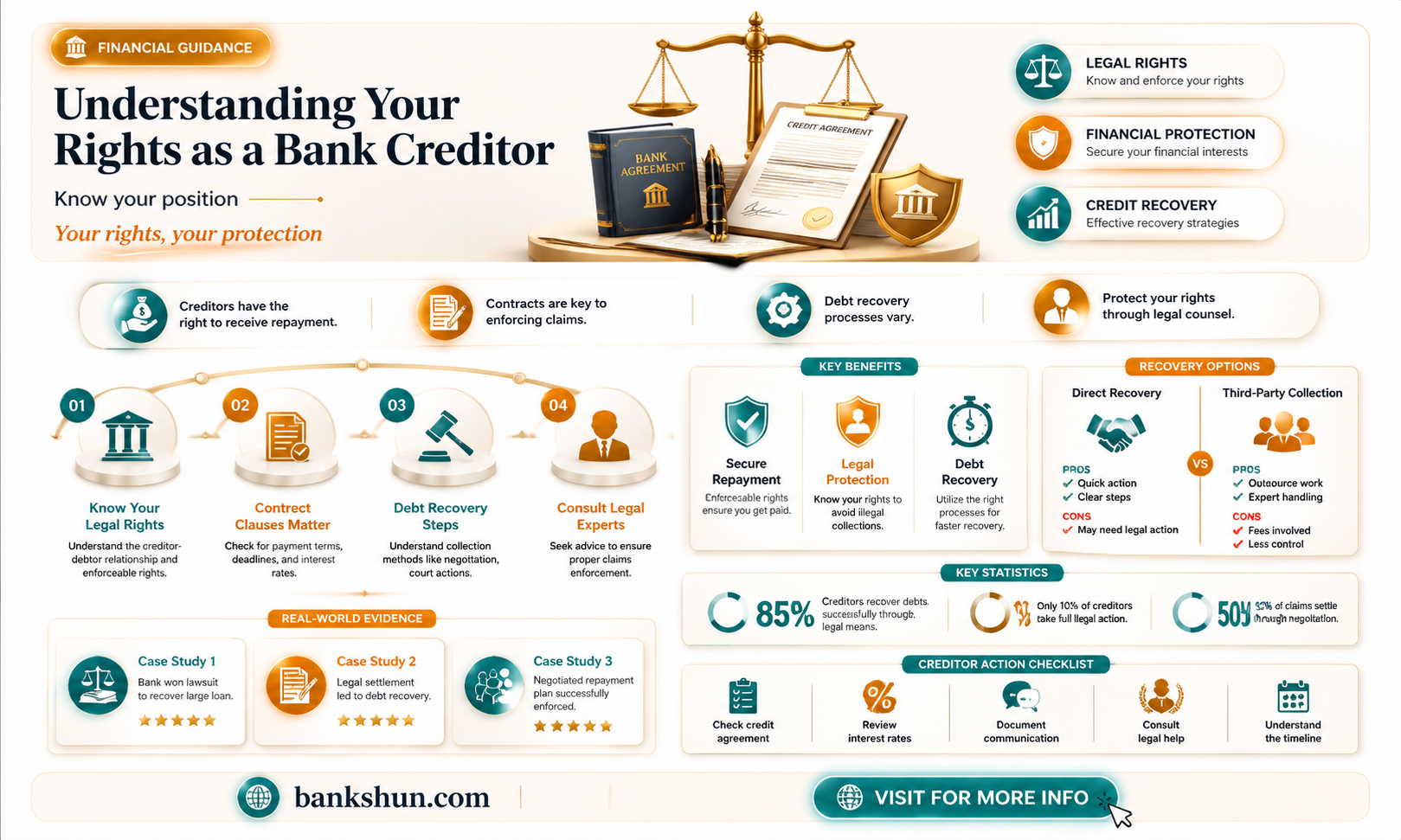

A creditor is a person or entity that lends money to another party through an agreement or contract. The term 'creditor' typically refers to a financial institution, such as a bank, that lends money and is owed that money. However, a creditor can also be an individual who lends money to friends or family, or a business that provides supplies or services to a company or individual but allows for a delay in payment. Creditors can be classified as personal, real, secured, or unsecured. Personal creditors are individuals who lend money, while real creditors are financial institutions with legally binding contracts that allow them to seize the borrower's assets if they default on the loan. Secured creditors have a legal right to reclaim property used as collateral for a loan, while unsecured creditors do not have this right and may be at higher risk of losing their money.

| Characteristics | Values |

|---|---|

| Definition | A creditor is a person or entity that loans another party money through an agreement or contract. |

| Types | Personal, real, secured, and unsecured. |

| Personal creditor | Friends or family who lend money. |

| Real creditor | Financial institutions, such as banks or credit card issuers, that have a right to be repaid. |

| Secured creditor | Lenders with a legal or contractual right to assets put up as collateral to secure a loan. |

| Unsecured creditor | Lenders who have loaned money but did not secure assets to safeguard themselves against unpaid debt. |

Explore related products

What You'll Learn

![]()

Who is a creditor?

A creditor is an individual or institution that extends credit to another party to borrow money, usually by a loan agreement or contract. In other words, a creditor is a person or entity that loans money to another party through an agreement or contract.

Creditors are commonly classified as personal or real. Personal creditors are those who loan money to friends or family, or a business that provides immediate supplies or services to a company or individual but allows for a delay in payment. Real creditors, on the other hand, are banks or finance companies that have legal contracts and loan agreements with the borrower that grant the lender the right to claim any of the debtor's real assets or collateral if the loan is unpaid. Real creditors are financial institutions, such as banks or credit card issuers, that have a right to be repaid.

The term creditor can also be used to refer to secured and unsecured creditors. Secured creditors are lenders with a legal or contractual right to assets put up as collateral to secure a loan. Unsecured creditors, such as credit card companies, are lenders who have loaned money but did not secure assets to safeguard themselves against unpaid debt.

Creditors often charge interest on the loans they offer their clients, such as a 5% interest rate on a $5,000 loan. The interest represents the borrower's cost of the loan and the creditor's degree of risk that the borrower may not repay the loan. To mitigate risk, most creditors tie interest rates or fees to the borrower's creditworthiness and past credit history. Borrowers with good credit scores are considered low-risk to creditors and are often given low-interest rates, while borrowers with low credit scores are considered high-risk and are often charged higher interest rates.

In the context of a bank, a creditor is typically a financial institution or person who is owed money by the bank. This could include depositors who have placed money in the bank, as well as other financial institutions that have provided loans or credit to the bank. In the event of a bankruptcy, the creditors of a bank would be those individuals or entities that are owed money by the bank and would have a claim on the bank's assets.

The West Bank: Palestine's Territory?

You may want to see also

Explore related products

![]()

Types of creditors

Creditors can be individuals, businesses, or institutions that extend credit to another party. They can be classified as personal or real creditors. Personal creditors are individuals who loan money to friends or family, while real creditors are financial institutions such as banks or credit card companies that have legal contracts and loan agreements with the borrower.

There are several types of creditors:

- Secured creditors: These are often banks or mortgage companies that have a legal right to reclaim property, such as a car or home, used as collateral for a loan through repossession.

- Unsecured creditors: Credit card companies are a common example of unsecured creditors. Unsecured debt does not have collateral, such as a car or home, tied to it. If the debtor cannot repay the debt, the creditor may sue to garnish wages or take other actions.

- Loan creditors: These include banks and financial institutions that lend money, often with interest, to individuals or businesses.

- Trade creditors: These are entities that supply goods or services to a company or individual and allow for delayed payment. They extend credit to customers buying goods or services.

It is important to distinguish between creditors and debt collectors. Creditors are the original lenders that offer loans, while debt collectors purchase delinquent loans from creditors at a discount and focus on collecting that loan.

Reconciling Bank Statements: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Creditors and contracts

A creditor is an individual or institution that extends credit to another party to borrow money, usually by a loan agreement or contract. Creditors are commonly classified as personal or real. Personal creditors include friends or family that you borrow money from and have to pay back. Real creditors are banks or finance companies that have legal contracts and loan agreements with the borrower. They grant the lender the right to claim any of the debtor's real assets or collateral if the loan is unpaid.

Loan creditors include banks and financial institutions that lend money to businesses. When a company borrows funds for expansion or operations, the lender becomes a creditor until the loan is repaid. Trade creditors are suppliers or vendors who provide goods or services on credit. For example, a construction company may receive materials from a brick supplier without upfront payment, making the brick supplier a trade creditor.

Creditors can be unsecured or secured. Unsecured creditors lend money without any collateral. Secured creditors lend money with collateral, so if the debtor defaults on their loan, the creditor may repossess the asset pledged as collateral. Secured creditors, such as banks, can repossess collateral like homes and cars on secured loans, and take debtors to court over unsecured debts.

Creditors' rights are the procedural provisions designed to protect the ability of creditors to collect the money that they are owed. These provisions vary from one jurisdiction to another. Creditors' rights deal with the rights of creditors against the debtor and against one another. Attorneys who practice in the area of creditor's rights may file lawsuits and use other legal collection techniques to collect consumer and commercial debts. They may also represent the creditor's interests in a bankruptcy proceeding.

What ACH Stands for in Banking and Why It Matters

You may want to see also

Explore related products

![]()

Creditors and collateral

A creditor is an individual or institution that extends credit to another party to borrow money, usually by a loan agreement or contract. In simple terms, a creditor lends money and is owed that money.

Creditors can be classified as personal or real. Personal creditors are those who loan money to friends or family or a business that provides immediate supplies or services to a company or individual but allows for a delay in payment. Real creditors are banks or finance companies that have legal contracts and loan agreements with the borrower that grant the lender the right to claim any of the debtor's real assets or collateral if the loan is unpaid.

The term creditor can mean different things depending on the situation, but it typically means a financial institution or person who is owed money. If you’re the person who owes the money to a creditor, you may be referred to as a debtor or borrower.

There are four basic types of creditors: personal, real, secured, and unsecured.

Secured creditors have a legal right to reclaim the property, such as a car or home, used as collateral for a loan, often through a lien or repossession. Unsecured creditors, such as credit card companies, are creditors where the borrower has not agreed to give the creditor any property as collateral to secure a debt. These creditors may sue debtors over unpaid debts and courts may order the debtor to pay, garnish wages, issue a bank levy, or take other actions.

Collateral in the financial world is a valuable asset that a borrower offers to a lender as security for a loan. Collateral is a guarantee for the lender. For example, when a homebuyer gets a mortgage, the home serves as the collateral for the loan. For a car loan, the vehicle is the collateral. A business that obtains financing from a bank may pledge valuable equipment or real estate owned by the business as collateral for the loan. In the event of a default, the lender can seize the collateral and sell it to recoup the loss.

Disconnecting Your Bank from Plaid: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Creditors and interest rates

A creditor is an individual or institution that extends credit to another party, allowing them to borrow money through a loan agreement or contract. Creditors are typically financial institutions or persons who are owed money, and they can be classified as personal or real. Personal creditors include friends or family, while real creditors are banks or financial institutions with legally binding contracts that allow them to seize the borrower's assets if they default on their loans.

When a person borrows money from a bank, they enter into a creditor-debtor relationship. The creditor (the bank) lends money to the debtor (the borrower) with the expectation of repayment, often with interest. Interest rates are applied to the principal amount of the loan, and they represent the cost of debt for the borrower and the rate of return for the creditor.

Interest rates are influenced by various factors, including the borrower's credit score, loan type, and overall economic conditions. Borrowers with good credit scores are considered low-risk by creditors and are usually offered lower interest rates. Conversely, borrowers with low credit scores are perceived as riskier, leading to higher interest rates to mitigate the creditor's potential losses.

The interest rate also depends on the creditor's assessment of the loan's risk. A loan considered low-risk by the creditor will generally have a lower interest rate, while a high-risk loan will attract a higher interest rate. This risk assessment is tied to the borrower's creditworthiness and credit history.

In addition to interest rates, creditors may also charge fees associated with the loan. These fees can vary depending on the creditor and the specific terms of the loan agreement. It is important for borrowers to carefully review the loan agreement to understand all the associated costs, including interest rates and any applicable fees.

Understanding the relationship between creditors and interest rates is crucial for both borrowers and lenders. Borrowers should aim to maintain good credit scores to access more favourable loan terms, while creditors use interest rates as a tool to manage risk and generate returns on their lending activities.

Banking Experts: Who to See and When

You may want to see also

Frequently asked questions

A creditor is a person or financial institution that lends money to another party.

A real creditor is a financial institution, such as a bank or credit card company, that has a right to be repaid. Personal creditors are individuals who lend money to friends or family.

Secured creditors have a legal right to reclaim the property, such as a car or home, used as collateral for a loan. Unsecured creditors, such as credit card companies, do not have this right, and the borrower has not agreed to give any property as collateral.

A creditor lends money and is owed money, while a debtor borrows money and owes the debt.