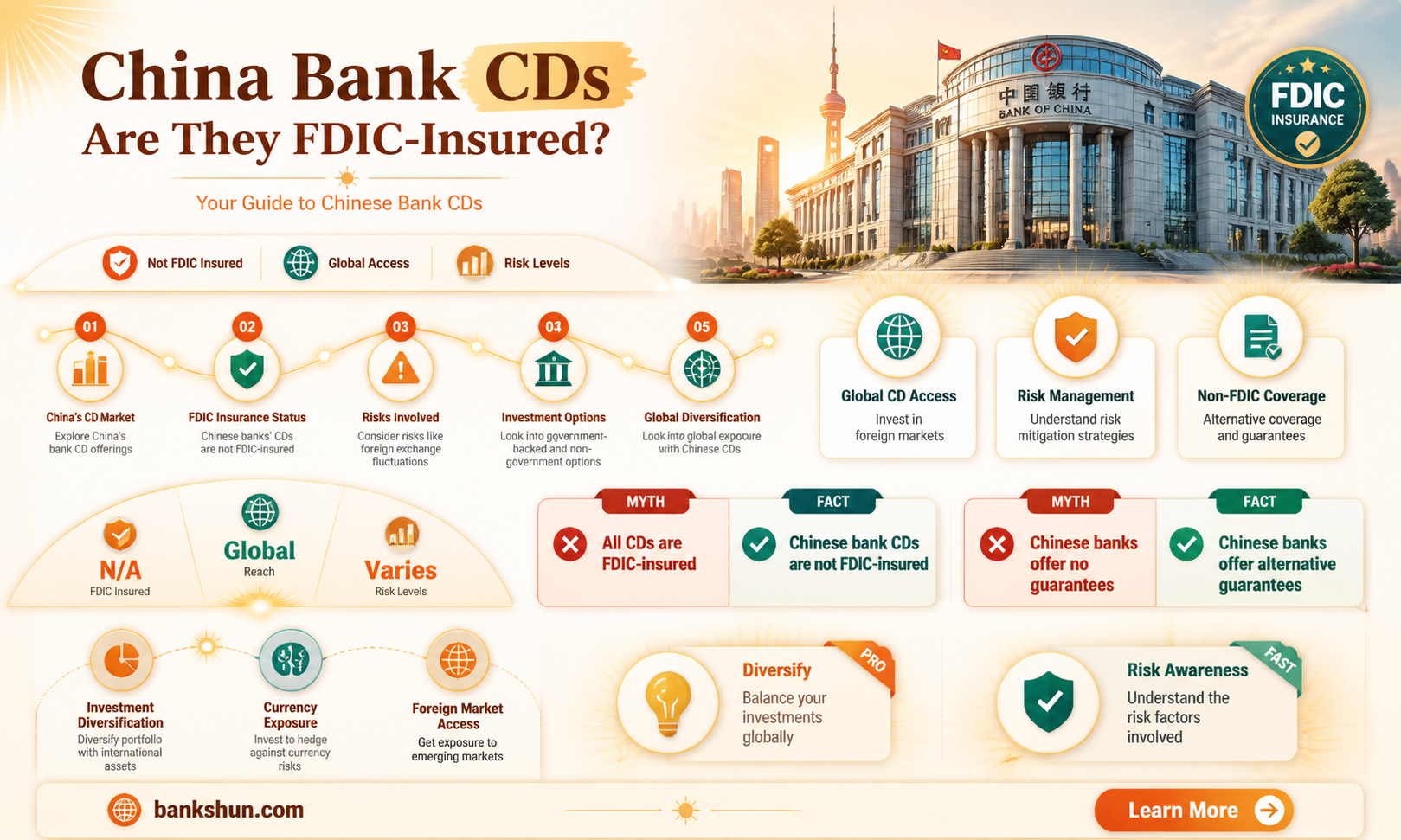

The Bank of China offers a range of financial products to its customers, including certificates of deposit (CDs) and corporate demand deposit and time deposit products. The Bank of China's CDs have terms ranging from one month to four years, and customers can access their CD account details through the bank's online banking system. Additionally, the bank provides corporate clients with access to FDIC insurance coverage for their multi-million-dollar deposits through its Insured Case Sweep Services (ICS) and Certificate of Deposit Account Registry Service (CDARS) programs. This ensures that their funds are protected and insured by multiple financial institutions.

| Characteristics | Values |

|---|---|

| FDIC Insurance | The Bank of China offers FDIC insurance coverage for multi-million-dollar deposits through its Insured Cash Sweep (ICS) services and Certificate of Deposit Account Registry Service (CDARS) |

| Terms | The Bank of China offers CDs with terms ranging from 1 month to 4 years |

| Minimum Deposit | A minimum deposit is required to open a CD, and it varies with the term of the CD |

| Interest | Interest is not compounded. Accrued interest is credited to the account at maturity |

| Fees | There are no monthly maintenance fees |

| Early Withdrawal | Penalties may apply for early withdrawals |

Explore related products

What You'll Learn

![]()

Bank of China CDs and FDIC insurance

The Bank of China offers a range of financial products to its customers, including Certificates of Deposit (CDs). CDs are a type of savings account that typically offers a higher interest rate than a regular savings account. The Bank of China offers CDs with terms ranging from one month to four years, providing customers with flexibility to meet their financial needs.

When considering a CD, it is important to understand the level of protection offered for your deposited funds. In the United States, the Federal Deposit Insurance Corporation (FDIC) provides insurance coverage for depositors, guaranteeing the safety of their money up to a certain limit. This insurance coverage is a critical safety net, protecting customers' funds in the event of a bank failure or financial crisis.

The Bank of China, through its participation in specific programs, ensures that its customers' deposits are FDIC-insured. By utilising the Certificate of Deposit Account Registry Service (CDARS) and Insured Case Sweep Services (ICS), the bank enables its customers to access FDIC insurance coverage for their multi-million-dollar deposits. These programs provide an added layer of security, giving customers peace of mind that their funds are protected.

It is worth noting that FDIC insurance coverage has certain limitations and requirements. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have deposits exceeding $250,000, you may want to consider dividing your funds across multiple FDIC-insured institutions to ensure full coverage. Additionally, it is always advisable to review the specific terms and conditions associated with any financial product, including CDs, to understand the level of protection offered and any applicable exclusions or limitations.

Jos. A. Bank: A Brand Worth Trusting?

You may want to see also

Explore related products

![]()

FDIC insurance coverage for multi-million-dollar deposits

The Federal Deposit Insurance Corporation (FDIC) provides insurance coverage for deposits in FDIC-insured banks. This coverage is not limited to US citizens or residents, and since its founding in 1933, no depositor has lost any FDIC-insured funds. The FDIC maintains the Deposit Insurance Fund (DIF), which insures deposits and protects depositors of FDIC-insured banks. The standard deposit insurance amount is $250,000 per depositor, per FDIC-insured bank, per ownership category. However, if you have multiple accounts in different ownership categories, you may qualify for more than $250,000 in insurance coverage. For example, if you have a single ownership account at one FDIC-insured bank and a joint ownership account at the same bank, you will be insured for up to $250,000 for your single ownership account and separately for your ownership interest in the joint account.

FDIC insurance covers deposit accounts, including checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). It is important to note that FDIC insurance does not cover investments, even if they were purchased at an insured bank. Additionally, deposits that exceed $250,000 and are linked to trust documents or deposits established by a third-party broker may require additional time for the FDIC to determine the insurance coverage. In such cases, the FDIC may request supplemental information from the depositor.

To determine if a bank is FDIC-insured, individuals can inquire with a bank representative, look for the FDIC sign at the bank, or use the FDIC's BankFind tool, which provides detailed information about insured institutions. The FDIC also offers an online Electronic Deposit Insurance Estimator (EDIE) to help calculate insurance coverage for different ownership categories.

Regarding multi-million-dollar deposits, FDIC insurance coverage extends beyond $250,000 in certain cases. For trust owners, the insurance coverage is calculated by multiplying $250,000 by the number of eligible beneficiaries, with a maximum insurance amount of $1,250,000 for five or more beneficiaries. It is important to note that the same beneficiary can be counted multiple times across different trust accounts at the same bank, but they only count once per owner for insurance purposes.

In summary, FDIC insurance coverage for multi-million-dollar deposits depends on the number of accounts, ownership categories, and beneficiaries involved. While the standard insurance limit is $250,000, certain structures allow for higher coverage amounts. It is recommended to use the FDIC's tools and resources to calculate specific coverage amounts for multi-million-dollar deposits.

Who is the Current CEO of Wells Fargo Bank?

You may want to see also

Explore related products

![]()

Insured Cash Sweep Services (ICS)

Insured Cash Sweep (ICS) is a service that banks and savings associations use to insure deposits that exceed the Federal Deposit Insurance Corporation's (FDIC) coverage limit of $250,000 per depositor, per institution. ICS accounts allow customers to deposit, manage, and withdraw funds from a single primary account, while the bank spreads the funds across a network of FDIC-insured banks, ensuring that each institution holds up to $250,000. This service provides peace of mind, as it offers full FDIC insurance on deposits, with some accounts providing coverage of up to $150 million.

ICS accounts are available at various banks, including those that participate in the IntraFi Network, such as Axos Bank and Live Oak Bank. To open an ICS account, customers typically need to opt into a sweep account and sign an agreement allowing the bank to transfer their funds to partner banks. While neobanks also offer ICS accounts through their partners, FDIC insurance only applies if the partner bank fails, and accessing funds from a failed fintech company could be challenging.

When choosing an ICS account, it's essential to consider the sweep preferences. Customers can usually select between demand and savings sweep accounts. Demand accounts offer unlimited withdrawals, making them ideal for operational funds. On the other hand, savings sweep accounts place funds in money market accounts with withdrawal limits but often provide better interest rates, making them suitable for emergency savings.

The ICS service also enables customers to earn interest on their deposits. While the accounts are interest-earning, the yield may vary depending on the account balance. For example, the Holdings High-Yield Cash Account offers an APY of 1.5% on all balances, while Live Oak Bank's ICS account offers a slightly lower yield of 3.20% APY.

Overall, Insured Cash Sweep Services provide a valuable option for individuals or businesses seeking to maximize FDIC insurance coverage on their deposits while also earning competitive interest rates. By utilizing ICS accounts, customers can rest assured that their funds are fully protected and easily accessible through a single primary account.

CRA in Banking: What It Stands For and Why It Matters

You may want to see also

![]()

Certificate of Deposit Account Registry Service (CDARS)

The Certificate of Deposit Account Registry Service (CDARS) is a US for-profit service that breaks up large deposits and places them across a network of over 3000 banks and savings associations in the United States. This allows depositors to deal with a single bank that participates in CDARS while avoiding having funds above the Federal Deposit Insurance Corporation (FDIC) deposit insurance limits in any one bank.

CDARS allows a business to invest in Certificates of Deposits (CDs) held by multiple FDIC-insured banking institutions, achieving full FDIC coverage for the total sum. Before the advent of fintech, companies seeking FDIC coverage for sums over $250,000 had to manage relationships with multiple banks and multiple bank statements. With CDARS, businesses can make a single deposit, which is then automatically distributed to enough financial institutions to achieve full FDIC coverage.

CDARS offers a range of maturities between 4 weeks and 3 years. However, there are drawbacks to using CDARS. Firstly, the invested funds are locked in CDs until maturity, and early withdrawal incurs a penalty. Secondly, businesses are limited to 7 term options for their CDs, which may be prohibitive for those requiring liquidity on multiple time horizons. Finally, banks pay a set fee for access to CDs in CDARS, which can reduce returns on investment compared to lower-cost alternatives.

While the FDIC has not endorsed any particular method of maximizing FDIC insurance coverage, it has confirmed that deposits placed through the IntraFi Network, of which CDARS is a part, are eligible for "pass-through" FDIC insurance. IntraFi is not an FDIC-insured bank, but deposit insurance covers the failure of an insured bank.

Regarding the Bank of China, while I could not find specific information on whether its CDs are FDIC-insured, the bank does offer CDs with terms ranging from 1 month to 4 years.

Capitalizing on Banking Failures: Strategies for the Savvy Investor

You may want to see also

![]()

Bank of China CDs maturity and early withdrawals

Certificates of Deposit (CDs) are a type of deposit account that offers a higher interest rate than other types of deposit accounts. CDs are payable at the end of a specified amount of time, referred to as the term. The Bank of China offers IRA CDs with terms ranging from 1 month to 4 years. These CDs offer tax benefits and automatic renewal at maturity. The minimum deposit for an IRA CD is $1,000, and there is no monthly maintenance fee.

Early withdrawals from CDs are generally subject to penalties and penalty taxes. For example, at HSBC China, if you make an early withdrawal from a Personal Large-Denomination CD, the principal and interest could be lower than your purchase price, resulting in a substantial loss. Therefore, it is recommended to retransfer the product instead of withdrawing it early.

Similarly, Bank of America charges a penalty for early withdrawals from CDs. However, there may be ways to avoid this penalty by carefully choosing the type of CD. For example, a "step-up coupon schedule" CD pays a fixed interest rate for a defined period, after which the interest rate increases. This option provides flexibility and a higher rate of return, even if you cannot access your funds during the term.

It is important to note that CDs are FDIC-insured up to applicable limits, which is currently $250,000 per account owner, per institution. This insurance coverage was made permanent in 2010 and applies to both bank CDs and brokered CDs. By purchasing CDs from different issuing banks, you can effectively expand your FDIC protection beyond the $250,000 limit in a single account.

Best Bank CD Rates: Compare and Maximize Your Returns

You may want to see also

Frequently asked questions

Yes, the Bank of China offers FDIC insurance on its CDs.

The FDIC insurance coverage provided by the Bank of China on its CDs varies depending on the specific product and financial institution involved. For example, through its Insured Case Sweep Services (ICS), the bank offers FDIC insurance coverage for multi-million-dollar deposits in Demand Deposit Accounts (DDAs) or Money Market Deposit Accounts (MMDAs).

The ICS service provides customers with access to FDIC insurance coverage from multiple financial institutions, offering a compelling return potential for their multi-million-dollar funds.

The Bank of China offers CDs with terms ranging from one month to four years, providing flexibility for customers' financial needs.

Customers can conveniently access their CD account information by enrolling in the Bank of China's online banking system.