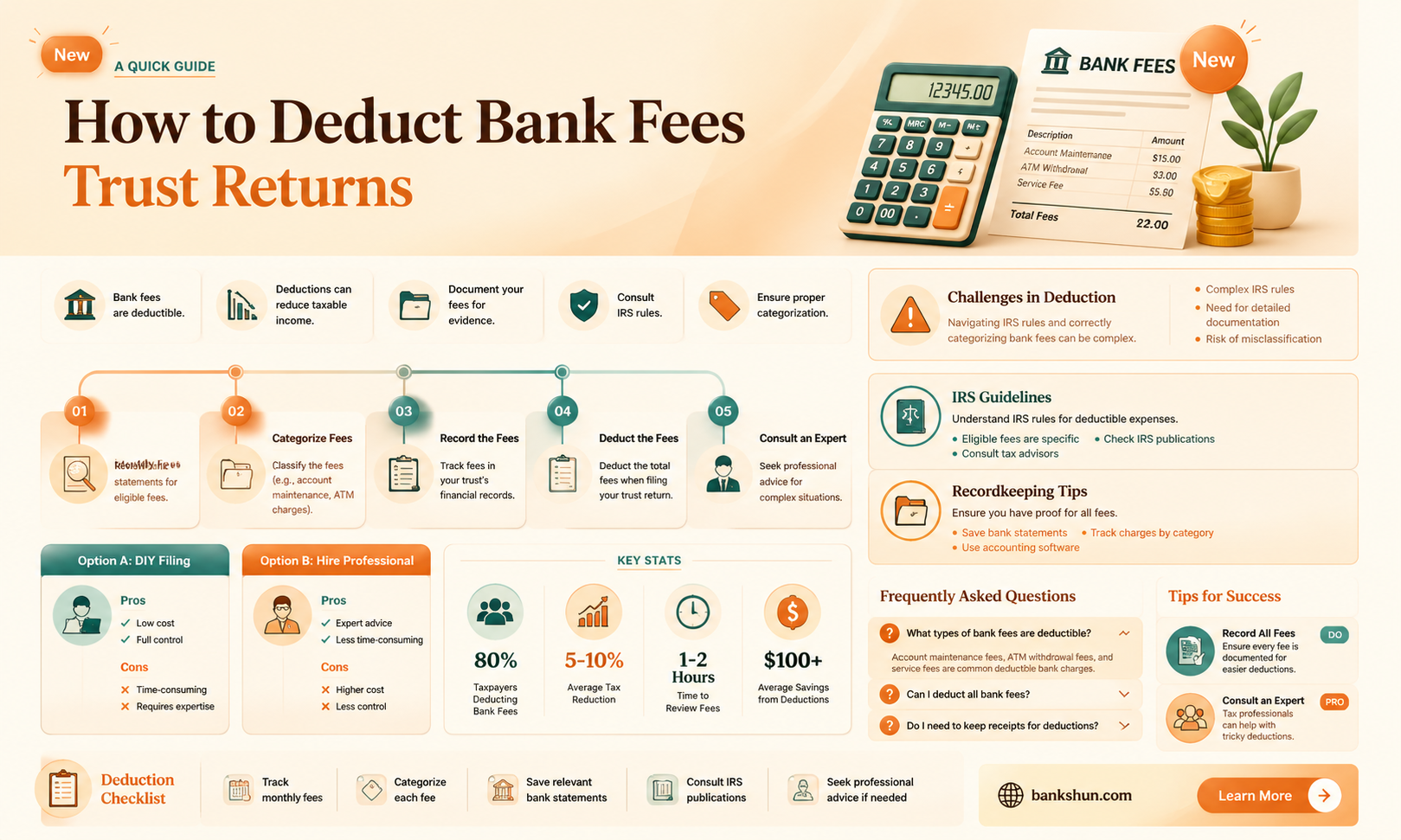

The deductibility of bank fees on trust returns is a complex topic that requires careful consideration of applicable tax laws and regulations. In the United States, the Internal Revenue Service (IRS) provides guidance on this matter through various forms, instructions, and notices. For example, Form 1041 and its accompanying schedules outline specific rules for trusts, including electing small business trusts (ESBT), bankruptcy estates, and Alaska Native Settlement Trusts. The Tax Cuts and Jobs Act of 2017, also known as the TCJA, introduced changes to deductions for trusts and estates, impacting trustee fees and charitable contributions. Understanding these regulations is essential for trustees to accurately file tax returns and claim allowable deductions, such as administrative expenses and certain fiduciary expenses. However, uncertainties remain, particularly regarding the interpretation of Section 67 and its impact on itemized deductions. As a result, trustees and tax professionals must stay updated with IRS clarifications and rulings to ensure compliance and optimize tax benefits.

| Characteristics | Values |

|---|---|

| Bank fees deductible on trust return | Not explicitly mentioned |

| Trustee fees deductible | Yes |

| Trustee fees deductible from TAI | Yes |

| Trustee fees deductible from DNI | No |

| Tax rate for trusts | Changed very little |

| Tax rate for individuals | Decreasing |

| Charitable deductions | Allowed only if the trust document explicitly allows for it |

| Section 67(e) | Excludes fiduciary-specific expenses |

| Section 67(g) | Disallows investment management and advisory fees as deductions |

| Section 645 | Election period available |

| Section 646 | Special tax treatment for Alaska Native Settlement Trusts |

| Section 503 of title 11 of the U.S. Code | Allows bankruptcy estate a deduction for administrative expenses |

Explore related products

What You'll Learn

![]()

The impact of the Tax Cuts and Jobs Act of 2017 on bank fees

The 2017 Tax Cuts and Jobs Act (TCJA) brought about several changes to the tax code, impacting the tax planning strategies of millions of Americans. While the act did not directly mention bank fees, it did make changes to deductions, depreciation, expensing, tax credits, and other tax items that could have an impact on how bank fees are treated.

One of the key impacts of the TCJA on bank fees is through its effect on itemized deductions. The act introduced a $10,000 cap on state and local tax (SALT) deductions for married couples filing jointly and a $5,000 cap for those filing separately. This includes a range of fees, such as homeowners association fees, insurance, and maintenance, which may be considered bank fees in certain contexts. The TCJA also created confusion regarding the deductibility of expenses under Sec. 67, with some expenses that were previously deductible, such as tax preparation fees, appraisal fees, and certain fiduciary expenses, potentially being disallowed under Sec. 67(g).

Another way the TCJA may impact bank fees is through its effect on trusts and estates. The act includes a provision, Sec. 67(g), which clarifies the ability of trusts and estates to deduct certain expenses. This could impact the deductibility of various fees associated with trusts, including potential bank fees. Trusts with state and local tax (SALT) liabilities may be particularly affected, as the TCJA created a $10,000 SALT limitation for trusts, leading to planning considerations to minimize these taxes.

Additionally, the TCJA introduced changes to individual tax brackets, lowering them across the board. This could impact the overall tax liability of individuals and potentially affect their ability to deduct certain bank fees. The act also introduced a higher standard deduction, which may lead to more taxpayers taking the standard deduction instead of itemizing their deductions, including any potential bank fee deductions.

Overall, while the 2017 Tax Cuts and Jobs Act did not specifically target bank fees, its wide-ranging changes to the tax code could have indirect impacts on the deductibility and treatment of bank fees. Individuals and businesses are advised to review the tax reform changes and plan their tax strategies accordingly.

Understanding Banking Consent Orders: Explained

You may want to see also

Explore related products

![]()

Tax-deductible charitable contributions

Trusts and estates are allowed to make tax-deductible charitable contributions only if the trust document explicitly allows for it. Many trust documents do not have this provision. While the IRS is attempting to close the loophole allowing for a state tax credit combined with a federal charitable deduction, it may be beneficial for a trust to consider this option.

In most cases, the amount of charitable cash contributions taxpayers can deduct on Schedule A as an itemized deduction is limited to a percentage (usually 60%) of the taxpayer’s adjusted gross income (AGI). Qualified contributions are not subject to this limitation. Individuals may deduct qualified contributions of up to 100% of their adjusted gross income. A corporation may deduct qualified contributions of up to 25% of its taxable income. Contributions that exceed that amount can carry over to the next tax year.

Contributions to certain private foundations, veterans organizations, fraternal societies, and cemetery organizations are limited to 30% of adjusted gross income. The 50% limitation applies to all public charities, all private operating foundations, certain private foundations that distribute the contributions they receive to public charities and private operating foundations within 2-1/2 months following the year of receipt, and certain private foundations where the contributions are pooled in a common fund, and the income and corpus are paid to public charities.

In addition to deducting cash contributions, taxpayers can generally deduct the fair market value of any other property they donate to qualified organizations. For contributions of cash, check, or other monetary gifts, taxpayers must maintain a record of the contribution, such as a bank record or receipt from the charity. For non-cash contributions exceeding $500, taxpayers must fill out Form 8283, Noncash Charitable Contributions, and attach it to their tax return. If the deduction exceeds $5,000 per item or group of similar items, a qualified appraisal of the item is required.

To claim a deduction for charitable donations, taxpayers must have donated to an IRS-recognized charity and received nothing in return for their gift. Taxpayers must itemize deductions on Schedule A (Form 1040) to deduct charitable contributions. For contributions of $250 or more, taxpayers must obtain and keep a contemporaneous written acknowledgment from the qualified organization indicating the amount of cash or description of property contributed.

Capital One Banks: Which States Have Branches?

You may want to see also

Explore related products

![]()

Trustee fees

The IRS allows for the deduction of administrative expenses that are incurred only because there is a trust or estate. These expenses are not considered miscellaneous itemized deductions, which are rendered non-deductible by the TCJA.

According to Regs. Sec. 1.67-4, deductible trustee fees include costs such as tax preparation fees for most returns, appraisal fees, and certain fiduciary expenses. Tax preparation fees specifically refer to the preparation of trust tax returns (Form 1041). It is important to note that costs that are typically incurred by an individual holding the same property, such as homeowners association fees, insurance, and maintenance, are not deductible.

When a trust terminates during the election period, the trustee must file a final Form 1041. This form includes the entity information, the checked "Final return" box, and the appropriate signatures and dates. However, items of income, deduction, and credit are not reported on this form. Instead, they are reported on the related estate's return.

In the case of an electing trust, the trustee files Form 1041 as if it were an estate if no executor has been appointed for the related estate. The trustee can choose the fiscal year as the trust's tax year during the election period.

Notary Services: Are They Available at All Banks?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Investment management and advisory fees

To clarify, expenses that are paid or incurred in the administration of a trust, and that would not have been incurred if the property were not held in such a trust, are deductible under Sec. 67(e)(1). This includes costs such as tax preparation fees for most returns, appraisal fees, and certain fiduciary expenses outlined in Regs. Sec. 1.67-4.

On the other hand, costs that are not deductible under this section are those that would typically be incurred by an individual holding the same property, such as homeowners association fees, insurance, and maintenance.

It is important to note that the IRS is constantly updating and refining its regulations. For example, the IRS issued Notice 2018-61, intending to clarify the effect of Sec. 67(g) on the ability of trusts and estates to deduct certain expenses.

As such, it is always advisable to refer to the latest guidelines provided by the IRS and consult with a qualified tax professional or advisor to ensure compliance with the most current regulations.

Online Money Transfers: How Long Do They Take?

You may want to see also

Explore related products

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

Fiduciary-specific expenses

The IRS provides guidance on this matter, and their regulations clarify the deductibility of administrative expenses and excess deductions upon the termination of a trust or estate. These regulations, REG-113295-18, specifically address IRC §§ 67(g) and 642(H)(2), emphasising that certain deductions are allowed because they are not considered miscellaneous itemized deductions. This is particularly relevant for tax years 2018 and beyond, where practitioners may need to revisit returns to determine if taxpayers could benefit from amendments.

Another important consideration is the treatment of beneficiaries' excess deductions. According to proposed regulations, these deductions in the hands of the beneficiary are treated the same as they were by the trust or estate. This means that a long-term capital loss for a trust, for example, remains a long-term capital loss for the beneficiary. Additionally, when it comes to fiduciary-specific expenses, fees paid and expenses reimbursed for a personal representative or fiduciary administering the trust or estate are deductible. This includes travel expenses, which can be a significant component of fiduciary responsibilities.

Furthermore, it is worth noting that certain trust arrangements may claim to reduce or eliminate federal taxes in ways that are not permitted by law. These abusive trust arrangements often promise tax benefits without any meaningful change in the taxpayer's control over their income or assets. As such, it is important to be vigilant and ensure that any deductions claimed are compliant with applicable regulations. In conclusion, understanding the deductibility of fiduciary-specific expenses is a critical aspect of trust management, and by staying informed about the latest regulations, practitioners can make informed decisions to optimise financial strategies for their clients.

Initiating a Food Bank: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The TCJA has eliminated or minimized many deductions for individuals, and trusts and estates are subject to similar deduction rules. One consequence is the elimination of a significant deduction for trusts and estates that pay trustee/executor fees.

Section 67(e) excludes fiduciary-specific expenses, such as trustees and executor's fees, from miscellaneous itemized deductions. Trusts and estates can benefit from deductions that individuals cannot if these expenses are not considered miscellaneous.

Deductible expenses for trusts and estates include tax preparation fees for most returns, appraisal fees, and certain fiduciary expenses. These expenses are deductible under Section 67(e)(1) if they are incurred in the administration of the estate or trust and would not have been incurred otherwise.

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)