FICO, an acronym for Fair Isaac Corporation, is a widely recognized term in the banking and financial sectors, primarily associated with credit scoring. It refers to a company that developed a proprietary credit scoring model used by lenders to assess an individual's creditworthiness. The FICO score is a three-digit number, ranging from 300 to 850, that summarizes a person's credit history and is a critical factor in determining loan approvals, interest rates, and credit limits. This scoring system has become an industry standard, helping banks and financial institutions make informed decisions about extending credit to consumers. Understanding what FICO stands for is essential for anyone navigating the world of personal finance and credit management.

Explore related products

![What the Fico( 12 Steps to Repairing Your Credit)[WHAT THE FICO][Paperback]](https://m.media-amazon.com/images/I/41NX51g9r7L._AC_UY218_.jpg)

What You'll Learn

- FICO Score Meaning: FICO stands for Fair Isaac Corporation, a credit scoring model used in banking

- FICO Score Range: Scores range from 300 to 850, indicating creditworthiness for lenders

- FICO vs. Credit Reports: FICO scores are derived from credit reports, summarizing financial health

- Importance in Banking: Banks use FICO scores to assess loan, credit card, and mortgage risks

- Improving FICO Scores: Pay bills on time, reduce debt, and monitor credit to boost scores

![]()

FICO Score Meaning: FICO stands for Fair Isaac Corporation, a credit scoring model used in banking

FICO, an acronym for Fair Isaac Corporation, is the backbone of credit scoring in the banking industry. This three-digit number, ranging from 300 to 850, is a snapshot of an individual’s creditworthiness, distilled from their financial history. Lenders rely on it to assess risk, determine loan approvals, and set interest rates. Understanding what FICO stands for isn’t just trivia—it’s the first step in demystifying how banks evaluate your financial trustworthiness.

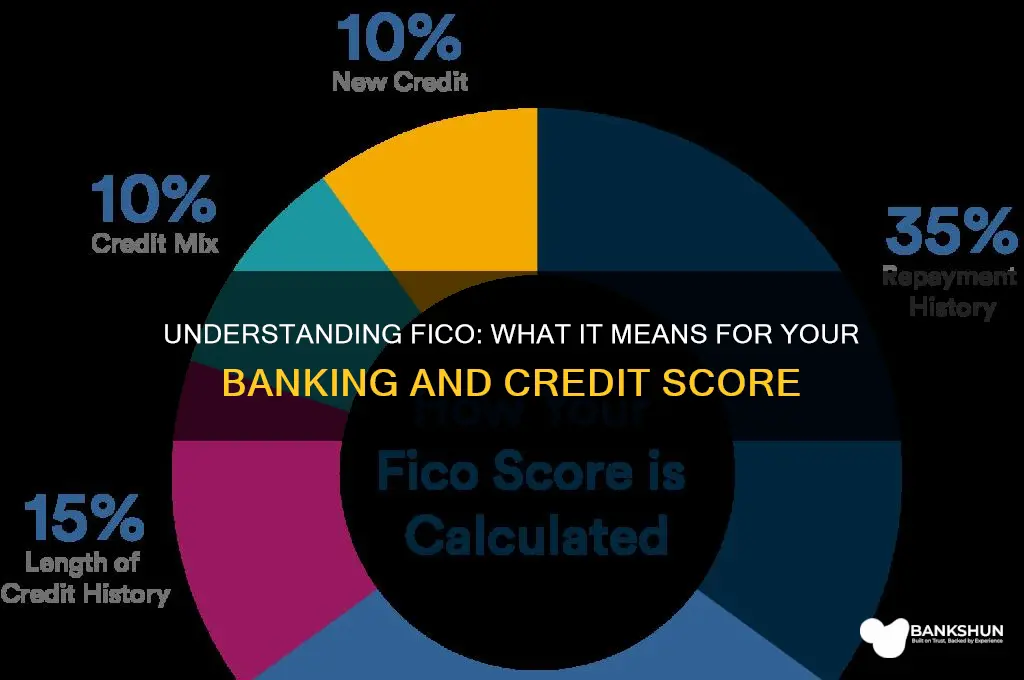

To calculate a FICO score, the Fair Isaac Corporation uses a proprietary algorithm that weighs five key factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%). For example, consistently paying bills on time boosts your score, while maxing out credit cards or frequently opening new accounts can lower it. Knowing these weights allows you to strategically improve your score, such as by reducing debt or avoiding unnecessary credit inquiries.

Comparatively, FICO scores are not the only credit scoring models, but they are the most widely used in banking. Alternatives like VantageScore exist, but 90% of top lenders prefer FICO due to its long-standing reputation and predictive accuracy. This dominance means that, whether you’re applying for a mortgage, auto loan, or credit card, your FICO score is likely the deciding factor. It’s a standardized language banks use to communicate risk, making it essential for anyone navigating the financial system.

Practically, monitoring your FICO score is as crucial as checking your bank balance. Free tools like credit card issuer portals or services like Credit Karma offer regular updates, but for the most accurate report, purchase it directly from myFICO.com. Aim for a score above 740 to qualify for the best interest rates, and if your score is below 670, focus on paying down debt and correcting errors on your credit report. Small actions, like setting payment reminders or keeping credit card balances under 30% of their limit, can yield significant improvements over time.

In essence, FICO stands for more than just a company—it represents a critical tool in the banking ecosystem. By understanding its meaning and mechanics, you gain control over your financial narrative. It’s not just a number; it’s a reflection of your financial habits and a key to unlocking opportunities. Treat it with care, and it will open doors to better rates, approvals, and long-term financial health.

Second Chance Banking: Rebuilding Financial Trust and Opportunities

You may want to see also

Explore related products

![]()

FICO Score Range: Scores range from 300 to 850, indicating creditworthiness for lenders

FICO, an acronym for Fair Isaac Corporation, is a critical player in the banking and financial sectors, primarily known for its credit scoring model. The FICO score range, spanning from 300 to 850, serves as a standardized measure of an individual's creditworthiness, providing lenders with a quick assessment of the risk associated with extending credit. This range is not arbitrary; it is a carefully calibrated scale that reflects a borrower's credit history, payment behavior, and overall financial responsibility.

Consider the FICO score range as a financial report card, where each score bracket corresponds to a distinct level of credit risk. Scores below 580 are generally classified as poor, indicating a higher likelihood of default. Lenders may be hesitant to approve loans for individuals in this range, and if they do, the terms are often less favorable, with higher interest rates and stricter conditions. On the opposite end, scores above 800 are considered exceptional, signaling to lenders that the borrower is highly reliable and poses minimal risk. These individuals typically enjoy the best loan terms, including lower interest rates and more flexible repayment options.

The distribution of scores within this range is not linear but rather follows a bell curve, with the majority of consumers falling in the 'fair' to 'very good' categories (580-799). This segment represents the average credit risk and is where most lending decisions are made. For instance, a score of 670 might qualify someone for a mortgage but at a slightly higher interest rate compared to someone with a score of 750. Understanding where you fall within this range is crucial for managing financial expectations and planning.

Improving one's FICO score is a practical goal for many, especially those aiming to secure better loan terms. The journey from a 'fair' to 'very good' score, or even to the exceptional range, involves consistent financial habits. Key strategies include paying bills on time, reducing credit card balances, and avoiding new credit inquiries. For example, paying down credit card debt to below 30% of the total credit limit can significantly boost a score. Additionally, regularly checking credit reports for errors and disputing inaccuracies can also contribute to score improvement.

In the context of lending, the FICO score range is a powerful tool for both borrowers and lenders. For borrowers, it provides a clear target for financial improvement, with each score bracket offering a distinct set of opportunities and challenges. Lenders, on the other hand, use this range to streamline their risk assessment processes, making lending decisions more efficient and consistent. By understanding and strategically navigating the FICO score range, individuals can enhance their financial profiles, while lenders can optimize their portfolios, ensuring a healthier financial ecosystem.

Mastering the Art of Robbing a Bank: A Board Game Guide

You may want to see also

Explore related products

![]()

FICO vs. Credit Reports: FICO scores are derived from credit reports, summarizing financial health

FICO scores and credit reports are often conflated, yet they serve distinct roles in assessing financial health. A FICO score is a three-digit number, ranging from 300 to 850, that distills the information in a credit report into a single metric. Think of the credit report as a detailed financial biography—listing loans, credit cards, payment history, and public records—while the FICO score is the CliffsNotes version, summarizing that data into a predictive risk assessment for lenders. For instance, a credit report might show you’ve had a credit card for five years with occasional late payments, but your FICO score quantifies how those details impact your creditworthiness.

To understand the relationship, consider the process: FICO scores are derived from five key factors in a credit report—payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%). Each factor is weighted based on its historical correlation with repayment behavior. For example, a missed mortgage payment will weigh more heavily than a late utility bill because it reflects a higher financial commitment. Lenders use FICO scores as a quick reference to gauge risk, but they often review the full credit report for context, such as recent improvements or isolated errors.

A common misconception is that a high FICO score guarantees loan approval, but this isn’t always the case. While a score above 740 is generally considered excellent, lenders also scrutinize the credit report for red flags like high debt-to-income ratios or frequent credit inquiries. Conversely, a low FICO score doesn’t necessarily mean you’re unlendable—if your credit report shows consistent on-time payments and a low credit utilization rate, lenders might overlook a temporary dip. This interplay highlights why both the score and the report matter.

Practical tip: Regularly review your credit report for inaccuracies, as errors can artificially lower your FICO score. For instance, a misreported late payment or an account that isn’t yours can drag down your score by 50–100 points. Dispute errors through the credit bureaus (Experian, TransUnion, Equifax) and monitor your FICO score monthly, especially if you’re planning to apply for a mortgage or auto loan. Tools like annualcreditreport.com offer free reports, while services like myFICO provide score tracking for a fee.

In essence, FICO scores and credit reports are two sides of the same coin. The report provides the raw data, while the score interprets it into actionable insight. By understanding this dynamic, you can strategically manage your credit—paying down balances to improve your "amounts owed" factor, avoiding new credit applications before major loans, and ensuring timely payments to bolster your history. Together, they offer a comprehensive view of your financial health, empowering you to make informed decisions and achieve your financial goals.

Is GPE Affiliated with the World Bank? Exploring the Connection

You may want to see also

Explore related products

![]()

Importance in Banking: Banks use FICO scores to assess loan, credit card, and mortgage risks

FICO, an acronym for Fair Isaac Corporation, is a critical tool in the banking industry, representing a numerical summary of an individual's creditworthiness. This three-digit score, ranging from 300 to 850, serves as a snapshot of a person's financial reliability, influencing their access to loans, credit cards, and mortgages. In the realm of banking, FICO scores are indispensable for assessing risk, ensuring that financial institutions make informed decisions when extending credit.

Consider the process of applying for a mortgage. Banks must evaluate the likelihood of a borrower repaying the loan over an extended period. A FICO score provides a concise, standardized measure of this risk. For instance, a score above 740 is generally considered excellent, indicating a low risk of default. Conversely, scores below 580 may signal higher risk, prompting banks to either deny the loan or offer it at a higher interest rate. This risk-based pricing ensures that banks can manage their portfolios effectively while providing borrowers with tailored financial products.

The importance of FICO scores extends beyond mortgages to credit cards and personal loans. For credit card issuers, these scores help determine not only approval but also credit limits and interest rates. A higher FICO score can unlock access to premium cards with rewards programs and lower interest rates, while a lower score may limit options to secured cards or those with higher fees. Similarly, when applying for a personal loan, a strong FICO score can result in favorable terms, such as lower APRs and longer repayment periods, making it a crucial factor in financial planning.

However, reliance on FICO scores is not without challenges. Critics argue that these scores may not fully capture an individual's financial situation, particularly for those with limited credit histories or unconventional income sources. Banks must balance the efficiency of using FICO scores with the need for a more holistic assessment, especially in cases where alternative data, such as rental payments or utility bills, could provide additional insights. Despite these limitations, FICO scores remain a cornerstone of risk management in banking, offering a reliable, data-driven approach to credit evaluation.

In practical terms, understanding and improving one’s FICO score can significantly enhance financial opportunities. Key strategies include paying bills on time, reducing credit card balances, and avoiding frequent credit inquiries. For young adults or those rebuilding credit, secured credit cards or becoming an authorized user on a family member’s account can help establish a positive credit history. Regularly monitoring credit reports for inaccuracies and disputing them promptly is also essential, as errors can unfairly lower a FICO score. By taking proactive steps, individuals can position themselves for better loan terms and financial flexibility.

How Banks Generate Profits: Key Strategies and Revenue Streams Explained

You may want to see also

Explore related products

![]()

Improving FICO Scores: Pay bills on time, reduce debt, and monitor credit to boost scores

FICO, an acronym for Fair Isaac Corporation, is a critical metric in the banking and financial sectors, representing a credit score that lenders use to assess an individual’s creditworthiness. Ranging from 300 to 850, a higher FICO score signifies lower credit risk, unlocking access to better loan terms, lower interest rates, and increased financial opportunities. For those looking to enhance their financial standing, improving this score is a tangible goal with clear, actionable steps.

Step 1: Pay Bills on Time

Late payments are a red flag to creditors, signaling financial instability. Payment history accounts for 35% of your FICO score, making it the single most influential factor. To ensure timely payments, set up automatic transfers for recurring bills, such as credit cards, loans, and utilities. For variable expenses, mark due dates on a calendar or use reminders on your phone. If you’ve missed payments in the past, focus on consistency moving forward—time heals this blemish, but only if you avoid repeating the mistake.

Step 2: Reduce Debt Strategically

High debt levels, particularly on credit cards, can drag down your score. Aim to keep your credit utilization ratio—the percentage of available credit you’re using—below 30%. For example, if you have a $10,000 credit limit, keep balances under $3,000. Prioritize paying off high-interest debt first, but also make small payments on other accounts to keep them active and demonstrate responsible management. Avoid closing old accounts, as this reduces your overall credit limit and can increase your utilization ratio.

Step 3: Monitor Credit Reports Vigilantly

Errors on credit reports are more common than you might think, and they can unfairly lower your score. Obtain free annual credit reports from the three major bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com. Review them for inaccuracies, such as incorrect account balances, unauthorized inquiries, or accounts that aren’t yours. Dispute errors directly with the bureau and the reporting creditor. Additionally, consider using credit monitoring services that alert you to significant changes, helping you catch potential fraud early.

Cautions and Considerations

While these steps are effective, they require patience. Improving a FICO score isn’t an overnight process—it can take 6 to 12 months of consistent effort to see meaningful results. Avoid quick-fix schemes, such as paying for credit repair services that promise instant improvements, as these are often scams. Similarly, resist the temptation to open new credit accounts solely to increase your available credit, as this can temporarily lower your score due to hard inquiries and reduced average account age.

Improving your FICO score is a deliberate, disciplined process that hinges on timely payments, strategic debt reduction, and vigilant credit monitoring. By adopting these habits, you not only boost your score but also cultivate financial health that extends beyond creditworthiness. Start today—your future self will thank you for the opportunities a strong FICO score unlocks.

A Beginner's Guide to Purchasing Digital Gold Through Your Bank

You may want to see also

Frequently asked questions

FICO stands for Fair Isaac Corporation, the company that developed the FICO credit scoring model widely used in banking and lending.

A FICO score is used by banks and lenders to assess a borrower's creditworthiness, helping them determine the risk of extending credit or loans.

A FICO score is calculated based on factors such as payment history, credit utilization, length of credit history, types of credit, and new credit inquiries.

FICO scores typically range from 300 to 850, with higher scores indicating lower credit risk and better borrowing terms for individuals.

FICO scores are crucial in banking as they help lenders make informed decisions about loan approvals, interest rates, and credit limits, ensuring responsible lending practices.