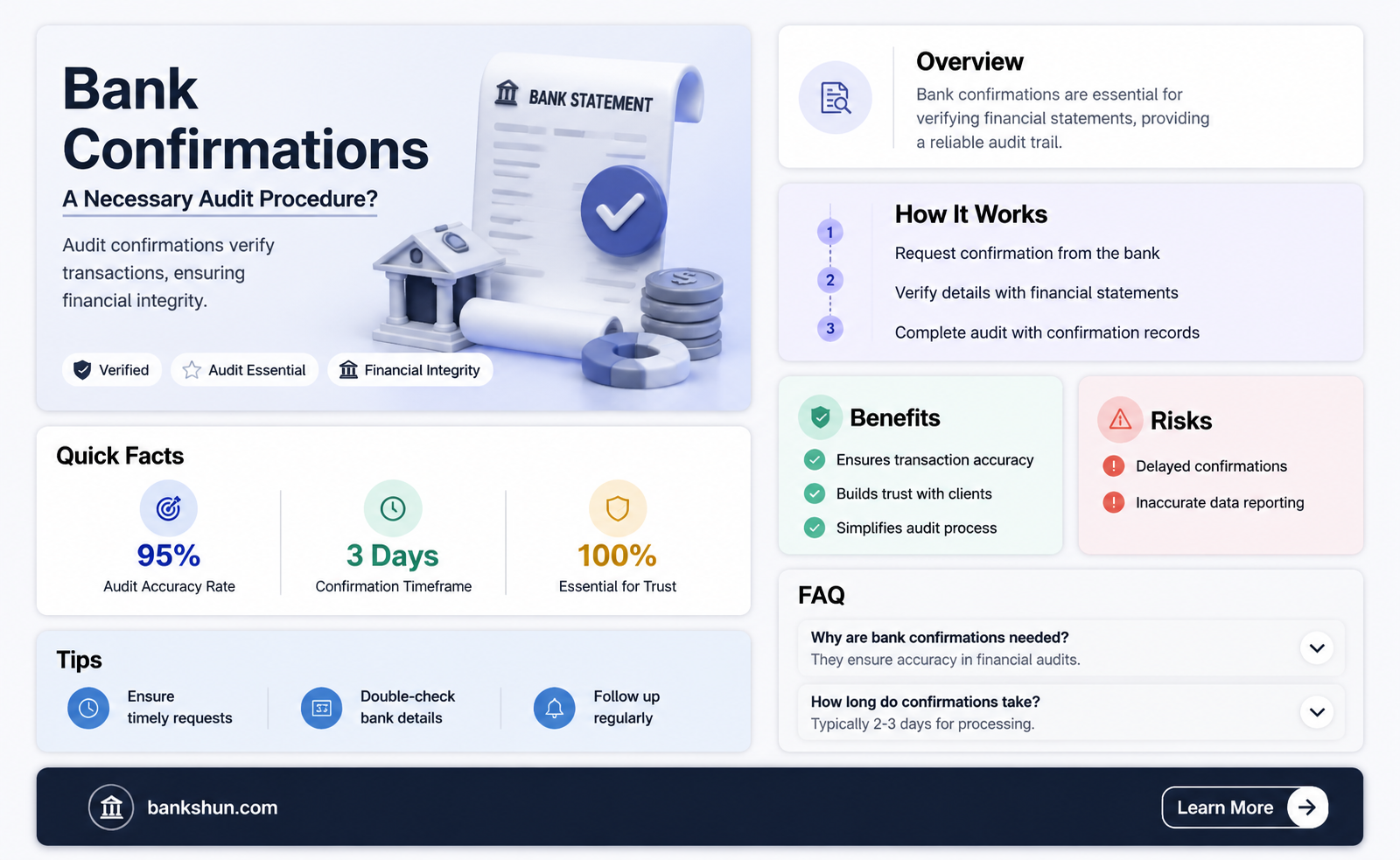

Bank confirmations are not a required procedure for audits, but they are often used to validate the information on bank statements received from a company. Auditors may choose to use bank confirmations when the risk of material misstatement is high, for a first-year audit, or for newly opened bank accounts. Bank confirmation letters are considered to be among the most persuasive forms of audit evidence, as they are received directly from a third party. Bank confirmations can also help address the completeness of the number of bank accounts, although most banks will not disclose accounts not listed on the confirmation. Auditors should maintain control over the confirmation requests and responses to minimise the risk of bias.

| Characteristics | Values |

|---|---|

| Are bank confirmations required for an audit? | No, bank confirmations are not a required audit procedure. |

| When should bank confirmations be sent? | When the risk of material misstatement is high, for any first-year audit client, or for newly opened bank accounts. |

| What are the alternatives to bank confirmations? | Inspecting documents (e.g. invoices, shipping records, contracts, cash receipts), reviewing subsequent cash receipts, performing analytical procedures, conducting physical observations. |

| What are confirmation letters? | Confirmation letters are among the most persuasive forms of audit evidence as they are received directly from a third party. |

| What are positive confirmations? | Recipients are asked to respond directly to the auditor, confirming whether they agree or disagree with the provided information. |

| What are negative confirmations? | Recipients only need to respond if they disagree with the information. A non-response is assumed as agreement. |

| What are blank confirmations? | Recipients are asked to provide the requested information directly to the auditor without specifying amounts or details. |

Explore related products

What You'll Learn

- Bank confirmations are not a required audit procedure

- Bank confirmations can be used to detect fraud

- Auditors can use alternative methods to verify information

- Confirmation letters are among the most persuasive forms of audit evidence

- Bank confirmations may be the most effective test of the existence of cash balances

![]()

Bank confirmations are not a required audit procedure

The decision to use bank confirmations depends on the risk assessment for the relevant cash assertions. Auditors should consider sending bank confirmations when the risk of material misstatement is high or for any first-year audit client or newly opened bank accounts. Additionally, bank confirmations can be useful in detecting fraud, as they can help identify fake bank statements.

When bank confirmations are not sent, auditors can use alternative methods to verify information. These methods include inspecting documents such as invoices, shipping records, contracts, and cash receipts; reviewing subsequent cash receipts for accounts receivable; performing analytical procedures such as analyzing financial data for trends; and conducting physical observations such as inventory counts.

The confirmation process involves preparing confirmation letters, which are considered persuasive forms of audit evidence as they are received directly from a third party. Positive confirmation requests require respondents to explicitly confirm or disagree with the provided information, while negative confirmation requests only require a response if there is a disagreement. Blank confirmation requests do not specify amounts or details and instead ask recipients to provide the requested information directly.

Wells Fargo: A Troubled Bank's Future?

You may want to see also

Explore related products

![]()

Bank confirmations can be used to detect fraud

Bank confirmations are not a required procedure for audits. However, they can be a powerful tool for auditors to provide independent evidence to substantiate various financial statement assertions. They are used to validate the information on the bank statements received from the company.

For example, in 2013, James Shepherd, an investment company owner, defrauded over 100 investors of approximately $6 million. He misused funds and tricked his company's external auditors with fake bank confirmation responses. The fraudulent financial statement reflected a $6,041,850 cash balance when in reality, the fund had less than $100,000. This example illustrates how bank confirmation responses can be manipulated to conceal fraud.

Additionally, bank confirmations can address the completeness of the number of bank accounts if the bank discloses all accounts, even those not listed on the confirmation. This is important because fraudsters may funnel money into fake bank accounts. However, most banks will not disclose accounts not listed on the confirmation, and alternative procedures may be necessary to detect fraud in these cases.

To ensure the effectiveness of bank confirmations in detecting fraud, auditors should maintain control over the confirmation requests and responses to minimize the possibility of interception and alteration. Positive confirmations, where recipients are asked to explicitly agree or disagree with the provided information, are considered more reliable. Blank confirmations may also be used to mitigate the risk of incorrect information being signed and returned.

Crafting a Compelling Resume: Adding a Minor for Banking Roles

You may want to see also

Explore related products

![]()

Auditors can use alternative methods to verify information

Bank statements are considered a reliable source of a company's financial transactions and are essential during financial audits. They are used to prevent fraud, identify mistakes in financial records, and ensure compliance with regulatory requirements. While bank confirmations are a powerful tool for auditors, they are not always necessary, and alternative methods can be used to verify information.

Auditing standards generally assert that the reliability of audit evidence is increased when obtained from independent sources outside the entity. However, there are characteristics of standard bank confirmations that may make them less reliable in some circumstances. For example, financial institutions often add disclaimers or restrictions to responses, limiting responsibility for their accuracy. Additionally, there is a risk of bias if responses are intercepted and altered.

In situations where a third party does not provide the requested confirmation or disagrees with the information, auditors can employ alternative methods to verify information. These may include:

- Inspecting documents: Auditors can review invoices, shipping records, contracts, cash receipts, or other relevant information.

- Reviewing subsequent cash receipts: Auditors can inspect documentation for product delivery, services performed, or voucher payments subsequent to year-end bank statements to substantiate values being asserted.

- Performing analytical procedures: This involves analyzing financial data to identify trends and can include sales cutoff tests for accounts receivable.

- Conducting physical observations: Auditors can perform inventory counts or observe processes to gather evidence.

- Interviewing management and employees: Auditors can gather information directly from key individuals within the organization.

- Expanding sample sizes or performing additional tests: Increasing the scope or number of tests can provide further assurance.

Furthermore, advancements in technology have introduced automated bank statement verification. This utilizes advanced algorithms and intelligent document processing to identify discrepancies, improving accuracy and efficiency. Automated tools simplify the reconciliation process, saving time and reducing errors, allowing accountants to focus on strategic activities.

In conclusion, while bank confirmations can be a valuable tool for auditors, they are not always necessary. Auditors can employ alternative methods to verify information effectively, utilizing independent sources and analytical procedures to ensure the accuracy and integrity of a company's financial records.

Stride Bank and Chime: What's the Difference?

You may want to see also

Explore related products

![]()

Confirmation letters are among the most persuasive forms of audit evidence

Confirmation letters are also used to confirm the existence and terms and conditions of the related-party balances within the entity being audited. The auditor may use positive or negative confirmations or a combination of both. Positive confirmation requests require the respondent to reply by either conforming to the information already provided within the confirmation letter or providing data themselves. Positive confirmation requests are considered more reliable as they require explicit acknowledgment from the respondent. Negative confirmation requests only require the respondent to respond if they disagree with the information presented. Blank confirmation requests do not specify amounts or details and instead ask recipients to provide the requested information directly to the auditor.

The confirmation letter shall include relevant information that the recipient can clearly confirm, such as the exact and full name of the organisation being audited. Confirmations help in identifying discrepancies in accounting records, existence, and rights and obligations. Obtaining responses is a critical stage in terms of information reliability. The auditor must take the necessary steps to obtain control over the process.

Bank confirmations may be the most effective test of the existence of cash balances and the completeness of debt, contingent liabilities, and other disclosure matters. However, they are only effective when used properly, cash balances are material, and risk considerations warrant their use. Bank confirmations are not a required audit procedure, and alternative procedures may be applied when the risk of material misstatement and fraud is low.

Banking Apps: Safe or Not?

You may want to see also

Explore related products

![]()

Bank confirmations may be the most effective test of the existence of cash balances

Bank confirmations are not a required procedure for audits. However, they are often used to validate the information on bank statements received from the company. They are considered one of the most persuasive forms of audit evidence, as they are received directly from a third party.

Bank confirmation letters can be used to confirm the existence and terms and conditions of related-party balances within the entity being audited. Positive confirmation requests require the respondent to either confirm or deny the information in the letter, while negative confirmation requests only require a response if the respondent disagrees with the information. Blank confirmation requests do not specify amounts or details and instead ask the recipient to provide the requested information directly. Positive confirmations are considered more reliable, as they require explicit acknowledgment, whereas negative confirmations are considered less reliable because a non-response is assumed as agreement.

However, there are some characteristics of standard bank confirmations that may make them less reliable in certain circumstances. For instance, financial institutions often add disclaimers or restrictions to the accuracy of their responses. Additionally, there is a risk that recipients of positive confirmation requests may sign and return the confirmation without verifying the information. In such cases, alternative procedures may be more effective in reducing the risk of material misstatement to an acceptably low level. These alternative procedures may include inspecting documents, reviewing subsequent cash receipts, performing analytical procedures, or conducting physical observations.

Bank Assets: Understanding the Core Components

You may want to see also

Frequently asked questions

No, bank confirmations are not a required audit procedure. Auditors can use alternative methods to verify information, such as inspecting documents, reviewing cash receipts, performing analytical procedures, or conducting physical observations.

Bank confirmations should be sent when the risk of material misstatement is high, for any first-year audit client, or for newly opened bank accounts. They can also be useful in detecting fraud.

There are three types of audit confirmations: positive, negative, and blank confirmations. Positive confirmations require recipients to explicitly agree or disagree with the provided information, while negative confirmations only require a response if there is a disagreement. Blank confirmations do not specify amounts or details and instead request that the recipient provides the information directly to the auditor.