In the banking sector, ACM stands for Automated Clearing House (ACH) Credit Memo, a term used to describe a specific type of transaction within the ACH network. This network facilitates electronic funds transfers between financial institutions, enabling seamless and efficient payment processing. An ACH Credit Memo is a transaction code that represents a credit being pushed from one account to another, often used for direct deposits, vendor payments, or tax refunds. Understanding ACM is crucial for banks and financial professionals, as it plays a significant role in the smooth operation of electronic payment systems and ensures accurate and timely fund transfers.

Explore related products

What You'll Learn

![]()

Automated Clearing House (ACH)

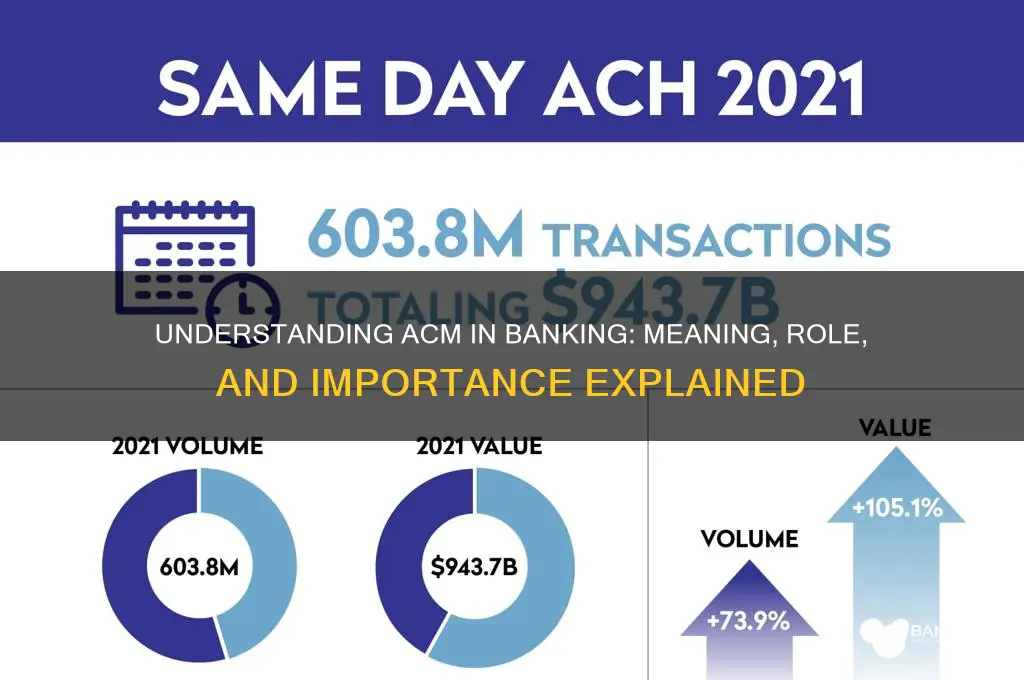

In the realm of banking, ACM often refers to Automated Clearing House (ACH), a network that processes electronic payments and collections between banks. Unlike wire transfers, which are immediate and often costly, ACH transactions are batch-processed, making them ideal for recurring payments like payroll, bill payments, and direct deposits. This system operates on a timetable, typically settling transactions within 1–2 business days, ensuring efficiency without compromising cost-effectiveness.

Consider the mechanics of ACH: it functions as a middleman, aggregating transactions from originating banks and routing them to receiving banks. For instance, when an employer initiates payroll, the ACH network consolidates employee payments, verifies account details, and ensures funds are transferred securely. This batch processing reduces the administrative burden on banks and minimizes errors, making it a cornerstone of modern financial operations. However, it’s crucial to note that ACH transactions are not instantaneous, so timing is key when scheduling payments.

From a practical standpoint, businesses and individuals can leverage ACH for its cost-efficiency and reliability. For businesses, ACH is a preferred method for handling large volumes of transactions, such as vendor payments or customer refunds. Individuals benefit from its use in direct deposits, utility bill payments, and loan repayments. To optimize ACH usage, ensure account information is accurate, monitor transaction timelines, and set up alerts for recurring payments. Additionally, understanding ACH return codes (e.g., for insufficient funds or incorrect account details) can help troubleshoot issues promptly.

Comparatively, ACH stands out against other payment methods like credit cards or wire transfers due to its lower fees and reduced risk of fraud. While credit cards offer instant processing, they incur higher transaction costs, and wire transfers, though faster, are more expensive and less suitable for routine payments. ACH strikes a balance, offering a secure, affordable solution for both high-volume and recurring transactions. Its widespread adoption across industries underscores its reliability and adaptability in the evolving financial landscape.

In conclusion, ACH is not just a banking acronym but a vital tool that streamlines financial transactions. Its batch-processing model, cost-efficiency, and broad applicability make it indispensable for businesses and individuals alike. By understanding its mechanics and best practices, users can maximize its benefits while minimizing potential pitfalls. Whether you’re managing payroll, paying bills, or receiving direct deposits, ACH remains a cornerstone of efficient, secure banking operations.

Steps to Become a Successful Bank Financial Center Manager

You may want to see also

Explore related products

$45.35

![]()

Association for Computing Machinery (ACM) relevance

The Association for Computing Machinery (ACM) is often mistaken for a banking acronym, but its relevance to the financial sector is profound, albeit indirect. While "ACM" in banking might refer to specific systems or processes, the ACM as an organization plays a pivotal role in shaping the technological backbone of modern banking. By advancing computing research, education, and innovation, the ACM indirectly influences how banks develop and deploy technologies like blockchain, AI, and cybersecurity frameworks. This connection highlights the symbiotic relationship between computing advancements and financial services, where the ACM’s work underpins the tools banks rely on to operate efficiently and securely.

Consider the rise of fintech, where ACM’s contributions to algorithms, data science, and machine learning have enabled banks to automate risk assessments, personalize customer experiences, and detect fraud in real time. For instance, the ACM’s Digital Library provides access to cutting-edge research that banks leverage to stay ahead of cyber threats. A practical example is the use of ACM-published studies on quantum computing, which banks are exploring to future-proof their encryption methods. This demonstrates how the ACM’s focus on theoretical and applied computing translates into tangible benefits for the banking industry, even if the acronym itself isn’t directly tied to banking terminology.

To harness the ACM’s relevance effectively, banks should prioritize collaboration with computing professionals and researchers affiliated with the organization. Steps include sponsoring ACM conferences, integrating ACM-recommended best practices into IT strategies, and encouraging employees to join ACM chapters for skill development. Caution, however, should be exercised in over-relying on academic research without practical adaptation. The ACM’s insights are most valuable when tailored to specific banking challenges, such as regulatory compliance or legacy system modernization. By bridging the gap between theory and application, banks can maximize the ACM’s impact on their operations.

A comparative analysis reveals that while other organizations focus on banking-specific standards (e.g., SWIFT for payments), the ACM’s strength lies in its broad, interdisciplinary approach to computing. This makes it uniquely positioned to address cross-cutting issues like data privacy, algorithmic bias, and scalability—challenges that banks increasingly face in a digital-first world. For example, ACM’s Code of Ethics provides a framework for ethical AI deployment, a critical consideration as banks adopt machine learning models for credit scoring. This broader perspective ensures that banks aren’t just adopting technology but doing so responsibly and sustainably.

In conclusion, while "ACM" may not be a banking acronym, the Association for Computing Machinery is indispensable to the industry’s technological evolution. Its research, resources, and community foster innovation that banks can directly apply to enhance security, efficiency, and customer trust. By engaging with the ACM, financial institutions can stay at the forefront of technological advancements, ensuring they remain competitive in an increasingly digital landscape. The takeaway is clear: the ACM’s relevance to banking lies not in its name but in its ability to shape the future of computing, which, in turn, shapes the future of finance.

Bank Currency Trading: A Step-by-Step Guide to Exchange Rates and Fees

You may want to see also

Explore related products

![]()

ACM in financial technology (Fintech)

In the realm of financial technology (Fintech), ACM often stands for Automated Cash Management, a critical function that leverages technology to streamline liquidity management, optimize cash flow, and enhance financial decision-making. Unlike manual processes, ACM systems integrate real-time data analytics, machine learning, and predictive modeling to automate tasks such as cash forecasting, fund allocation, and risk mitigation. For instance, Fintech platforms like Treasury Prime and Kyriba use ACM to help businesses monitor cash positions across multiple accounts, predict future cash needs, and execute transactions seamlessly. This automation reduces human error, improves efficiency, and ensures liquidity is always aligned with operational demands.

Consider the operational challenges faced by multinational corporations with accounts spread across different banks and regions. ACM systems consolidate this fragmented data into a unified dashboard, providing CFOs and treasurers with actionable insights. For example, an ACM tool might flag surplus cash in one region and automatically transfer it to another where funds are needed, all while adhering to regulatory compliance. This level of automation is particularly valuable in Fintech, where speed and accuracy are paramount. However, implementing ACM requires careful integration with existing ERP systems and robust cybersecurity measures to protect sensitive financial data.

From a persuasive standpoint, adopting ACM in Fintech is not just a luxury but a necessity in today’s fast-paced financial landscape. Startups and established firms alike can gain a competitive edge by reducing idle cash, minimizing borrowing costs, and improving investment strategies. For instance, a Fintech company managing a digital wallet platform could use ACM to dynamically allocate user funds into high-yield accounts, boosting returns without compromising liquidity. The key takeaway? ACM transforms passive cash management into an active, strategic function that drives profitability and resilience.

Comparatively, while traditional banking systems often rely on siloed, manual processes for cash management, Fintech’s ACM solutions are inherently collaborative and interconnected. APIs play a pivotal role here, enabling seamless communication between banks, payment gateways, and third-party applications. For example, Stripe’s Treasury product uses ACM principles to allow businesses to manage payouts, balances, and reserves directly within their payment workflows. This contrasts sharply with legacy systems, where such tasks would require multiple logins and manual interventions. The result? Fintech’s ACM not only simplifies operations but also fosters innovation by enabling new financial products and services.

Finally, a descriptive lens reveals how ACM is reshaping the Fintech ecosystem by democratizing access to sophisticated cash management tools. Small and medium-sized enterprises (SMEs), historically underserved by traditional banks, can now leverage ACM-powered platforms to achieve financial optimization once reserved for large corporations. Tools like Float or Fluidly offer SMEs cash flow forecasting, invoice management, and automated payment scheduling at affordable price points. This leveling of the playing field underscores ACM’s role in driving financial inclusion and empowering businesses of all sizes to thrive in an increasingly digital economy.

Is a Bank Run a Real Risk? Understanding Financial Stability

You may want to see also

Explore related products

![]()

ACM standards for banking security

In the realm of banking, ACM stands for Account Change Management, a critical process ensuring the integrity and security of customer accounts during updates or modifications. However, when discussing ACM standards for banking security, it’s essential to clarify that ACM here refers to Access Control Management, a cornerstone of safeguarding sensitive financial data. Access control is the gatekeeper of banking systems, dictating who can view, modify, or manage customer information. Without robust ACM standards, banks risk unauthorized access, data breaches, and regulatory non-compliance.

Implementing ACM standards involves a multi-step approach. First, authentication protocols must be established to verify user identities. This includes multi-factor authentication (MFA), where users provide two or more verification factors (e.g., password and biometric scan). Second, authorization frameworks define user permissions based on roles. For instance, a teller may access transaction histories but not account balances. Third, audit trails must be maintained to track all access attempts, ensuring accountability. Tools like SIEM (Security Information and Event Management) systems can automate this process, flagging anomalies in real time.

A comparative analysis reveals that banks adopting ACM standards experience 40% fewer security incidents compared to those relying on outdated access controls. For example, a European bank that integrated role-based access control (RBAC) and privileged access management (PAM) reduced insider threats by 50% within six months. Conversely, institutions lacking these measures often face hefty fines under regulations like GDPR or PCI DSS. The takeaway is clear: ACM standards are not optional but a necessity in a digital banking landscape rife with cyber threats.

To adopt ACM standards effectively, banks should follow a phased approach. Phase 1: Assessment involves auditing existing access controls and identifying vulnerabilities. Phase 2: Implementation includes deploying MFA, RBAC, and PAM solutions. Phase 3: Monitoring requires continuous oversight using AI-driven tools to detect unusual access patterns. Caution must be exercised in balancing security with user experience; overly restrictive controls can frustrate employees and customers. Finally, Phase 4: Compliance ensures alignment with regulatory requirements, such as regular penetration testing and third-party audits.

In conclusion, ACM standards for banking security are a dynamic, layered defense mechanism. By prioritizing access control management, banks not only protect customer data but also build trust and maintain regulatory compliance. The investment in robust ACM frameworks is not just a cost but a strategic imperative in an era where cyber threats evolve daily.

Wells Fargo: Still a Banking Powerhouse?

You may want to see also

![]()

ACM’s role in regulatory compliance

In banking, ACM stands for Anti-Money Laundering Compliance, a critical function that ensures financial institutions adhere to regulatory requirements designed to combat illicit financial activities. The role of ACM in regulatory compliance is multifaceted, involving proactive measures to detect, prevent, and report suspicious transactions. By leveraging advanced technologies and robust frameworks, ACM professionals safeguard institutions from reputational damage, financial penalties, and legal consequences.

Consider the lifecycle of ACM compliance: it begins with customer due diligence (CDD), where institutions verify the identity of clients and assess their risk profiles. For instance, high-risk customers, such as politically exposed persons (PEPs), require enhanced due diligence (EDD) to mitigate potential risks. This process is not one-size-fits-all; it demands tailored approaches based on factors like transaction volume, geographic location, and business relationships. Practical tip: Automate CDD processes using AI-driven tools to reduce manual errors and increase efficiency, ensuring compliance without compromising customer experience.

Next, transaction monitoring is a cornerstone of ACM’s regulatory role. Institutions must continuously screen transactions for anomalies that could indicate money laundering or terrorist financing. For example, a sudden spike in transaction amounts or frequent cross-border payments may trigger alerts. However, false positives are a common challenge, often overwhelming compliance teams. To address this, implement machine learning algorithms that refine monitoring systems over time, distinguishing genuine risks from benign activities. Caution: Over-reliance on technology without human oversight can lead to missed red flags, so maintain a balanced approach.

Reporting is another critical aspect of ACM’s compliance function. Financial institutions are mandated to file Suspicious Activity Reports (SARs) with regulatory bodies like FinCEN in the U.S. or the NCA in the UK. Timeliness and accuracy are paramount; delays or incomplete reports can result in severe penalties. For instance, in 2020, a global bank was fined $400 million for failing to submit SARs promptly. Takeaway: Establish a structured reporting workflow, including internal reviews and legal consultations, to ensure compliance and minimize risks.

Finally, ACM plays a pivotal role in training and awareness programs. Regulatory compliance is not solely the responsibility of the compliance team; it requires institution-wide vigilance. Regular training sessions on AML regulations, red flag indicators, and reporting procedures empower employees to act as the first line of defense. Comparative analysis shows that institutions with comprehensive training programs experience 30% fewer compliance breaches than those with ad-hoc approaches. Instruction: Develop role-specific training modules, incorporating real-world case studies, to enhance engagement and retention.

In summary, ACM’s role in regulatory compliance is a dynamic and indispensable function within banking. By integrating advanced technologies, structured processes, and proactive training, institutions can navigate the complex landscape of AML regulations effectively. The ultimate goal is not just to meet regulatory standards but to foster a culture of integrity and accountability that protects both the institution and the broader financial ecosystem.

Backpacks at Citizens Bank Park: What's Allowed?

You may want to see also

Frequently asked questions

ACM stands for Automated Clearing House (ACH) Management in banking, though it can also refer to Account and Cash Management depending on the context.

ACM is used to streamline electronic payment processing, manage cash flow, and oversee account transactions efficiently, often through ACH systems.

Yes, ACM can be applied to international banking, particularly in managing cross-border payments and cash management solutions.

ACM improves efficiency, reduces manual errors, enhances cash visibility, and lowers transaction costs by automating processes.

ACM is applicable to banks of all sizes, as it helps manage accounts and cash flow regardless of the institution's scale.