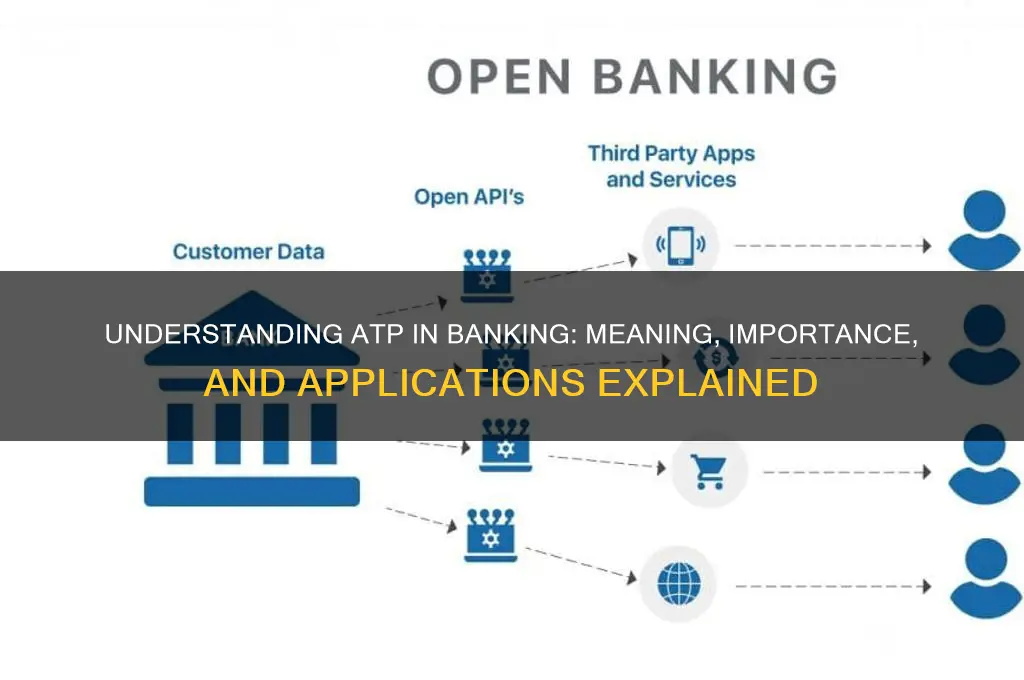

ATP in banking stands for Automated Trust and Payment, a system designed to streamline and secure financial transactions by automating processes such as fund transfers, payment settlements, and trust account management. It enhances efficiency, reduces errors, and ensures compliance with regulatory standards, making it a critical tool for financial institutions to manage complex transactions with precision and reliability.

Explore related products

$72.95 $72.95

$51.16 $63.95

What You'll Learn

![]()

Automated Teller Machines (ATMs)

In the realm of banking, ATP often refers to Automated Transaction Processing, a system that streamlines financial operations by minimizing manual intervention. However, when discussing Automated Teller Machines (ATMs), it’s crucial to clarify that ATP isn’t directly tied to their functionality. Instead, ATMs themselves are a cornerstone of automated banking, enabling customers to perform transactions without human assistance. These machines have evolved from simple cash dispensers to multifunctional hubs offering services like deposits, transfers, and even bill payments. Understanding their role provides insight into how banks leverage technology to enhance accessibility and efficiency.

Consider the mechanics of an ATM transaction: when a user inserts their card, the machine communicates with the bank’s network to verify credentials and authorize operations. This process relies on secure protocols, such as encryption and PIN verification, to protect sensitive data. For instance, a typical withdrawal involves the ATM deducting funds from the user’s account in real-time, dispensing cash, and updating the account balance instantly. This seamless interaction exemplifies how ATMs integrate with broader banking systems, reducing the need for physical branches and extending service hours to 24/7 availability.

From a practical standpoint, maximizing ATM usage requires awareness of associated fees and security measures. Most banks allow fee-free withdrawals at their own ATMs, but using out-of-network machines can incur charges ranging from $2 to $5 per transaction. To avoid these costs, plan withdrawals in advance or use mobile apps to locate in-network ATMs. Additionally, safeguard against fraud by shielding the keypad when entering your PIN and inspecting the card slot for skimming devices. For older adults or those less tech-savvy, many ATMs feature simplified interfaces or language options to ensure ease of use.

Comparatively, ATMs offer distinct advantages over traditional teller interactions. They eliminate wait times, provide immediate access to cash, and reduce the risk of human error in transactions. However, they lack the personalized advice a human banker can offer, making them unsuitable for complex financial inquiries. For example, while an ATM can facilitate a loan payment, it cannot explain repayment terms or interest rates. Thus, ATMs complement rather than replace human services, catering to routine tasks while freeing bank staff for more specialized roles.

Looking ahead, the future of ATMs lies in innovation. Next-generation machines incorporate biometric authentication, such as fingerprint or facial recognition, to enhance security. Some even support contactless transactions via smartphone apps or NFC technology, catering to the growing preference for digital banking. For instance, certain ATMs now allow users to withdraw cash using QR codes generated on their mobile devices, eliminating the need for physical cards. As these advancements become widespread, ATMs will continue to redefine convenience in banking, bridging the gap between traditional and digital financial services.

Is the AAMC Section Bank C/P Harder? Unpacking the Difficulty

You may want to see also

Explore related products

![]()

Account-to-Account Transfers (ATP)

To execute an ATP, both the sender and recipient must have accounts with banks that support real-time payment systems, such as the UK’s Faster Payments or the U.S. RTP® Network. The sender initiates the transfer by providing the recipient’s account details, typically an account number and sort code or routing number. The transaction is authenticated using secure methods like biometrics or one-time passwords, minimizing the risk of fraud. Businesses can integrate ATP into their platforms via APIs, allowing customers to pay directly from their bank accounts during checkout, bypassing card fees and reducing cart abandonment rates.

One of the standout advantages of ATP is its cost efficiency. Unlike credit card transactions, which incur fees of 2–3% per transaction, ATP fees are significantly lower, often less than 1%. This makes it particularly appealing for high-value transactions or recurring payments. For example, a subscription service can save thousands annually by switching to ATP for customer billing. Additionally, ATP reduces chargeback risks since transactions are irreversible once completed, providing merchants with greater financial security.

However, adopting ATP requires careful consideration of compatibility and user experience. Not all banks or regions support real-time payments, so businesses must ensure their customer base has access to these systems. Moreover, educating users about the benefits and process of ATP is crucial, as many are accustomed to card payments. Providing clear instructions and highlighting the speed and security of ATP can encourage adoption. For instance, a fintech app might offer a step-by-step guide or a video tutorial to onboard users seamlessly.

In conclusion, Account-to-Account Transfers (ATP) represent a transformative shift in payment technology, offering speed, security, and savings for both consumers and businesses. By understanding its mechanics, benefits, and implementation challenges, organizations can leverage ATP to enhance their financial operations and customer experience. As real-time payment infrastructure continues to expand globally, ATP is poised to become the preferred method for moving money in the digital age.

Cash-Basis Companies: Do They Need Bank Reconciliations?

You may want to see also

Explore related products

![]()

Anti-Money Laundering (AML) Compliance

In the realm of banking, ATP often refers to Automated Transaction Processing, a critical function for efficiency. However, when discussing Anti-Money Laundering (AML) Compliance, the focus shifts to a different, yet equally vital, aspect of financial operations. AML compliance is the backbone of a bank’s integrity, ensuring that illicit funds do not infiltrate the financial system. It’s not just about regulatory adherence; it’s about safeguarding the institution’s reputation and contributing to global financial stability.

AML compliance involves a multi-step process that begins with Customer Due Diligence (CDD). Banks must verify the identity of their customers, assess their risk profiles, and monitor transactions for suspicious activity. For instance, a sudden influx of large cash deposits from a low-income individual could trigger an alert. Financial institutions use advanced software to flag such anomalies, but human judgment remains indispensable. A 2022 report by PwC highlighted that 45% of banks increased their AML budgets, emphasizing the growing complexity of compliance.

One of the most challenging aspects of AML compliance is keeping pace with evolving tactics used by money launderers. Criminals exploit gaps in regulatory frameworks and technological vulnerabilities. For example, cryptocurrency has emerged as a new frontier for laundering, with decentralized platforms offering anonymity. Banks must invest in continuous training for their staff and adopt cutting-edge tools like AI-driven transaction monitoring systems. A practical tip: regularly update risk assessment models to reflect emerging threats, such as trade-based money laundering, which accounts for up to 80% of illicit financial flows in some regions.

Non-compliance with AML regulations can result in severe consequences, including hefty fines, loss of banking licenses, and reputational damage. In 2020, a major European bank was fined $1.5 billion for AML failures. To avoid such outcomes, banks should establish a robust compliance framework that includes clear policies, regular audits, and a culture of accountability. A comparative analysis shows that institutions with dedicated AML teams and board-level oversight are 30% less likely to face regulatory penalties.

Finally, AML compliance is not a one-time effort but an ongoing commitment. Banks must balance regulatory demands with customer experience, ensuring that legitimate transactions are not unduly disrupted. For instance, implementing tiered monitoring systems can reduce false positives while maintaining vigilance. The takeaway is clear: effective AML compliance requires a strategic blend of technology, expertise, and adaptability. By prioritizing it, banks not only meet legal obligations but also contribute to a safer financial ecosystem.

Is Indymac Bank's Website a Hidden Online Danger?

You may want to see also

Explore related products

![]()

Available-to-Promise Inventory Management

In the realm of banking, ATP often refers to Available-to-Promise, a concept borrowed from inventory management that has found its way into financial operations. While it may seem out of place, the principle of ATP is increasingly relevant in banking, particularly in managing liquidity, credit lines, and customer commitments. Available-to-Promise Inventory Management (ATP) ensures that what a bank promises to deliver—whether it’s funds, credit, or services—aligns with what is actually available. This precision is critical in maintaining trust and operational efficiency in a sector where over-commitment can lead to financial instability.

Consider a bank managing a pool of funds for loans. ATP systems analyze real-time data to determine how much capital is available for lending after accounting for existing commitments, reserves, and regulatory requirements. For instance, if a bank has $100 million in liquid assets but $30 million is earmarked for existing loans and $20 million must remain in reserve, the ATP system calculates that only $50 million is truly available for new commitments. This granular visibility prevents over-promising and ensures the bank remains solvent while meeting customer needs.

Implementing ATP in banking requires integrating multiple data streams—from customer accounts to market conditions—into a centralized system. Banks must adopt robust software that can process this data in real time, providing accurate ATP figures. For example, a bank might use an ATP module within its core banking system to automatically update available credit limits for customers based on their account activity and the bank’s overall liquidity position. This not only enhances customer experience but also reduces the risk of errors in manual calculations.

One of the key challenges in adopting ATP in banking is balancing accuracy with speed. While real-time data is ideal, delays in updating systems can lead to discrepancies between promised and available resources. Banks must invest in technologies like AI and machine learning to predict fluctuations in liquidity and adjust ATP figures proactively. For instance, if a bank anticipates a surge in loan applications during a holiday season, its ATP system can factor in this demand, ensuring sufficient funds are set aside without over-committing.

In conclusion, Available-to-Promise Inventory Management is not just a logistical tool but a strategic asset for banks. By aligning promises with actual availability, banks can enhance operational efficiency, reduce risk, and build stronger customer relationships. As financial institutions navigate increasingly complex markets, ATP systems will become indispensable in ensuring stability and reliability in every transaction.

SunTrust and Truist: One Bank, Two Names

You may want to see also

Explore related products

![]()

Association for Financial Professionals (AFP) Role

In the realm of banking, ATP often refers to Automated Transaction Processing, a critical function that streamlines financial operations by minimizing manual intervention. However, the Association for Financial Professionals (AFP) plays a distinct yet complementary role in this ecosystem. While ATP focuses on technological efficiency, AFP is dedicated to elevating the expertise and ethical standards of financial professionals themselves. This organization serves as a cornerstone for those who manage cash, investments, and risk within corporate and banking environments.

Consider the AFP as a professional development hub for financial practitioners. It offers certifications like the Certified Treasury Professional (CTP) and Certified Corporate Financial Planning & Analysis Professional (FP&A) credentials, which are widely recognized as benchmarks of competency in the field. These certifications are not just accolades; they equip professionals with the skills to navigate complex financial landscapes, from liquidity management to regulatory compliance. For instance, a CTP-certified individual is better prepared to optimize ATP systems by understanding the interplay between technology and financial strategy.

Beyond certifications, AFP fosters knowledge sharing and networking through its annual conferences, regional events, and digital platforms. These opportunities allow members to exchange insights on emerging trends, such as the integration of artificial intelligence in ATP systems or the impact of real-time payments on cash flow management. By staying ahead of industry shifts, AFP members can ensure their organizations leverage ATP technologies effectively while mitigating associated risks, like cybersecurity threats or operational inefficiencies.

A critical aspect of AFP’s role is its advocacy for ethical practices in financial management. In an era where ATP systems handle trillions of dollars daily, the potential for errors or fraud is significant. AFP promotes frameworks that emphasize transparency, accountability, and risk management, ensuring professionals prioritize integrity in their decision-making. For example, AFP’s Code of Ethics provides guidelines for handling sensitive financial data, a crucial consideration when implementing ATP solutions that process vast amounts of transactional information.

Finally, AFP acts as a bridge between theory and practice, offering resources like whitepapers, case studies, and toolkits that translate complex financial concepts into actionable strategies. This is particularly valuable for professionals tasked with overseeing ATP systems, as it enables them to align technological investments with broader organizational goals. By grounding technical advancements in practical expertise, AFP ensures that ATP is not just a tool but a strategic asset in the financial toolkit. In this way, the organization’s role is indispensable for anyone navigating the intersection of banking technology and financial leadership.

Discover Pinnacle Bank Arena's Seating Capacity and Event Experience

You may want to see also

Frequently asked questions

ATP stands for Automated Trust and Custody Processing in banking, though it can also refer to Available-to-Promise in certain financial contexts.

ATP is used to streamline trust and custody services, automate transaction processing, and ensure accurate record-keeping for assets held in trust or custody accounts.

No, ATP in banking does not refer to Adenosine Triphosphate, which is a biological term. In banking, ATP specifically relates to financial processes and systems.