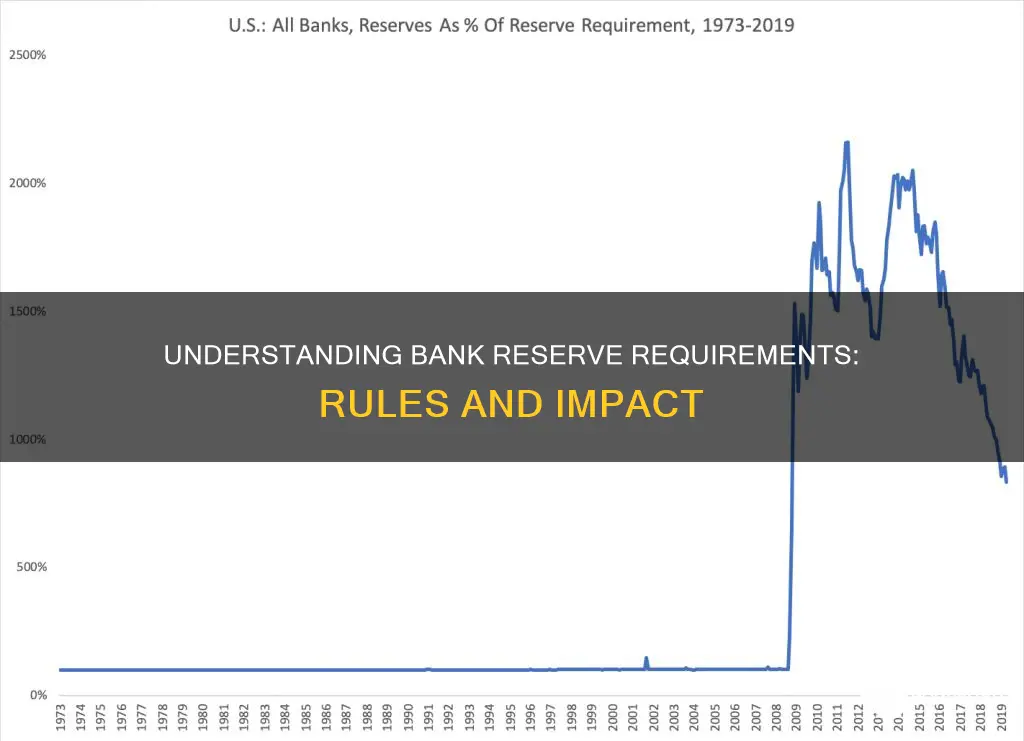

Reserve requirements are the amount of funds that a bank holds in reserve to ensure it can meet liabilities in the event of sudden withdrawals. They are set by a country's central bank, which determines the minimum amount of liquid assets that a commercial bank must hold. The reserve requirement is a tool used by central banks to control the money supply in the economy and influence interest rates. For example, if the Federal Reserve lowers the reserve requirement, banks will have more money to lend, which will lower interest rates. As of March 26, 2020, the Federal Reserve has reduced the reserve requirement ratio to zero percent for all depository institutions in response to the COVID-19 pandemic.

| Characteristics | Values |

|---|---|

| Definition | The amount of funds that a bank holds in reserve to ensure that it is able to meet liabilities in case of sudden withdrawals. |

| Purpose | To increase or decrease the money supply in the economy and influence interest rates. |

| Set By | The Federal Reserve's Board of Governors. |

| Current Ratio | Zero percent across all deposit tiers since March 26, 2020, in response to the COVID-19 pandemic. |

| Previous Ratios | Varied across different types of banks and deposits. For example, the reserve requirement for certain foreign borrowings was raised from 10% to 20% in 1971. |

| Exemptions | Some countries, like Canada, the UK, Australia, New Zealand, and Sweden, do not have reserve requirements and instead adhere to capital requirements. |

| Impact of Changes | Increasing the reserve requirement reduces the amount available for lending, leading to higher interest rates. Decreasing it has the opposite effect. |

| Considerations | Abrupt changes can cause liquidity problems for banks with low excess reserves, so they are generally avoided. |

Explore related products

![Bank deposits and legal reserve requirements; a study of the legal reserve requirements of the Federal Reserve System in the light of the composition and behavior of deposits in member [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

What You'll Learn

![]()

The reserve requirement is a tool to control liquidity

The reserve requirement is a tool used by central banks to control liquidity and increase or decrease the money supply in the economy. It is the amount of funds that a bank holds in reserve to meet liabilities in the event of sudden withdrawals. The reserve requirement is set by the central bank as a minimum amount, commonly referred to as the commercial bank's reserve, which is determined based on a specified proportion of the bank's deposit liabilities.

The reserve requirement is used to influence interest rates and control liquidity in the financial system. By reducing the reserve requirement, the central bank executes an expansionary monetary policy, increasing the money supply in the economy. Conversely, when the reserve requirement is raised, it leads to a contractionary monetary policy, reducing the money supply. The reserve requirement can impact interest rates, as banks loan funds to customers based on a fraction of their cash on hand.

The reserve requirement is not a static figure and can be adjusted by the central bank to meet economic needs. For example, in response to the COVID-19 pandemic, the Federal Reserve in the United States reduced the reserve requirement ratio to zero across all deposit tiers to jump-start the economy by allowing banks to lend more to individuals and businesses. This reduction in the reserve requirement increased liquidity in the financial system.

While the reserve requirement is a tool to control liquidity, it is not the only mechanism used by central banks. Other tools, such as interest rates on excess reserves and quantitative easing, also play a role in managing liquidity and achieving monetary policy goals. The use of these tools depends on various factors, including the demand for bank reserves, deposit composition, and yield curve considerations.

The Fed's Role: Bank Examinations and Their Importance

You may want to see also

Explore related products

$15.75

![]()

Reserve ratios are used to influence money supply

Reserve ratios are a tool used by central banks to influence the money supply in an economy. The reserve ratio, also known as the cash reserve ratio, is the minimum amount of funds a bank must hold in liquid assets to meet liabilities in the event of sudden withdrawals. This amount is set by the central bank and is determined by applying the reserve requirement ratios to an institution's reservable liabilities.

By increasing the reserve requirement, the central bank can limit the amount of lending by banks, thereby reducing the money supply in the economy. This is known as a contractionary monetary policy. Conversely, by reducing the reserve requirement, the central bank can increase the amount of lending by banks, leading to an expansionary monetary policy. For example, during the COVID-19 pandemic, the Federal Reserve reduced the reserve requirement ratio to zero to allow banks to use additional liquidity to lend to individuals and businesses, thereby stimulating the economy.

The reserve requirement is an important tool for central banks to control liquidity in the financial system. However, changes to the reserve requirement can have short-term disruptive effects on financial markets, so monetary authorities carefully consider such changes. In some countries, such as the United States, there are currently zero reserve requirements.

The interest rate paid on excess reserves, which are reserves above the minimum requirement, can also influence the money supply. For example, upon the introduction of quantitative easing and interest on excess reserves in 2009, banks were compensated for holding all their reserves, and the concept of excess reserves became less relevant.

The City Bank Logo: What Font Is It?

You may want to see also

Explore related products

$33.53 $42.99

![]()

Banks borrow to meet reserve requirements

Banks are required to hold a certain amount of cash in their vaults or at the closest Federal Reserve bank, in line with deposits made by their customers. This is known as the reserve requirement. The reserve requirement is determined by applying the reserve requirement ratios specified in the Board's Regulation D (Reserve Requirements of Depository Institutions, 12 CFR Part 204) to an institution's reservable liabilities.

The reserve requirement is a tool used by the central bank to increase or decrease the money supply in the economy and influence interest rates. By reducing the reserve requirement, the central bank is executing an expansionary monetary policy, and when it raises the requirement, it is exercising a contractionary monetary policy. The reserve requirement is set by the Federal Reserve Board of Governors, which also sets the interest rate banks get paid on excess reserves.

If a bank does not have enough cash to meet the reserve requirement, it can borrow from other banks or from the Fed's discount window. This is known as the federal funds rate, which serves as a basis for many other interest rates in the economy. Banks may also borrow short-term funds in the interbank lending market from banks with a surplus. In exceptional situations, the central bank may provide funds to cover the short-term shortfall as a lender of last resort.

Historically, central banks have occasionally changed reserve requirements to influence the money supply directly and, in turn, influence interest rate levels. However, this implementation policy is rarely used today. In the US, the Federal Reserve eliminated reserve requirements entirely in 2020, instead opting to use changes in the interest rate paid on reserves held by commercial banks as its primary monetary policy instrument.

Western Alliance Bank: Mobile App Availability

You may want to see also

Explore related products

![]()

History of reserve requirements

The practice of holding reserves in banks started during the early 19th century with the first commercial banks. The National Bank Act of 1863 imposed a 25% reserve requirement on banks under its charge. In 1865, a tax on state banknotes ensured that national bank notes replaced other currencies as a medium of exchange.

The creation of the Federal Reserve and its constituent banks in 1913 acted as a lender of last resort, further eliminating the risks and costs required in maintaining reserves. This also pared down reserve requirements from their earlier high levels. For example, reserve requirements for three types of banks under the Federal Reserve were set at 13%, 10%, and 7% in 1917.

In the years following, the reserve requirement was adjusted several times. Effective October 20, 1983, required reserves were reduced by an estimated $100 million due to the elimination of reserve requirements on non-personal time deposits with maturities of 1-1/2 years to 2-1/2 years. On January 12, 1984, the low reserve tranche for transaction accounts at depository institutions was raised from $26.3 million to $28.9 million. In 1985, the low reserve tranche for transaction accounts was raised again, this time from $28.9 million to $29.8 million.

In response to the COVID-19 pandemic, the Federal Reserve reduced the reserve requirement ratio to zero across all deposit tiers, effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.

OnlyFans Payouts: Which Banks Are Compatible?

You may want to see also

Explore related products

$35.49 $37.99

![]()

The Federal Reserve's role in setting requirements

The Federal Reserve, the central bank of the United States, is responsible for providing the country with a safe, flexible, and stable monetary and financial system. The Federal Reserve Act authorises the Board of Governors to establish reserve requirements within specified ranges for certain types of deposits and other liabilities of depository institutions. The Board of Governors sets the reserve requirement, which is the minimum amount of cash that financial institutions must hold in their vaults or at the closest Federal Reserve bank. This is based on customer deposits and is one of the three main tools of monetary policy.

The reserve requirement is a critical tool that the Federal Reserve uses to control liquidity in the financial system and influence interest rates. By reducing the reserve requirement, the Federal Reserve increases the money supply in the economy, executes an expansionary monetary policy, and lowers interest rates. Conversely, when the Federal Reserve raises the reserve requirement, it reduces the money supply, exercises a contractionary monetary policy, and increases interest rates.

The Federal Reserve adjusts the reserve requirement to achieve specific economic outcomes. For example, in response to the COVID-19 pandemic, the Federal Reserve reduced the reserve requirement ratio to zero across all deposit tiers, effective March 26, 2020. This reduction aimed to jump-start the economy by allowing banks to use additional liquidity to lend to individuals and businesses.

The Federal Reserve has historically modified the reserve requirement to address various economic situations. For instance, in 1980, the marginal reserve requirement was reduced from 10% to 5%, resulting in a decrease in required reserves. In contrast, in 1978, a supplementary reserve requirement of 2% was imposed on time deposits over $100,000, leading to an increase in required reserves. These adjustments demonstrate the Federal Reserve's role in managing the economy through the manipulation of reserve requirements.

DFAS: When Do Banks Receive Payments?

You may want to see also

Frequently asked questions

Reserve requirements are the amount of funds that a bank holds in reserve to ensure that it is able to meet liabilities in case of sudden withdrawals.

Reserve requirements are a tool used by the central bank to increase or decrease the money supply in the economy and influence interest rates.

When the central bank raises reserve requirements, banks have less to lend out to consumers and businesses, which raises interest rates. Conversely, when the central bank lowers reserve requirements, interest rates tend to fall.

The reserve requirement ratio was reduced to 0% across all deposit tiers in the United States in March 2020 in response to the COVID-19 pandemic. This means that there are currently no reserve requirements for banks in the US.

No, some countries such as Canada, the United Kingdom, New Zealand, Australia, and Sweden do not have reserve requirements. Instead, they may adhere to capital requirements, which refer to the amount of equity a bank must hold.