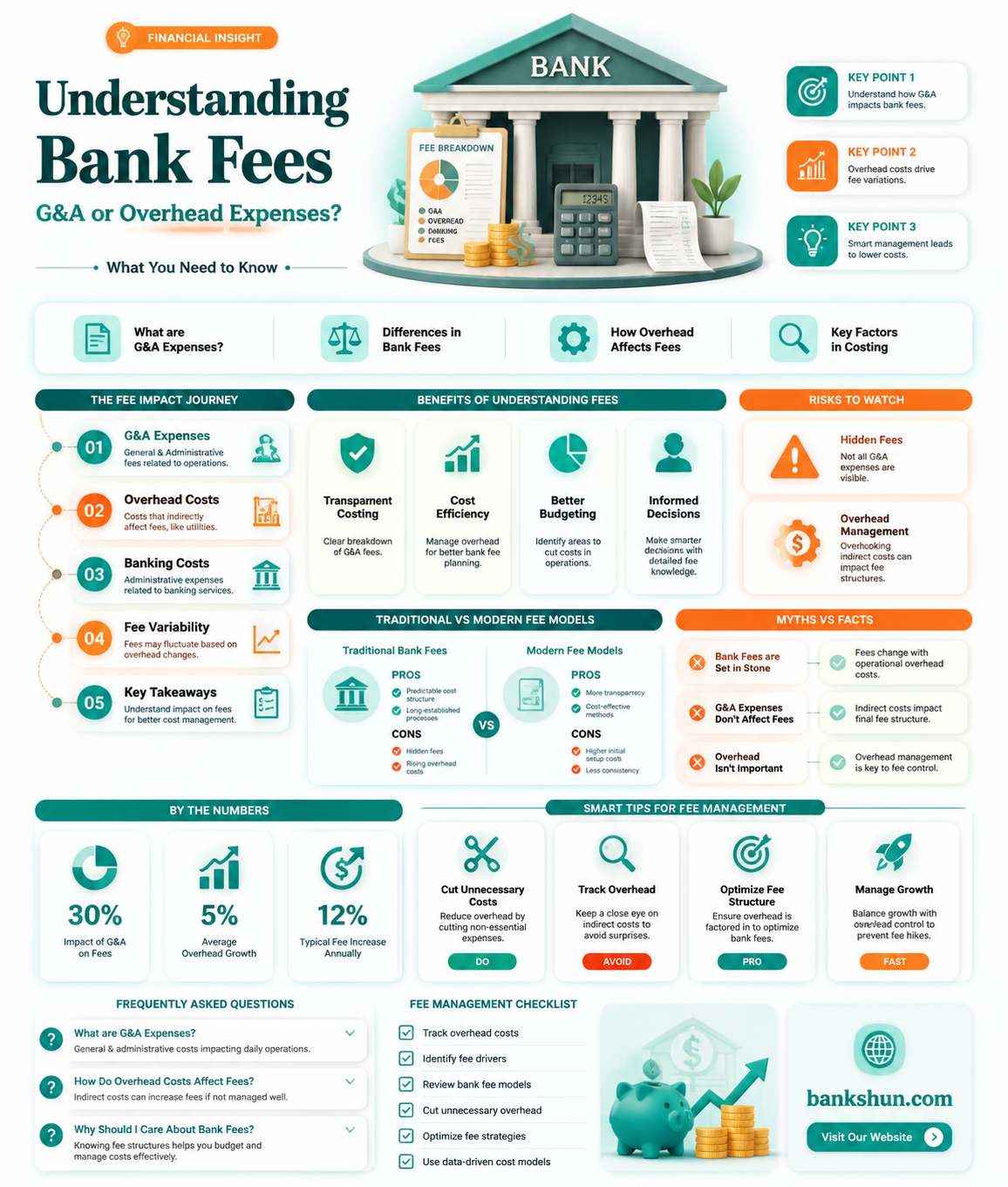

Bank fees are typically classified as G&A (General and Administrative) expenses, which are a specific category of overhead costs. Overhead and G&A expenses refer to costs that are essential for the day-to-day operations of a business but are not directly tied to the production of goods or services. G&A expenses focus on the administrative functions of the business and include costs such as accounting, legal, insurance, and bank fees. These expenses support the overall management and administration of the company rather than a particular product or service. While bank fees are generally classified as G&A, the classification of expenses can vary depending on the unique procedures and accounting practices of a company.

| Characteristics | Values |

|---|---|

| Direct costs | Directly linked to the production of goods or services |

| Indirect costs | Not directly linked to the production of goods or services but necessary for the business to function |

| Overhead costs | Indirect costs needed to run a business |

| G&A costs | A subset of overhead costs that focuses on expenses related to the general management and administration of the business |

| Overhead examples | Rent, utilities, maintenance, depreciation of assets |

| G&A examples | Bank fees, accounting expenses, insurance, office supplies, employee salaries |

| Overlap | Overhead and G&A costs can overlap |

| Difference | Depends on the company's procedures for recording expenses |

Explore related products

What You'll Learn

![]()

Bank fees are a type of G&A expense

Bank fees are a type of G&A (General and Administrative) expense. G&A expenses are a category of overhead costs that are essential for the smooth functioning of a business. They cover the administrative functions of a business, such as accounting, human resources, legal, finance, and information technology. G&A expenses are not directly tied to the production or sale of goods or services but are crucial for maintaining an efficient and well-structured organization. They enable businesses to comply with legal requirements, manage finances, and support employees.

While G&A expenses are a subset of overhead costs, not all overhead costs are G&A. Overhead costs refer to all the indirect costs needed to run a business. These include expenses such as rent, utilities, insurance, maintenance, and depreciation of assets. Overhead costs are not directly linked to the production of goods or services but are necessary for the day-to-day operations of a company.

Bank fees can be considered a G&A expense as they relate to the overall management and administration of a business rather than a specific product or service. They are typically classified as administrative expenses or financial expenses. Examples of bank fees include monthly service charges, transaction fees, ATM fees, and overdraft fees.

The distinction between overhead and G&A expenses is important, especially for government contractors who need to classify expenses correctly to avoid issues with the DCAA. While the specific classification of expenses may vary depending on the company's procedures, consistency in recording expenses is crucial. Properly categorizing expenses can impact a company's financial health, profitability, and tax obligations.

In summary, bank fees are typically classified as G&A expenses because they relate to the administrative and financial aspects of running a business rather than the direct production or sale of goods or services. G&A expenses are a subset of overhead costs, and both are essential for the overall operation and smooth functioning of an organization.

Coin Counting at US Bank: What Are Your Options?

You may want to see also

Explore related products

![]()

Overhead costs are a type of indirect cost

Overhead costs are not to be confused with direct costs, which are expenses directly linked to the production of goods or services. Direct costs are easily attributable to a specific "cost object," which may be a product, department, or project. For example, in construction, the costs of materials, labour, and equipment are considered direct costs.

General and Administrative (G&A) expenses are a category within overhead costs that focus on the administrative functions of the business. G&A expenses are not related to the production or sale of goods but are necessary for the smooth operation of the company. Examples include accounting expenses, insurance, office supplies, bank charges, and phone and internet bills.

While overhead and G&A costs can overlap, they are not the same. Overhead refers to all the indirect costs needed to run a business, while G&A is a subset of those costs, focusing on expenses related to the general management and administration of the business.

Understanding the difference between direct and indirect costs is important for pricing products or services competitively and accurately. It also helps with accounting, cost allocation, and future planning.

Are Your Bank CDs Covered by FDIC Insurance?

You may want to see also

Explore related products

![]()

Direct costs are tied to production

Direct costs are tied to the production of goods or services and are essential to the operation of a business. They are often variable costs, meaning they fluctuate with the level of production or sales. Direct costs can be tied to a specific product, service, project, or department within a company, and they are incurred for a specific purpose. These costs are typically incurred in the short term and can be easily traced to a particular cost object.

In the context of bank fees, if a bank charges a fee for a specific service, such as a wire transfer or an overdraft fee, these would be considered direct costs. These fees are directly tied to the production or delivery of a specific banking service and are incurred to generate revenue. For example, when a customer requests an international wire transfer, the bank may charge a fee to process the transaction, cover the costs of the transfer, and ensure its completion.

On the other hand, overhead costs are indirect costs that are necessary for the overall operation of a business but are not directly attributable to a specific product or service. Examples of overhead costs in a bank might include rent for the bank's branches, salaries for tellers and customer service staff, or advertising and marketing expenses to promote the bank's services. These costs are typically fixed or semi-variable and are incurred over the long term.

It's important to distinguish between direct costs and overhead costs for accurate financial reporting and decision-making. Direct costs are often passed on to the customer through the pricing of goods or services, while overhead costs are usually allocated across multiple products or services. By understanding and managing these costs effectively, businesses can improve profitability, set competitive prices, and make informed strategic decisions.

In summary, direct costs are tied to the production or delivery of specific goods or services and are essential to a company's operations. These costs are variable, short-term, and can be easily traced to a particular product, service, or department. In the context of bank fees, charges associated with specific services would fall under direct costs. By contrast, overhead costs are indirect and necessary for the overall operation of the business but are not directly tied to a specific product or service. Distinguishing between these cost types is crucial for financial management and strategic decision-making in any industry, including banking.

The Fed's Role: Bank Examinations and Their Importance

You may want to see also

Explore related products

![]()

G&A expenses are a type of overhead cost

G&A stands for "General and Administrative" expenses, and they are indeed a type of overhead cost. Overhead and G&A expenses are sometimes used interchangeably, but they are not exactly the same. Both refer to indirect costs that are essential for a business to function but are not directly tied to the production or sale of goods or services.

G&A expenses are a specific subset of overhead costs, focusing on expenses related to the general management and administration of the business. These costs support the overall operations of the company and are spread across the entire business, rather than being allocated to specific departments or projects. Examples of G&A expenses include accounting expenses, insurance, office supplies, bank charges, and phone and internet bills.

Overhead expenses, on the other hand, are indirect costs needed to run a business and can be allocated to specific projects or departments. They include expenses such as rent, utilities, and maintenance.

It's important to distinguish between overhead and G&A expenses, especially for government contractors who need to avoid issues with the Defense Contract Audit Agency (DCAA). The DCAA provides guidance on how to classify these expenses, which can impact government contracts.

In summary, G&A expenses are a type of overhead cost, but they have distinct characteristics and applications that set them apart, particularly in the context of government contracting.

Navy Federal: A Bank Worth Joining

You may want to see also

Explore related products

![]()

Overhead costs are essential for day-to-day operations

Overhead costs are essential for the day-to-day operations of a business. They are ongoing expenses that are required to run a business but are not directly involved in creating a product or service. Overhead costs are often referred to as operating expenses and include things like rent, utilities, insurance, office supplies, and administrative salaries. These costs are essential for the business to function, but they are not directly tied to the production of goods or services.

While overhead costs are necessary for the day-to-day operations of a business, they can also be a significant expense. Companies need to set prices low enough to attract customers and compete with rivals, but not so low that they cannot make a profit. Managing overheads carefully is crucial to maximize revenues and profits. If overhead costs are too high, the company may need to charge customers more to make a profit, which could lead to a loss of business.

Overhead costs are considered indirect costs because they cannot be traced directly to a cost objective, such as a contract, project, or task. These costs support the overall operations of the company and are often spread across the entire business. They are essential for the day-to-day running of the business, and regularly reviewing and analyzing these costs can help maximize efficiency and identify areas where costs can be cut.

Understanding the difference between overhead costs and other types of expenses, such as direct costs and G&A (General and Administrative) expenses, is important for effective financial management. Direct costs are directly linked to the production of goods or services, while G&A expenses are a specific part of overhead costs that focus on the administrative functions of the business. G&A expenses include things like accounting, insurance, and office supplies, while overhead costs can include a wider range of expenses such as rent, utilities, and maintenance.

In summary, overhead costs are essential for the day-to-day operations of a business as they provide critical support for the company to carry out profit-making activities. These costs are ongoing expenses that are not directly involved in creating products or services but are necessary for the business to function and compete effectively in the market. By managing overhead costs effectively and setting prices appropriately, businesses can maximize their revenues and profits.

Notary Services at Fifth Third Bank: Available or Not?

You may want to see also

Frequently asked questions

Bank fees are considered G&A (General and Administrative) expenses, a category within overhead costs. G&A expenses are not directly related to the production or sale of goods but are necessary for the smooth functioning of a company.

Examples of G&A expenses include accounting expenses, insurance, office supplies, corporate licenses, and bank charges.

Overhead expenses are considered indirect costs as they are not directly related to the production of goods or services but are essential for the day-to-day operations of a company.

Examples of overhead expenses include rent, utilities, maintenance, and depreciation of assets.

The difference between G&A and overhead depends on the procedures of your company and how expenses are recorded. G&A expenses typically focus on the administrative functions of a business, while overhead expenses can include selling and production-related expenses.

![Receipt Organizer Envelopes. 3-Way Organizers that Store Receipts, Track Expenses & Let You Find Receipts Fast. Includes an Expense Ledger + Mileage Log. 12 Pack. [6.5x9.5"] Made in USA.](https://m.media-amazon.com/images/I/71PRTws4eFL._AC_UL320_.jpg)