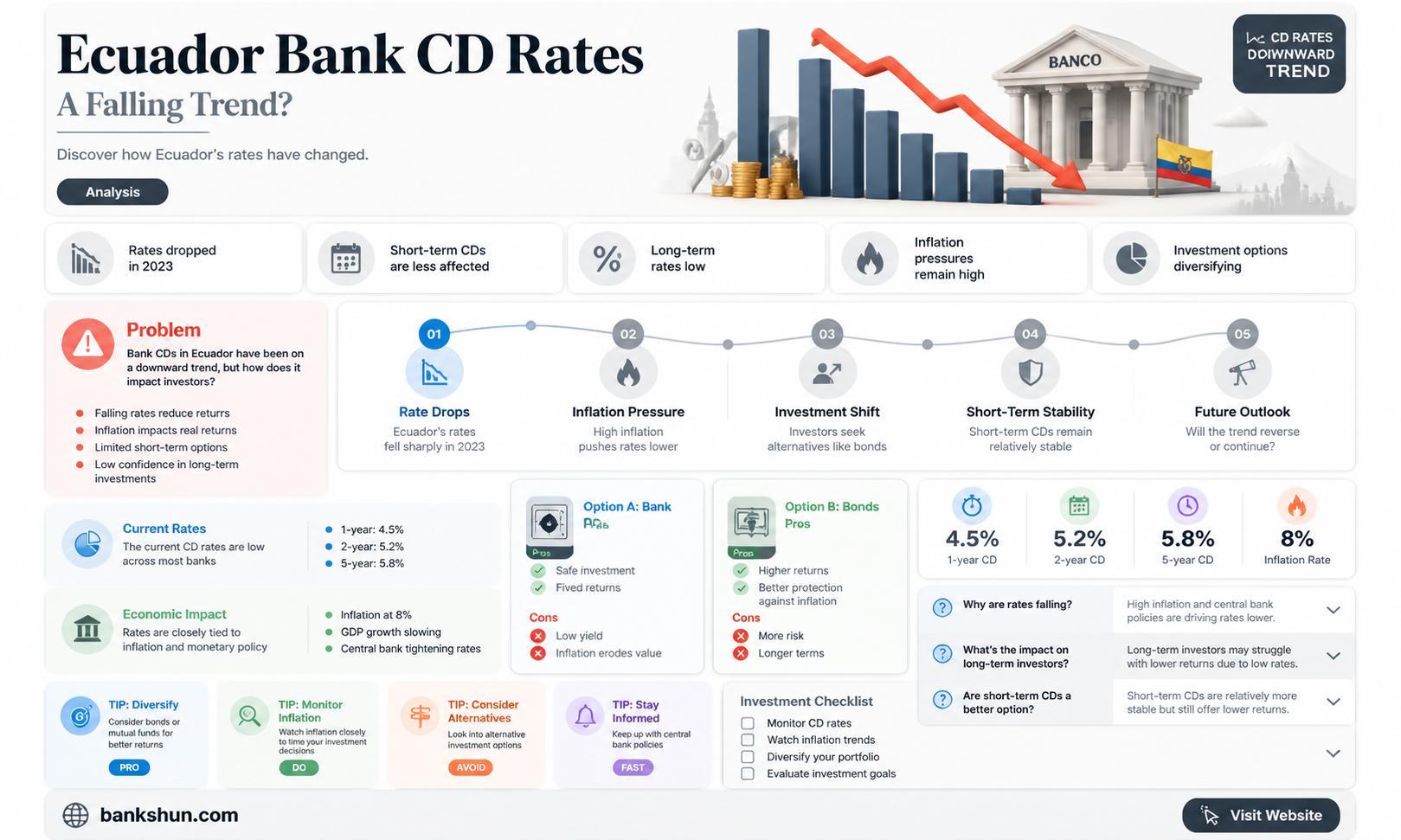

Ecuador's interest rates on Certificates of Deposit (CDs) are higher than those in the United States. Since 2010, there has been a 3-5% spread between CD rates in the US and Ecuador. For instance, if a CD in the US pays 5% interest, the same CD in Ecuador will generally pay 8-9%. Banks in Ecuador currently pay between 5% and 7% interest on one-year CDs, while cooperativas pay between 7% and 10% interest. However, it is important to note that early liquidation of CDs in Ecuador can be difficult and costly, and that Ecuadorian tax laws change frequently.

| Characteristics | Values |

|---|---|

| Interest rates on CDs | 5% to 10% |

| Interest rates compared to the US | 3-5% higher |

| Interest payment frequency | Monthly |

| CD term | 1 year or more |

| CD providers | Banks and Cooperativas de Ahorro Y Crédito |

| CD interest rates compared between providers | Cooperativas offer higher rates than banks |

| Minimum investment amounts, rates, terms, and early withdrawal policies | Set by each institution, subject to Ecuadorian law |

| Investor visa eligibility | Yes, with specific requirements |

| Physical presence required to open an account | Yes |

Explore related products

What You'll Learn

![]()

Ecuador CD rates are higher than in the US

Ecuador's interest rates on Certificates of Deposit (CDs) are notably higher than those in the United States. Since 2010, there has been a 3-5% spread between CD rates in the two countries. For example, if a CD in the U.S. pays an interest rate of 5%, the same CD in Ecuador will generally pay an interest rate of 8-9%. This boost in interest income, combined with Ecuador's much lower cost of living, can significantly enhance an individual's quality of life, especially for those retired on a fixed income.

Ecuadorian financial institutions can offer higher interest rates than their U.S. counterparts because they, in turn, receive much higher interest rates for the money they lend out, which can be as high as 16%. Additionally, the larger economy and banking sectors in Ecuador are quite different from those in North America, with the government and people utilising significantly less debt. Ecuador's government and personal debt are relatively low. The poverty rate has decreased from 35% a decade ago to 21% currently, and the national debt is approximately 40% of its gross domestic product (GDP).

When investing in CDs in Ecuador, it is essential to shop around and ask banks at what dollar amounts the rates change. For instance, a CD with a deposit ranging from $10,000 to $30,000 may receive a certain interest rate, but that rate may increase by 0.3% if the deposited amount exceeds $30,000. It is also important to consider the length of the CD. As of 2024, CDs in Ecuador lasting more than six months are exempt from income tax, and the best rates are typically offered for CDs with durations of more than one year. However, early liquidation of CDs in Ecuador can be challenging, and it is generally difficult to retrieve the money before maturity unless there are exceptional circumstances.

While investing in Ecuadorian CDs can provide higher interest rates, it is important to be aware of the risks and restrictions. Deposit insurance from COSEDE, the Ecuadorian government's Deposit Insurance arm, protects a depositor's funds up to a certain limit, typically $32,000 per institution. However, there may be concerns about the reliability of the insurance guarantee in the event of a major issue, as Ecuador cannot simply print more USD to cover any potential shortfalls. Therefore, it is advisable to diversify investments and not put all funds into Ecuadorian CDs alone.

ACH Banking: How Does It Work?

You may want to see also

Explore related products

![]()

Banks vs. Cooperativas de Ahorro Y Crédito

Banks and Cooperativas de Ahorro y Crédito (similar to credit unions) offer different interest rates in Ecuador. Banks typically offer lower CD interest rates, ranging from 5% to 7% for one-year CDs, because they are perceived as more secure. On the other hand, Cooperativas de Ahorro y Crédito offer higher interest rates, ranging from 7% to 10% for one-year CDs, as they are perceived as less secure.

The interest rates offered by banks in Ecuador can vary depending on the amount deposited and the length of the CD. For example, a CD with $10,000 to $30,000 at one bank may offer a certain rate, but that rate may increase by 0.3% if you deposit more than $30,000. Additionally, CDs lasting more than six months are typically exempt from Ecuadorian income tax, and the best rates are usually offered for CDs lasting more than one year. It is important to note that early withdrawal from CDs in Ecuador can be difficult and may require legal assistance.

Cooperativas de Ahorro y Crédito have a strong social presence and are governed by principles and values. They offer the same services as banks, such as savings accounts, loans, and payment services, but their objectives differ. The financial system in Ecuador includes both public and private institutions, as well as processes of popular and solidarity economy, which creates a clear differentiation.

When deciding between banks and Cooperativas de Ahorro y Crédito in Ecuador, it is important to consider the interest rates, the length of the CD, and the early withdrawal policies. Additionally, understanding the regulatory environment and the social impact of these institutions can also be important factors in making an informed decision.

The Bank Job: Fact or Fiction?

You may want to see also

Explore related products

![]()

Requirements for an investor visa

Ecuador's Investor Visa, or 'Inversionista', is a residence permit that offers a cost-effective pathway for foreign nationals to gain permanent residency and citizenship. The visa has one of the world's lowest minimum investment requirements, with a threshold of $46,000 to $47,500. This can be invested in a variety of asset classes, including real estate, company shares, or a Certificate of Deposit (CD) with a recognised Ecuadorian financial institution.

The Investor Visa provides applicants with a three-year path to permanent residency and a four-year route to citizenship. To qualify, applicants must spend at least 180 to 185 days a year in Ecuador during the years preceding their application. After two years of continuous residency, an applicant is eligible for permanent residency. To qualify for citizenship after four years, an applicant must demonstrate mastery of the Spanish language and Ecuadorian civics.

The CD option for the Investor Visa must be for a minimum of two years, with monthly interest payments. The interest rates on CDs in Ecuador are significantly higher than in the US, ranging from 5% to 10%. However, liquidating a CD before maturity can be challenging and may require legal assistance.

It is important to note that each document submitted as part of the visa application must be dated within six months prior to submission to ensure their validity. Additionally, the application form must be in Spanish.

Russia's SWIFT Sanctions: Which Banks Are Affected?

You may want to see also

Explore related products

![]()

Tax implications for Americans

Ecuador's interest rates on Certificates of Deposit (CDs) are higher than those in the United States. For example, a CD in the U.S. that pays 5% interest would generally pay 8-9% in Ecuador. This boost in interest income, combined with Ecuador's lower cost of living, can significantly improve an individual's quality of life, especially if they are retired and living on a fixed income.

As an American, it is important to note that you will need to pay taxes on CD interest every year that it is earned, even before the CD matures and you can access the money. The IRS considers CD interest as ordinary income, just like money earned from employment, and it is taxed at the same rate. This means that you will need to pay taxes on CD interest at your regular income tax rate, which can range from 10% to 37% for federal taxes, plus any applicable state taxes.

If you earn $10 or more in interest during the year, your bank will send you Form 1099-INT, which shows your taxable interest income. Even if you do not receive this form, you are still required to report any interest earnings of $10 or more on your federal income tax return. It is important to note that you must give the payer of interest income your correct taxpayer identification number to avoid penalties and backup withholding.

There are ways to minimize or eliminate taxes on CD interest. One way is to hold CDs in retirement accounts such as IRAs, HSAs, or 529 plans. With a Roth IRA CD, the interest is tax-free if you hold the IRA for 5 years and are 59.5 years old or older. Another option is to open a short-term CD, which allows you to defer taxes from one year to the next. Additionally, early withdrawal penalties can be deducted from your taxes, potentially reducing what you owe.

It is important to consult with a tax professional to understand the specific tax implications for your situation and to stay up-to-date with changing tax laws.

The Future of Truist Bank: Will It Survive?

You may want to see also

Explore related products

![]()

Early liquidation

The difficulty of early liquidation also depends on the type of CD. For CDs associated with an Inversionista Visa, liquidating before maturity is particularly challenging. On the other hand, non-visa CDs may offer slightly more flexibility, but even then, early liquidation is generally not advisable due to the associated costs and complexities.

It is important to carefully consider the terms and conditions of the CD before investing, as early liquidation can result in significant financial losses. Additionally, it is worth noting that Ecuadorian banks generally do not have a mechanism for withdrawing money early, unlike some other countries that may allow cancellation with a penalty.

Overall, while early liquidation of bank CDs in Ecuador is technically possible in specific circumstances, it is a complex and costly process that should be approached with caution. Investors should be prepared for the possibility of losing a significant portion of their interest earnings and should carefully evaluate their options before initiating early liquidation.

DDA: What It Means and Its Importance in Banking

You may want to see also

Frequently asked questions

The bank CD rates in Ecuador are higher than in the United States. Banks in Ecuador currently pay between 5% and 7% interest on one-year CDs, while cooperativas pay between 7% and 10% interest on those one-year CDs.

It is unclear whether bank CD rates are falling in Ecuador. While the deposit interest rate reached an all-time high of 4.865% pa in 2008, it decreased to 3.496% pa in 2017, the lowest rate recorded since 2008.

Since 2010, there has been around a 3-5% spread between CD rates in the US and Ecuador. For example, if a CD in the US pays 5% interest, the same CD in Ecuador will generally pay 8-9% interest.