking systems.

Common security features include watermarks, security threads, fluorescent fibers, and chemical-sensitive paper that reacts to alterations. Some cheques also have holographic overlays or unique serial numbers for added protection.

![Reusable Giant Check [48" x 24"] - Dry Erase Big Checks for Presentations, Oversized Checks for Presentation, Novelty Big Check, Giant Big Fake Check, Large Checks for Presentations, Donation, Awards](https://m.media-amazon.com/images/I/81v8nI6+hBL._AC_UL320_.jpg)

![Reusable Big Check for Presentaion[30" x 16"] - Big Check Giant Dry Erase Checks for Presentations, Novelty Oversized Blank Checks,Large Fake Checks for Donation, Awards,Fundraisers](https://m.media-amazon.com/images/I/710PVCa6VwL._AC_UL320_.jpg)