In the banking sector, ERD stands for Expected Remittance Date, a critical term used in international trade finance to denote the anticipated date by which a payment is expected to be received from the importer’s bank. This date is crucial for exporters and financial institutions as it ensures timely settlement of transactions, particularly in letter of credit (LC) operations. The ERD helps in managing cash flow, mitigating risks, and maintaining transparency in cross-border trade, making it an essential component of global banking and trade finance processes.

Explore related products

![Database Design Using Entity-Relationship Diagrams (03) by [Hardcover (2003)]](https://m.media-amazon.com/images/I/31PncsZKvRL._AC_UY218_.jpg)

What You'll Learn

![]()

Entity Relationship Diagram Basics

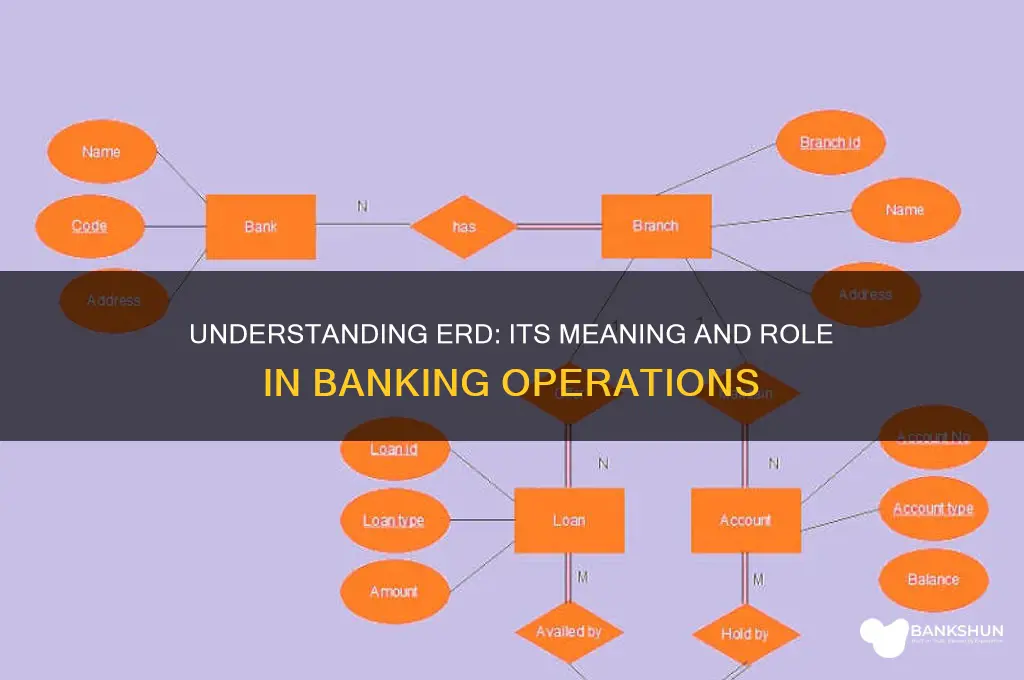

In banking, ERD stands for Entity Relationship Diagram, a visual tool that maps the relationships between different data entities within a system. Think of it as a blueprint for how customer information, accounts, transactions, and other critical data points interconnect.

For instance, an ERD would illustrate how a "Customer" entity relates to an "Account" entity, and how "Transactions" are linked to both. This clarity is essential for designing efficient databases, ensuring data integrity, and streamlining processes like loan approvals or fraud detection.

Without a well-structured ERD, banking systems risk data inconsistencies, redundant information, and operational inefficiencies.

Let's break down the core components of an ERD. Entities represent real-world objects like "Customer," "Loan," or "Branch." Attributes define the properties of these entities – a "Customer" might have attributes like "Name," "SSN," and "Address." Relationships depict how entities interact. For example, a "Customer" can have "many" accounts, while an "Account" belongs to "one" customer. These relationships are often described as one-to-one, one-to-many, or many-to-many. Cardinality specifies the exact number of occurrences in a relationship. A customer can have "zero or more" loans, but a loan must always be associated with "one" customer.

Creating an ERD involves a systematic approach. Start by identifying the key entities relevant to your banking process. Next, define the attributes for each entity, ensuring they are atomic (indivisible) and relevant. Then, establish the relationships between entities, carefully considering cardinality and optionality. Tools like Lucidchart, Draw.io, or even pen and paper can be used to visually represent these relationships using standardized symbols. Remember, simplicity is key – avoid overcomplicating the diagram with unnecessary details.

Regularly review and refine your ERD as your banking system evolves, ensuring it remains an accurate reflection of your data structure.

While ERDs are powerful tools, they have limitations. They primarily focus on the structure of data, not its behavior or business logic. They don't capture temporal aspects, such as how data changes over time. Additionally, ERDs can become complex and difficult to interpret for large, intricate systems. To mitigate these challenges, consider using complementary modeling techniques like data flow diagrams or state diagrams. Remember, an ERD is a living document – it should evolve alongside your banking system, reflecting changes in data requirements and business processes. By understanding these basics and adapting them to your specific needs, you can leverage ERDs to build robust and efficient banking systems.

Creating Your Own UTAU Voice Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

ERD Role in Banking Systems

ERD, or Entity-Relationship Diagram, serves as a cornerstone in banking systems by visually mapping complex relationships between entities like customers, accounts, and transactions. This blueprint clarifies how data interacts, ensuring systems are designed with precision and scalability. For instance, an ERD might illustrate how a single customer can hold multiple accounts, each with distinct transaction histories, all linked through unique identifiers. This clarity is critical in banking, where accuracy and integrity of data directly impact financial operations and regulatory compliance.

Consider the process of implementing a new banking software. An ERD acts as a shared language between developers, analysts, and stakeholders, reducing misunderstandings and aligning expectations. It identifies key attributes—such as account balances, transaction dates, and customer IDs—and defines relationships like "one-to-many" or "many-to-many." For example, a customer (one) can have multiple loans (many), but each loan must be tied to a specific account. This structured approach minimizes errors during development and ensures the system can handle future expansions, such as integrating new product lines or regulatory requirements.

However, creating an effective ERD in banking isn’t without challenges. Banks must balance granularity with simplicity. Overly complex diagrams can overwhelm users, while oversimplified ones may omit critical details. For instance, including every possible transaction type (e.g., deposits, withdrawals, transfers) in a single diagram can clutter the view, but excluding key types risks incomplete system design. Best practices include prioritizing core entities and relationships first, then layering additional details as needed. Tools like normalization techniques help refine the ERD, ensuring data redundancy is minimized and performance optimized.

The role of ERD extends beyond initial system design; it’s a living document that evolves with the bank’s needs. During system upgrades or mergers, an ERD helps identify data integration points and potential conflicts. For example, when merging two banks, the ERD can highlight discrepancies in how customer data is structured, enabling smoother consolidation. Regular reviews of the ERD also ensure it remains aligned with business processes, reducing the risk of data silos or inconsistencies that could lead to financial discrepancies or compliance issues.

In practice, banks can maximize the utility of ERDs by involving cross-functional teams in their creation and maintenance. IT teams should collaborate with business analysts and compliance officers to ensure the diagram reflects both technical capabilities and regulatory mandates. Additionally, leveraging ERD tools integrated with database management systems allows for automated validation of the model against actual data, catching discrepancies early. By treating the ERD as a strategic asset rather than a one-time deliverable, banks can build systems that are robust, adaptable, and aligned with long-term goals.

Exploring Union Bank's Presence in Alabama: Locations and Services

You may want to see also

Explore related products

![]()

Key Components of Banking ERDs

In banking, ERD stands for Entity-Relationship Diagram, a visual tool that maps out the relationships between different data entities within a system. When designing a banking ERD, several key components must be included to ensure accuracy and functionality. These components serve as the building blocks for a comprehensive understanding of the bank's data structure.

Entities and Attributes form the foundation of any ERD. In a banking context, entities may include customers, accounts, transactions, loans, and branches. Each entity has specific attributes, such as customer ID, account number, transaction date, loan amount, and branch location. For instance, a customer entity might have attributes like name, address, and date of birth. Clearly defining these entities and their attributes is crucial, as it establishes the data framework and enables efficient information retrieval. A well-designed ERD should include a detailed list of entities and their corresponding attributes, ensuring that all relevant data points are captured.

The relationships between entities are another critical aspect of banking ERDs. These relationships illustrate how different entities interact and connect within the system. For example, a customer can have multiple accounts, and an account can be associated with numerous transactions. Relationships can be one-to-one, one-to-many, or many-to-many, each represented by specific notations in the ERD. Consider a scenario where a bank wants to analyze customer behavior; understanding the relationship between customers and their transactions is essential. By mapping these relationships, banks can identify patterns, such as frequent transactions or account linkages, which can inform decision-making and risk assessment.

Cardinality and Optionality are essential concepts to convey the nature of relationships in an ERD. Cardinality defines the numerical relationship between entities, such as one customer having multiple accounts (one-to-many). Optionality indicates whether an entity's participation in a relationship is mandatory or optional. For instance, a customer may optionally have a loan, but every loan must be associated with a customer. These specifications ensure data integrity and provide constraints for the system. When creating a banking ERD, it's vital to accurately represent cardinality and optionality to reflect the real-world rules and limitations of the banking system.

In addition to these components, normalization techniques play a significant role in optimizing banking ERDs. Normalization involves organizing data to minimize redundancy and improve data integrity. This process includes breaking down data into smaller, well-structured tables and establishing relationships between them. For example, separating customer information from account details allows for efficient updates and reduces data duplication. Normalization ensures that the ERD adheres to industry standards and best practices, making it easier to maintain and scale the database as the bank's operations grow.

By incorporating these key components, banking ERDs become powerful tools for data modeling and system design. They provide a clear visual representation of complex banking systems, enabling stakeholders to understand data flow, identify potential issues, and make informed decisions. Whether it's optimizing customer data management or streamlining transaction processes, a well-structured ERD is an invaluable asset for any banking institution's digital infrastructure.

Efficiently Remove Bank Rows in Excel: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

ERD vs. Other Banking Models

ERD, or Emergency Relief Disbursement, is a specialized banking model designed to provide rapid financial assistance during crises. Unlike traditional banking models, which focus on long-term lending, savings, or investment, ERD systems prioritize speed, accessibility, and targeted relief. For instance, during natural disasters or economic downturns, ERD mechanisms can disburse funds within hours, bypassing the bureaucratic delays common in conventional banking. This immediacy is achieved through pre-approved beneficiary lists, digital payment systems, and partnerships with local governments or NGOs. While traditional models excel in stability and growth, ERD shines in its ability to address urgent, short-term needs, making it a complementary rather than competing framework.

Consider the operational differences between ERD and microfinance models. Microfinance institutions typically offer small loans to low-income individuals, fostering entrepreneurship and self-sufficiency over time. In contrast, ERD is not about repayment or creditworthiness; it’s about survival. For example, during the COVID-19 pandemic, ERD programs distributed direct cash transfers to vulnerable populations without requiring repayment. Microfinance, while valuable for long-term economic development, lacks the agility to respond to sudden, large-scale emergencies. ERD fills this gap by acting as a financial first-aid kit, ensuring immediate liquidity when traditional lending mechanisms fall short.

From a technological standpoint, ERD leverages digital infrastructure in ways that other banking models are still catching up to. Mobile money platforms, biometric verification, and blockchain technology enable ERD systems to reach remote or unbanked populations efficiently. For instance, in Kenya, M-Pesa has been instrumental in delivering ERD funds during droughts and floods. Traditional banks, often reliant on physical branches and manual processes, struggle to replicate this level of accessibility. However, this reliance on technology also poses risks, such as cybersecurity threats or digital exclusion of tech-illiterate populations, which must be mitigated through robust safeguards.

A persuasive argument for ERD lies in its cost-effectiveness during crises. By providing timely financial aid, ERD reduces the long-term economic burden on governments and communities. For example, a study by the World Bank found that every $1 spent on ERD during a disaster saves $7 in recovery costs. Traditional banking models, focused on profit margins and risk management, often fail to account for these societal savings. Policymakers should view ERD not as a competitor but as a critical tool in a broader financial ecosystem, one that enhances resilience and minimizes the cascading effects of emergencies.

Finally, the scalability of ERD sets it apart from other banking models. While traditional banks and even microfinance institutions often struggle to expand rapidly during crises, ERD systems are designed for flexibility. For instance, during the 2010 Haiti earthquake, ERD programs scaled up within days to serve millions of affected individuals. This scalability is achieved through modular designs, pre-established protocols, and cross-sector collaborations. By contrast, other models require time-consuming adjustments to infrastructure and policy, making them less effective in emergency scenarios. ERD’s unique ability to adapt quickly underscores its indispensable role in modern banking.

Lloyds Bank in Malta: Exploring Availability and Banking Options

You may want to see also

![]()

Benefits of Using ERDs in Banking

In banking, ERD stands for Entity-Relationship Diagram, a visual tool that maps out the relationships between different data entities within a system. While it might seem like a technical concept, ERDs offer a surprising number of benefits for banks, streamlining operations and improving overall efficiency.

Let's delve into why they're a game-changer.

Clarity and Communication: Imagine trying to explain a complex loan application process to a new team member using only text. ERDs act as a universal language, providing a clear, visual representation of how customer data, loan products, and approval workflows interconnect. This shared understanding fosters better communication between IT teams, business analysts, and stakeholders, leading to faster project completion and reduced errors.

Think of it as a blueprint for your bank's data landscape, ensuring everyone is on the same page.

Identifying Inefficiencies and Redundancies: ERDs don't just map existing systems; they reveal hidden inefficiencies. By visualizing data flow, banks can pinpoint redundant data entry points, unnecessary steps in processes, and potential bottlenecks. For example, an ERD might highlight that customer information is being entered separately in both the loan origination system and the customer relationship management (CRM) platform, leading to wasted time and potential data inconsistencies. This visual insight allows banks to streamline processes, automate tasks, and ultimately improve customer service.

Think of it as a diagnostic tool for your bank's data health.

Facilitating System Design and Development: Building new banking applications or integrating new technologies requires a solid understanding of existing data structures. ERDs provide a foundation for system design, guiding developers in creating applications that seamlessly interact with existing data. They ensure data integrity, prevent compatibility issues, and accelerate development timelines. Imagine constructing a building without blueprints – ERDs provide the essential framework for building robust and efficient banking systems.

Regulatory Compliance and Risk Management: The banking industry is heavily regulated, with stringent data privacy and security requirements. ERDs play a crucial role in demonstrating compliance by clearly showing how sensitive customer data is stored, accessed, and protected. They also aid in risk management by identifying potential vulnerabilities in data flow and access points, allowing banks to implement necessary security measures.

In essence, ERDs are not just technical diagrams; they are powerful tools for banks to achieve greater transparency, efficiency, and security in their operations. By leveraging the benefits of ERDs, banks can navigate the complexities of modern financial systems with confidence and agility.

Mastering Lakshmi Vilas Bank PO Exam: Strategies for Success

You may want to see also

Frequently asked questions

ERD stands for Early Repayment Date in banking, referring to the date when a borrower can repay a loan or debt before the scheduled maturity date without incurring penalties.

The ERD is the date when early repayment is allowed, while the loan maturity date is the final due date for repayment as per the original loan agreement.

Typically, no penalties are applied for repaying a loan on or after the ERD, but penalties may apply if repayment occurs before the ERD.

ERD is important because it provides borrowers flexibility to repay loans early without penalties, while also protecting lenders by ensuring they receive a minimum interest income before early repayment is allowed.