CLTV, or Combined Loan-to-Value, is a critical metric used in banking and finance to assess the risk associated with lending, particularly in the context of mortgages and home equity loans. It represents the total percentage of a property's value that is financed by all outstanding loans secured by the property, including the primary mortgage and any secondary liens such as home equity lines of credit (HELOCs) or second mortgages. Lenders use CLTV to evaluate the borrower's equity position and the potential risk of default, as higher CLTV ratios indicate a greater financial exposure for the lender. Understanding CLTV is essential for both borrowers and lenders, as it influences loan approval, interest rates, and overall borrowing capacity in real estate transactions.

Explore related products

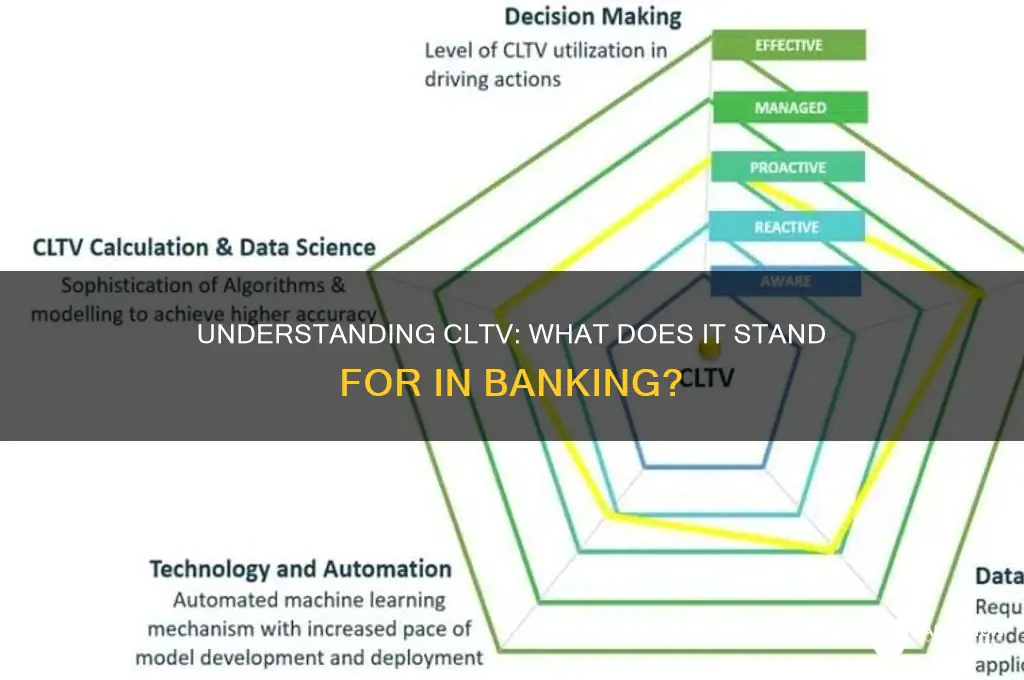

What You'll Learn

- CLTV Definition: Customer Lifetime Value measures total revenue from a customer over their banking relationship

- CLTV Calculation: Formula uses average purchase value, purchase frequency, and customer lifespan

- CLTV in Lending: Banks use CLTV to assess loan risks and determine credit limits

- CLTV vs LTV: CLTV focuses on long-term value, while LTV assesses short-term loan-to-value ratios

- CLTV Applications: Helps banks in customer segmentation, marketing strategies, and profitability analysis

![]()

CLTV Definition: Customer Lifetime Value measures total revenue from a customer over their banking relationship

In banking, CLTV stands for Customer Lifetime Value, a metric that quantifies the total revenue a financial institution can expect from a customer throughout their entire relationship. This isn’t just about a single transaction or product; it’s a forward-looking calculation that considers all potential revenue streams, from checking account fees to loan interest and investment management. For instance, a customer who starts with a basic savings account might later take out a mortgage, open a credit card, and invest in a retirement fund—all contributing to their CLTV. By understanding this metric, banks can tailor their strategies to maximize long-term profitability while meeting customer needs.

To calculate CLTV, banks analyze historical data, customer behavior, and predictive models. The formula typically includes average purchase value, purchase frequency, and customer lifespan. For example, if a customer spends $500 annually on banking services and is expected to remain with the bank for 20 years, their CLTV would be $10,000. However, this is a simplified view; advanced models factor in churn rates, cross-selling opportunities, and even the potential for referrals. Banks often segment customers based on CLTV to prioritize high-value clients, offering them personalized services or loyalty programs to retain their business.

One practical application of CLTV is in resource allocation. Banks with limited marketing budgets can focus on acquiring customers with higher predicted lifetime values rather than chasing short-term gains. For instance, a customer likely to take out a mortgage and invest in wealth management products is more valuable than one who only maintains a low-balance checking account. Similarly, CLTV helps banks decide when to invest in customer retention. If a high-value customer is at risk of leaving, the bank might offer incentives like waived fees or premium services to keep them.

Despite its utility, CLTV isn’t without challenges. Predicting customer behavior over decades is inherently uncertain, and external factors like economic downturns can skew projections. Additionally, over-reliance on CLTV can lead banks to neglect lower-value customers who might still contribute meaningfully over time. To mitigate these risks, banks should regularly update their CLTV models with fresh data and adopt a balanced approach that values all customers while prioritizing those with the highest potential.

In conclusion, CLTV is a powerful tool for banks to optimize their customer relationships and financial performance. By focusing on long-term revenue potential, banks can make smarter decisions about acquisition, retention, and service offerings. While it requires robust data and careful interpretation, the insights gained from CLTV can drive sustainable growth and customer satisfaction. For banks looking to thrive in a competitive market, mastering this metric is not just beneficial—it’s essential.

ExamSoft and NCLEX Test Banks: Are They Included Together?

You may want to see also

Explore related products

![]()

CLTV Calculation: Formula uses average purchase value, purchase frequency, and customer lifespan

In banking, CLTV stands for Customer Lifetime Value, a metric that predicts the total revenue a customer will generate over their entire relationship with a financial institution. Understanding CLTV is crucial for banks to optimize marketing strategies, tailor product offerings, and allocate resources effectively. At its core, CLTV calculation hinges on three key variables: average purchase value, purchase frequency, and customer lifespan. These elements collectively paint a picture of a customer’s long-term profitability, enabling banks to make data-driven decisions.

To calculate CLTV, start by determining the average purchase value (APV), which represents the typical transaction amount a customer makes. For instance, if a customer regularly deposits $1,000 monthly into a savings account, their APV is $1,000. Next, assess purchase frequency (PF), or how often the customer engages in transactions. In this example, the frequency is 12 times per year. Multiply APV by PF to find the annual customer value (ACV): $1,000 × 12 = $12,000. This figure reflects the customer’s yearly contribution.

The final step involves factoring in customer lifespan (CL), the estimated duration of the customer’s relationship with the bank. Suppose the average customer stays with the bank for 5 years. Multiply the ACV by the CL to arrive at the CLTV: $12,000 × 5 = $60,000. This calculation reveals the total revenue the bank can expect from this customer over their lifetime. However, for a more accurate prediction, banks often incorporate discount rates to account for the time value of money, adjusting future cash flows to present value.

While the formula appears straightforward, its application requires careful consideration. For example, APV and PF can fluctuate based on economic conditions or changes in customer behavior. Banks must regularly update these variables to maintain accuracy. Additionally, estimating customer lifespan can be challenging, as it depends on factors like customer satisfaction, market competition, and product relevance. Leveraging predictive analytics and customer segmentation can enhance the precision of CLTV calculations, allowing banks to identify high-value customers and tailor retention strategies accordingly.

In practice, CLTV serves as a strategic tool for banks to prioritize customer segments, optimize marketing budgets, and design personalized financial products. For instance, a bank might allocate more resources to retaining customers with a high CLTV by offering exclusive services or loyalty programs. Conversely, understanding low-CLTV segments can help banks refine acquisition strategies or improve product offerings. By mastering CLTV calculation, banks can foster long-term profitability while delivering value to their customers, creating a win-win scenario in the competitive financial landscape.

Step-by-Step Guide to Applying for SSY in ICICI Bank

You may want to see also

Explore related products

![]()

CLTV in Lending: Banks use CLTV to assess loan risks and determine credit limits

In the realm of banking, CLTV, or Combined Loan-to-Value, is a critical metric that lenders use to evaluate the risk associated with a loan. This ratio compares the total amount of loans secured by a property to the property's appraised value. For instance, if a borrower has a $200,000 mortgage and a $50,000 home equity line of credit (HELOC) on a property appraised at $300,000, the CLTV would be 83.3% (($200,000 + $50,000) / $300,000). Banks typically set maximum CLTV thresholds, often ranging from 80% to 90%, beyond which they consider the loan riskier. Exceeding these limits may result in higher interest rates, additional fees, or loan denial.

From an analytical perspective, CLTV serves as a safeguard for banks by quantifying the potential loss in the event of default. A lower CLTV indicates a larger equity cushion, reducing the lender's exposure. For example, a CLTV of 70% means the borrower has 30% equity in the property, providing a buffer against market fluctuations. Lenders often use this metric in conjunction with other risk factors, such as credit scores and debt-to-income ratios, to make informed decisions. Borrowers with a CLTV below the bank's threshold are more likely to secure favorable terms, as they pose less risk to the lender.

To illustrate the practical application of CLTV, consider a homeowner seeking a cash-out refinance. Suppose they owe $150,000 on a property worth $250,000 and want to borrow an additional $30,000. The new loan amount would be $180,000, resulting in a CLTV of 72% ($180,000 / $250,000). If the bank's maximum CLTV is 80%, this borrower would likely qualify. However, if they requested $50,000, the CLTV would rise to 80% ($200,000 / $250,000), pushing them to the limit. In this scenario, the bank might approve the loan but impose stricter conditions, such as a higher interest rate or private mortgage insurance (PMI).

A persuasive argument for borrowers is that understanding CLTV can help them strategize when applying for loans. For instance, paying down existing debt or increasing property value through renovations can lower the CLTV, improving the chances of approval and securing better terms. Additionally, borrowers should be cautious of taking on multiple loans that cumulatively exceed their bank's CLTV threshold. For example, a homeowner with a mortgage and a HELOC should monitor their combined balances relative to their property's value to avoid triggering higher costs or rejections on future loan applications.

In conclusion, CLTV is a pivotal tool in lending that banks use to manage risk and determine credit limits. By calculating the ratio of total secured debt to property value, lenders assess their exposure and set terms accordingly. Borrowers who grasp the significance of CLTV can take proactive steps to improve their financial position, such as reducing debt or enhancing property value. This knowledge empowers them to navigate the lending process more effectively, ensuring they secure the best possible terms for their financial needs.

Is Bank of Scotland Affiliated with HSBC? Unraveling the Connection

You may want to see also

![]()

CLTV vs LTV: CLTV focuses on long-term value, while LTV assesses short-term loan-to-value ratios

In banking, CLTV (Combined Loan-to-Value) and LTV (Loan-to-Value) are critical metrics for assessing risk and value, but they serve distinct purposes. CLTV evaluates the total debt secured by a property relative to its appraised value, considering all liens, including first and second mortgages or home equity lines of credit (HELOCs). For instance, if a homeowner has a $200,000 first mortgage and a $50,000 HELOC on a $300,000 property, the CLTV is 83.3% ($250,000 / $300,000). This metric is essential for lenders to gauge long-term risk, as it reflects the cumulative financial exposure tied to the asset.

LTV, in contrast, focuses solely on the primary mortgage or loan amount relative to the property’s value. Using the same example, the LTV for the first mortgage would be 66.7% ($200,000 / $300,000). LTV is a short-term snapshot, often used to determine eligibility for loans or refinancing. Lenders typically cap LTV at 80% for conventional loans to minimize risk, while CLTV limits may extend to 90% or higher, depending on the borrower’s creditworthiness and the lender’s policies. Understanding these thresholds is crucial for borrowers seeking to maximize their financing options.

The key difference lies in their scope and application. CLTV provides a comprehensive view of a property’s encumbrances, making it a long-term risk assessment tool. LTV, however, is a more immediate measure, used to evaluate the viability of a single loan. For example, a borrower with a high CLTV may struggle to secure additional financing, even if their LTV on a new loan is within acceptable limits. This distinction highlights why lenders scrutinize both metrics: CLTV ensures the property isn’t overleveraged, while LTV assesses the affordability and risk of the specific loan in question.

Practical tips for borrowers include monitoring both ratios to maintain financial flexibility. Refinancing to consolidate debt can lower CLTV, while increasing property value through renovations or market appreciation can improve both metrics. For lenders, balancing CLTV and LTV thresholds ensures a portfolio’s stability without unnecessarily restricting borrower access to credit. In essence, while LTV is a snapshot of current risk, CLTV is a forward-looking measure of long-term financial health, making both indispensable in banking.

Is the NCAA Game Hosted in the US Bank Stadium?

You may want to see also

![]()

CLTV Applications: Helps banks in customer segmentation, marketing strategies, and profitability analysis

In banking, CLTV stands for Customer Lifetime Value, a metric that quantifies the total revenue a bank can expect from a single customer throughout their relationship. This metric is pivotal for banks aiming to optimize their operations and enhance profitability. By understanding CLTV, banks can make informed decisions about resource allocation, customer retention, and acquisition strategies. Here’s how CLTV applications specifically aid in customer segmentation, marketing strategies, and profitability analysis.

Customer Segmentation: Tailoring Services to Maximize Value

CLTV enables banks to segment customers based on their long-term value, allowing for personalized service offerings. For instance, high-CLTV customers, who typically include affluent individuals or businesses with substantial transaction volumes, can be targeted with premium services like wealth management or exclusive loan products. Conversely, low-CLTV customers might benefit from cost-effective digital banking solutions or introductory offers to increase their engagement. By categorizing customers into distinct segments, banks can allocate resources efficiently, ensuring high-value customers receive dedicated attention while optimizing costs for lower-value segments.

Marketing Strategies: Precision in Acquisition and Retention

CLTV informs marketing strategies by identifying the most profitable customer profiles. Banks can use this data to design targeted campaigns that attract high-CLTV prospects. For example, if analysis reveals that young professionals with a high savings rate tend to have a higher CLTV, marketing efforts can focus on this demographic through tailored ads, social media campaigns, or referral programs. Additionally, CLTV helps in retention by identifying at-risk customers whose value is declining. Proactive measures, such as personalized incentives or improved customer service, can then be implemented to prevent churn and maintain profitability.

Profitability Analysis: Balancing Costs and Revenue

CLTV is a critical tool for profitability analysis, as it provides a clear picture of the net value each customer brings to the bank. By comparing CLTV with customer acquisition costs (CAC), banks can assess the efficiency of their marketing spend. A healthy CLTV-to-CAC ratio (ideally 3:1 or higher) indicates that the bank is acquiring customers at a sustainable cost. Furthermore, CLTV analysis helps identify unprofitable customer segments or products that may be draining resources. For instance, if a specific loan product attracts customers with a low CLTV, the bank might reconsider its terms or phase it out entirely to improve overall profitability.

Practical Implementation: Steps and Cautions

To leverage CLTV effectively, banks should follow a structured approach. First, gather comprehensive customer data, including transaction history, product usage, and demographic information. Next, employ predictive analytics to estimate future revenue streams and calculate CLTV. Caution must be exercised to avoid over-reliance on historical data, as customer behavior can change due to external factors like economic shifts or technological advancements. Regularly update CLTV models to reflect current trends and ensure accuracy. Finally, integrate CLTV insights into decision-making processes across departments, from marketing to product development, to maximize its impact.

In conclusion, CLTV applications empower banks to segment customers strategically, refine marketing efforts, and conduct robust profitability analyses. By focusing on this metric, banks can foster long-term customer relationships, optimize resource allocation, and ultimately drive sustainable growth.

Understanding the Key Functions and Responsibilities of a Banker

You may want to see also

Frequently asked questions

CLTV stands for Combined Loan-to-Value, a ratio used to assess the total amount of loans secured by a property relative to its appraised value.

CLTV is calculated by dividing the sum of all loans secured by the property (e.g., primary mortgage, home equity loans) by the property's appraised value, then multiplying by 100 to get a percentage.

CLTV is important because it helps lenders evaluate risk by determining how much debt is tied to a property. A higher CLTV indicates higher risk for the lender.

Most banks typically accept a maximum CLTV ratio of 80-90%, depending on the loan type and lender policies. Higher ratios may require additional conditions or mortgage insurance.