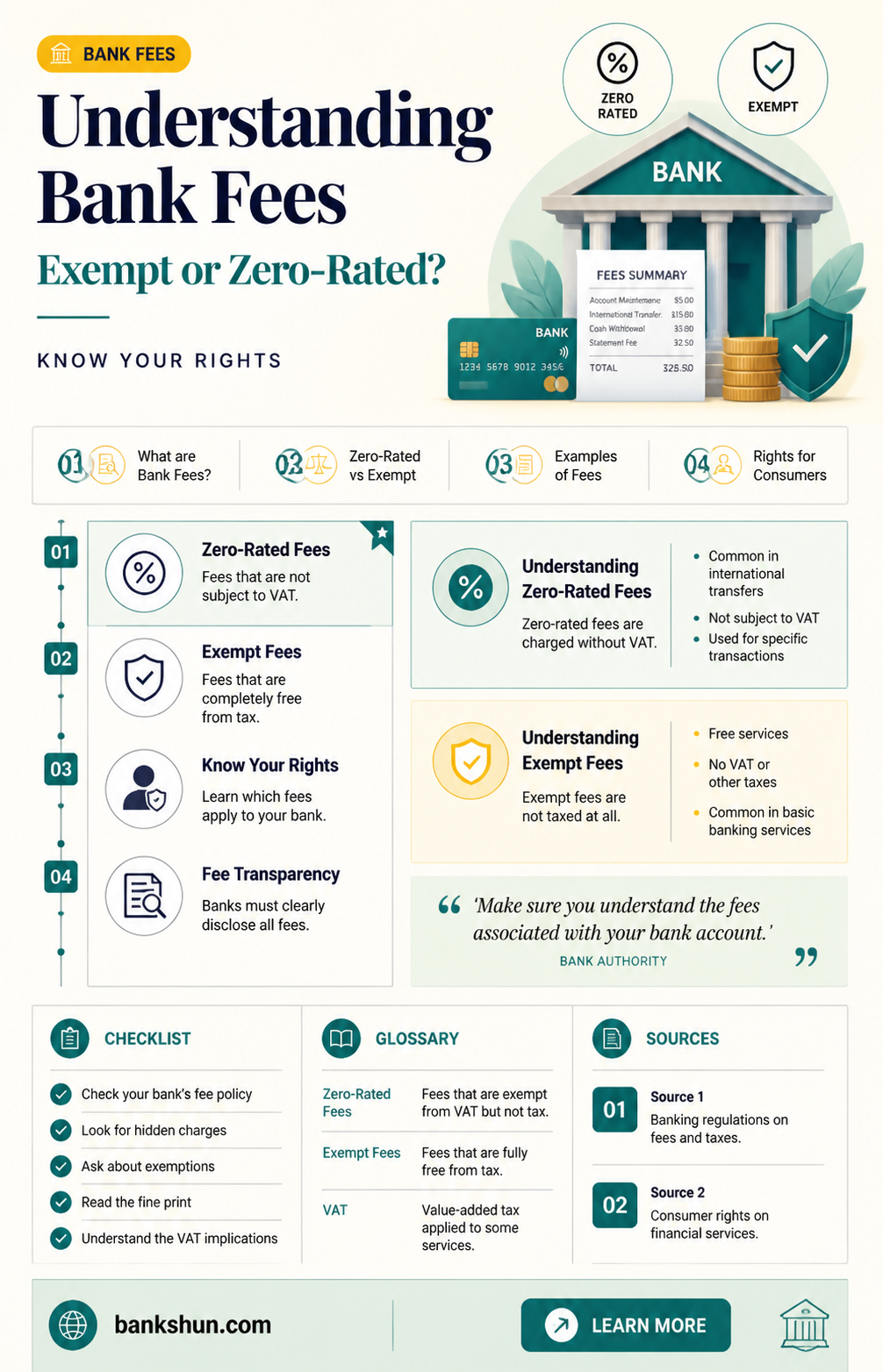

In the context of Value-Added Tax (VAT), zero-rated items are taxable but rated at 0%, while exempt items are not subject to any rate of VAT. Bank fees are generally considered exempt from VAT. This means that no VAT is charged on bank fees, and the financial institution cannot claim input VAT as a credit or refund. However, certain services connected to financial services may be zero-rated or taxable. For example, the issue of certain bank notes or coins may be taxable, and preparatory services carried out before an exempt financial transaction are also taxable.

Are bank fees exempt or zero-rated?

| Characteristics | Values |

|---|---|

| VAT charged | No |

| VAT reclaim | No |

| VAT return | No |

| Examples | Bank charges, PayPal fees, bank notes or coins, ATM convenience fees, interchange fees, reciprocity fees |

| T-Code | T9 or T2 |

Explore related products

What You'll Learn

![]()

Bank fees are exempt items

It is important to distinguish between zero-rated and exempt items when recording transactions within a bookkeeping system for VAT purposes. While neither will have VAT charged on them, they are treated differently for VAT calculations.

In the context of financial services, VAT exemption applies to services that include an element of making payments or transfers between bank accounts. Many charges made by banks, building societies, or similar organizations in connection with the operation of a current, deposit, or savings account will be exempt. For example, ATM providers' convenience fees, interchange fees, or reciprocity fees are often exempt.

However, it is important to note that there are exceptions to this. Certain charges, such as those for issuing specific types of financial certificates or the extra cost of special printing for cheque books, may not be exempt and could be subject to VAT.

The distinction between exempt and zero-rated items is crucial for businesses to ensure they are applying the correct VAT treatment.

The Federal Reserve Bank: Its Role and Responsibilities

You may want to see also

Explore related products

![]()

Bank charges are exempt from VAT

In the context of bank charges, VAT exemption implies that financial services, including bank charges and interest, are generally not subject to VAT. This exemption extends to various fees associated with the operation of current, deposit, or savings accounts. Examples of exempt fees include charges for overdrafts, transfers between accounts, and ATM usage.

However, it's important to note that there are exceptions to this exemption. Certain services provided by banks may be subject to VAT, such as the issue of specific financial certificates or charges for special printing of cheque books. These exceptions highlight the complexity of VAT application, which often includes provisions to provide relief to specific sectors or products.

The distinction between VAT exemption and zero-rated VAT is crucial for businesses. Businesses dealing with zero-rated goods can reclaim input VAT, reducing costs, while those offering exempt goods cannot, potentially leading to higher operating expenses. This distinction also impacts consumers, as VAT on zero-rated items can be adjusted by the government, whereas exempt items have no VAT applied at all.

While bank charges are generally VAT-exempt, it is always advisable to consult the latest guidelines and regulations, as VAT rules can be intricate and subject to change.

The Owner of Fidelity Bank: A Profile

You may want to see also

Explore related products

![]()

VAT exemption is simpler to administer

While the application of VAT can be complex, VAT exemption is generally simpler to administer than zero-rated VAT. This is because VAT exemption involves no VAT in the transaction, whereas zero-rated VAT involves charging VAT at a rate of 0% and reclaiming input VAT.

VAT exemption is a mechanism that allows certain goods and services to be exempt from VAT altogether. When a business provides a VAT-exempt product or service, it does not charge VAT to the customer and cannot recover any VAT incurred on related expenses. Common VAT-exempt items include insurance, postage services, rent, education, and bank charges. VAT exemptions are typically applied to essential goods and services that are considered vital for the welfare of society.

For example, if a business sells only VAT-exempt goods or services, it is considered an exempt business and will not be able to register for VAT. This means the business cannot reclaim any VAT on purchases or expenses. However, this does not prevent the business from claiming VAT refunds for other taxable activities.

In contrast, zero-rated VAT is subject to VAT at a rate of 0%. While businesses do not collect VAT on zero-rated supplies, they can reclaim the VAT paid on purchases, reducing costs and boosting profits. Zero-rated VAT can be advantageous for businesses, especially in industries heavily reliant on inputs subject to VAT, such as manufacturing or construction.

In summary, VAT exemption is simpler to administer as it involves no VAT in the transaction, whereas zero-rated VAT involves managing VAT reclamation, which can be complex.

Repo Cars: Buying Directly from Banks

You may want to see also

Explore related products

![Less Than Zero [DVD]](https://m.media-amazon.com/images/I/51JX98YDC5L._AC_UY218_.jpg)

![]()

Zero-rated VAT is more complex

Zero-rated VAT can be a valuable benefit for businesses, especially those in industries heavily reliant on inputs subject to VAT, such as manufacturing or construction. It can improve their cash flow and competitiveness by reducing their tax costs and ultimately enabling them to offer more competitive prices to consumers. For example, governments commonly lower the tax burden on low-income households by zero-rating essential goods, such as food, utilities, or prescription drugs.

Businesses dealing in zero-rated goods can reclaim input VAT, potentially lowering costs. This mechanism allows businesses to recover the VAT they have paid throughout the supply chain, thereby reducing their overall tax liability. However, it is important to note that businesses must include their zero-rated transactions in their regular VAT returns to ensure compliance.

Determining whether items are zero-rated or exempt from VAT can be complex, and it is recommended to consult with VAT specialists or review the relevant legislation. Proper classification, record-keeping, and expert advice are essential to ensure correct VAT compliance and prevent potential financial penalties.

The World Bank's Mission: Eradicate Poverty, Build Prosperity

You may want to see also

Explore related products

![]()

Zero-rated VAT can reduce business costs

Zero-rated VAT can be highly advantageous for businesses, reducing their costs and enhancing their cash flow and competitiveness. When a good or service is zero-rated, it means that while it is technically subject to VAT, it is charged at a rate of 0%. This means that while the customer does not pay VAT on the item, the supplier can still reclaim the VAT they have paid on their own purchases related to those sales. This mechanism allows businesses to recover the VAT they have paid throughout the supply chain, thereby reducing their overall tax liability.

For example, common zero-rated items include food, books, public transport, and clothing (children's clothing and protective clothing). Businesses selling these items can reclaim the VAT they have paid on their purchases, which may include raw materials, equipment, office supplies, and services. This can be particularly beneficial for businesses in industries heavily reliant on VAT-subject inputs, such as manufacturing or construction.

In contrast, VAT-exempt items do not allow for VAT reclaims. This can lead to higher costs for both businesses and consumers. VAT exemption is generally simpler to administer as no VAT is involved in the transaction. However, it can sometimes raise prices and revenues as it breaks the VAT's chain of credits on input purchases. VAT exemptions are typically applied to essential goods and services that are considered vital for the welfare of society, such as healthcare, education, and insurance services.

Bank charges are generally considered VAT-exempt and must be posted with T9, meaning they will not appear on the VAT return. However, it is important to note that the specific items or services exempt from VAT can vary from one country to another, as tax laws and regulations differ.

Overall, zero-rated VAT can indeed reduce business costs by allowing them to reclaim input VAT and improve their cash flow and pricing competitiveness. Accurate classification, record-keeping, and expert advice are essential for businesses to ensure they are applying the correct VAT treatment and optimizing their financial position.

Federal Reserve Banks: How Many Are There?

You may want to see also

Frequently asked questions

No, bank fees are exempt from VAT.

Zero-rated supplies are subject to VAT at a rate of 0%, while exempt supplies are not subject to any VAT rate.

Yes, suppliers can reclaim the VAT paid on purchases for zero-rated supplies.

No, suppliers cannot reclaim VAT on exempt items.

Some examples of zero-rated items include food, books, public transport, and clothing.

![Prime Screen [5 Pack] 10 Panel Saliva Oral Fluid Test Kit, E&I Exempt for Workplace and Insurance Use AMP, BAR, COC, MDMA, MET (Meth), MTD, OPI, OXY, PCP (Phencyclidine), THC (Marijuana) - QODOA-10106](https://m.media-amazon.com/images/I/61J34scD7uL._AC_UY218_.jpg)