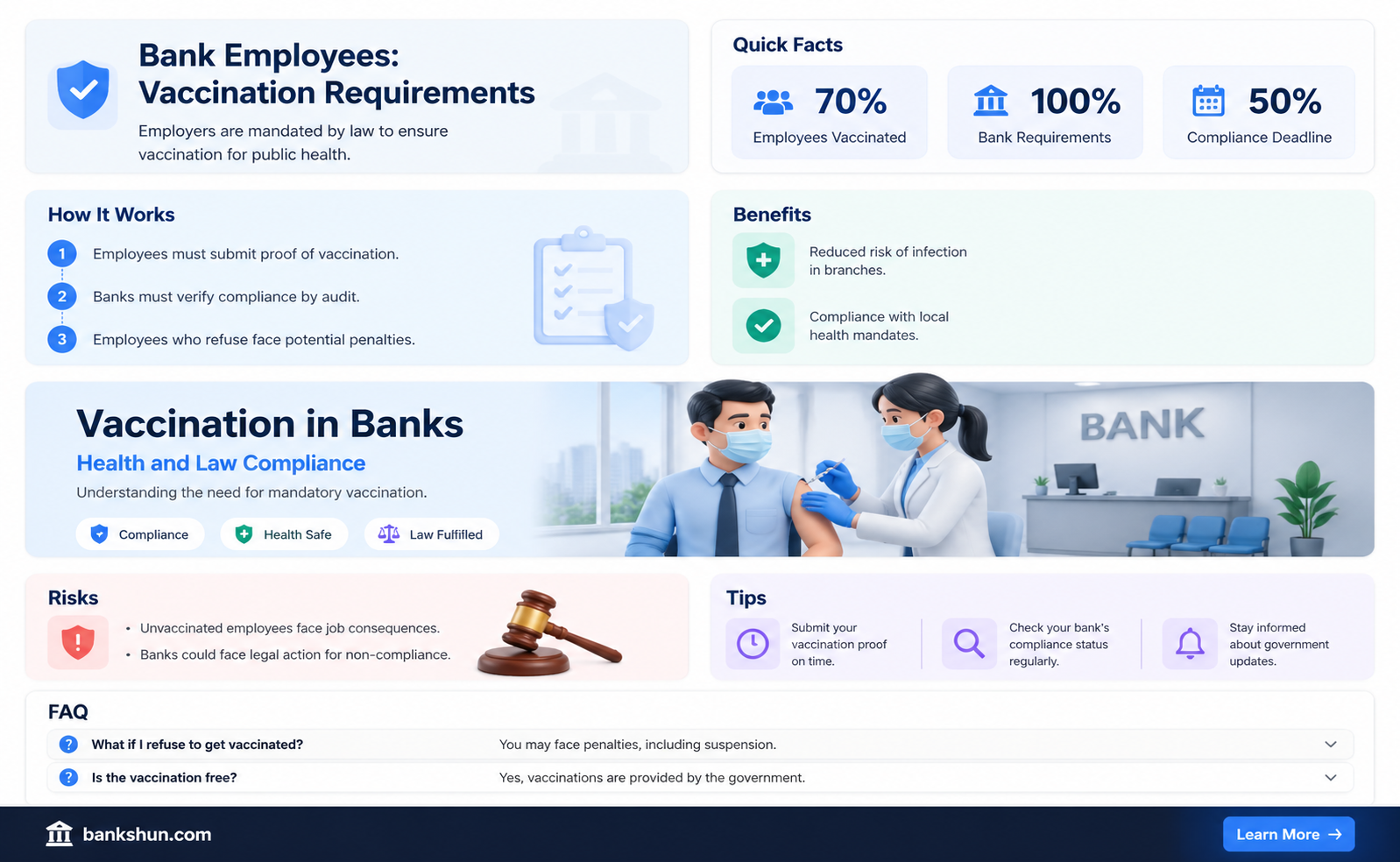

The COVID-19 pandemic has raised questions about whether bank employees are required to be vaccinated. While some banks, such as Morgan Stanley and Goldman Sachs, have mandated vaccines for their employees, others have taken a more relaxed approach, only encouraging vaccinations without making them compulsory. The decision to require vaccinations varies among banks and is influenced by factors such as local regulations, the prevalence of the virus, and the specific operations of the bank. Ultimately, the goal is to ensure a safe workplace for employees and customers while navigating the complex landscape of the pandemic.

| Characteristics | Values |

|---|---|

| Companies mandating vaccines for all employees | McDonald's, Ford, General Electric, Goldman Sachs |

| Companies mandating vaccines for some employees | Morgan Stanley, CVS, Goldman Sachs |

| Companies encouraging vaccination | JPMorgan Chase, Citi, Fifth Third |

| Companies offering incentives for vaccination | Fifth Third |

| Companies requiring vaccination status disclosure | Goldman Sachs, Morgan Stanley |

| Companies requiring vaccination for office entry | Morgan Stanley, Goldman Sachs |

| Companies requiring vaccination for business travel | Ford |

| CDC recommended vaccination phase for bank workers | Phase 1c |

Explore related products

What You'll Learn

- Morgan Stanley bars unvaccinated staff and clients from its New York offices

- Goldman Sachs requires vaccination for anyone entering its offices

- JPMorgan Chase encourages vaccination but enforces mask-wearing for all workers

- CDC recommends bank workers be in the third phase of vaccinations

- Banks offering incentives for employees to get vaccinated

![]()

Morgan Stanley bars unvaccinated staff and clients from its New York offices

The COVID-19 pandemic has forced companies to implement vaccine policies for their employees. In the United States, the CDC recommended that bank workers be included in the third phase of vaccinations. Following this, several banks have mandated that their employees be vaccinated.

One such bank is Morgan Stanley, which made headlines when it announced that it would bar unvaccinated staff and clients from entering its offices in New York City and Westchester. This decision was communicated to employees and clients through an internal memo, which stated that starting July 12, 2021, all individuals entering Morgan Stanley's New York City and Westchester offices would be required to be fully vaccinated against COVID-19.

The memo, signed by Chief Human Resources Officer Mandell Crawley, emphasized that employees who could not provide proof of full vaccination would lose building access. This move by Morgan Stanley followed similar announcements by other major banks, such as Goldman Sachs, which required its staff to inform the bank of their vaccination status, and General Electric, which mandated vaccines for its 56,000 U.S. workers.

Morgan Stanley's decision to bar unvaccinated individuals from its New York offices was part of its push to return to pre-pandemic working patterns. The bank's CEO, James Gorman, had previously expressed his expectation for employees at the New York branch to return to the office, stating that if one felt safe dining out in a restaurant in New York City, they could come into the office. Gorman's stance on remote work was echoed by other banking executives, such as David Solomon of Goldman Sachs and Jamie Dimon of JP Morgan, who viewed remote working as an "aberration" and a poor practice, respectively.

The implementation of vaccine mandates by companies like Morgan Stanley has sparked discussions about employee privacy and health concerns. While some view mandatory vaccinations as pushy or invasive, others argue that companies have a responsibility to ensure the health and safety of their workforce. Additionally, requiring vaccinations can help alleviate employee stress and tension in the office, especially in cities that were once epicenters of the pandemic, like New York.

The Federal Reserve: Government Entity or Independent Actor?

You may want to see also

Explore related products

![]()

Goldman Sachs requires vaccination for anyone entering its offices

As the delta variant continues to spread across communities in the US, companies and organisations are introducing stricter vaccine mandates for their employees. Goldman Sachs is one of the latest banks to require vaccinations for anyone entering its offices. The bank communicated this new policy to its employees via a memo, which stated that only vaccinated people can enter its buildings starting from September 7, 2021. This policy applies to everyone, including employees, clients, and visitors.

Goldman Sachs' decision to mandate vaccinations for anyone entering its offices is understandable and a reasonable response to the COVID-19 pandemic. By requiring vaccinations, the bank can help alleviate employees' concerns about returning to the office and reduce their stress. Additionally, having a large percentage of the office staff vaccinated can help prevent the spread of COVID-19 in the workplace and avoid potential legal liabilities in the event that an employee passes the virus to their co-workers.

Goldman Sachs' previous policy required its staff members to inform the bank of their vaccination status. The bank sent a memo to its employees in the United States, requesting them to report their vaccination status by a specified deadline. This allowed the bank to plan for a safer return to the office and abide by local public health measures. However, at that time, disclosing vaccination status was optional, and employees could choose to go maskless in the Manhattan office if they reported being inoculated.

Goldman Sachs' new policy requiring everyone entering its offices to be fully vaccinated is a response to the full approval of the Pfizer-BioNTech vaccine by the U.S. Food and Drug Administration. This approval has cleared the way for more corporations to mandate vaccinations for their employees. Employees who do not comply with the new policy will be expected to continue working from home.

Ecuador Bank CD Rates: A Falling Trend?

You may want to see also

Explore related products

![]()

JPMorgan Chase encourages vaccination but enforces mask-wearing for all workers

JPMorgan Chase & Co has not made vaccination mandatory for its employees, but it is strongly encouraging all its U.S. employees to get the Covid-19 vaccine. The bank has warned that the jab may eventually be made compulsory for workers. JPMorgan Chief Executive Jamie Dimon has been a strong advocate for the COVID-19 vaccines. In a memo, the bank said, "We strongly urge all of our employees to be vaccinated because we think it protects you, your friends and family, your fellow employees, and the community at large."

JPMorgan is now requiring all U.S. workers to log their vaccination status in a software portal. Employees who have been vaccinated do not need to wear masks, socially distance, or log their health status on a daily basis when they return to office life. Those who are unvaccinated need to wear masks and are encouraged to take weekly Covid tests. They must also continue to practice social distancing and complete daily health checks at all bank facilities.

The bank has said that it is looking into whether it can legally require staff to get the shots. JPMorgan has also stated that it strongly believes that the more people who are vaccinated, the safer they all are from the spread and impact of COVID-19. The bank's stance is in contrast to that of its smaller rival Morgan Stanley, which has announced that only vaccinated employees and clients could enter offices.

The issue of vaccination requirements for employees has been a topic of discussion for many companies. Some companies, like McDonald's, Ford, and Goldman Sachs, have mandated vaccines for all or some of their employees. The decision to require vaccinations may seem pushy and invasive of privacy, but companies have a responsibility to look out for the health and safety of their workers. A fully vaccinated workforce would reduce stress for employees and help avoid potential legal liabilities in the event an employee passes Covid-19 to their co-workers.

Linking Apple Pay: A Simple Guide to Bank Connections

You may want to see also

Explore related products

![]()

CDC recommends bank workers be in the third phase of vaccinations

The CDC has recommended that bank workers be included in Phase 1c of the COVID-19 vaccine rollout. This means that bank employees will be prioritised for vaccine doses alongside workers in sectors deemed essential but with a lower risk of exposure to COVID-19. This includes workers in transportation, food service, construction, IT, and telecommunications.

The American Bankers Association (ABA) has urged officials to allow for the vaccination of frontline essential workers in the banking sector as early as possible, citing their regular contact with the public. They believe that these workers face a high risk of infection and pose a great risk of spreading the virus if infected.

While the CDC's recommendation provides guidance, the decision on vaccine prioritisation is ultimately made by state public health authorities. Some states may choose to include bank employees in earlier phases of the vaccine rollout, depending on their individual criteria for determining essential workers.

Some banks have taken it upon themselves to mandate vaccines for their employees. Morgan Stanley, for example, requires its bankers, brokers, and traders to be vaccinated before returning to their New York City and Westchester County offices. Goldman Sachs has also required its staff to inform the bank of their vaccination status, though it does not require proof of vaccination. These decisions are made to ensure the health and safety of workers and to reduce the potential legal liabilities associated with COVID-19 infections in the workplace.

Understanding US Bank NSF Fee Amounts

You may want to see also

Explore related products

![]()

Banks offering incentives for employees to get vaccinated

While some banks have mandated COVID-19 vaccines for their employees, others have chosen to incentivize their workers to get vaccinated. Bank of America, for instance, is offering $200 awards to Merrill Lynch Wealth Management branch employees who return to the workplace and confirm they are fully vaccinated. To be eligible for the payment, employees must be in the office a minimum of eight times between early October and mid-November.

Morgan Stanley has also incentivized its bankers, brokers, and traders to get vaccinated by requiring unvaccinated workers to continue working remotely. Morgan Stanley CEO James Gorman bluntly stated, "If you can go into a city restaurant in New York, you can come into the office." He added that he would be "very disappointed" if workers had not "found their way into the office" by the Labor Day holiday on September 6.

Goldman Sachs, an arch-rival of Morgan Stanley, previously required its staff members to inform the bank of their vaccination status through its internal portal for employees. While employees need to report their status, they do not need to show proof of vaccination but will be asked to record the date they received their shots and the maker of the vaccine.

According to the U.S. Bureau of Labor Statistics, among establishments that required COVID-19 vaccinations for their employees to work onsite, 45.9% offered vaccination incentives. These incentives included financial incentives, paid time off, or allowing employees to remain on the clock to get vaccinated.

Exploring Santa Barbara: Montecito's Distance from the City

You may want to see also

Frequently asked questions

While there is no federal mandate requiring bank employees to be vaccinated, some banks have implemented their own vaccine mandates for employees. For example, Morgan Stanley and Goldman Sachs have required their employees to be vaccinated to return to the office.

Apart from Morgan Stanley and Goldman Sachs, other banks that have required employees to be vaccinated include JPMorgan Chase, Fifth Third, and PNC.

Some banks, like Morgan Stanley, have also required clients to be vaccinated to enter their premises. However, this is not a widespread policy among banks.