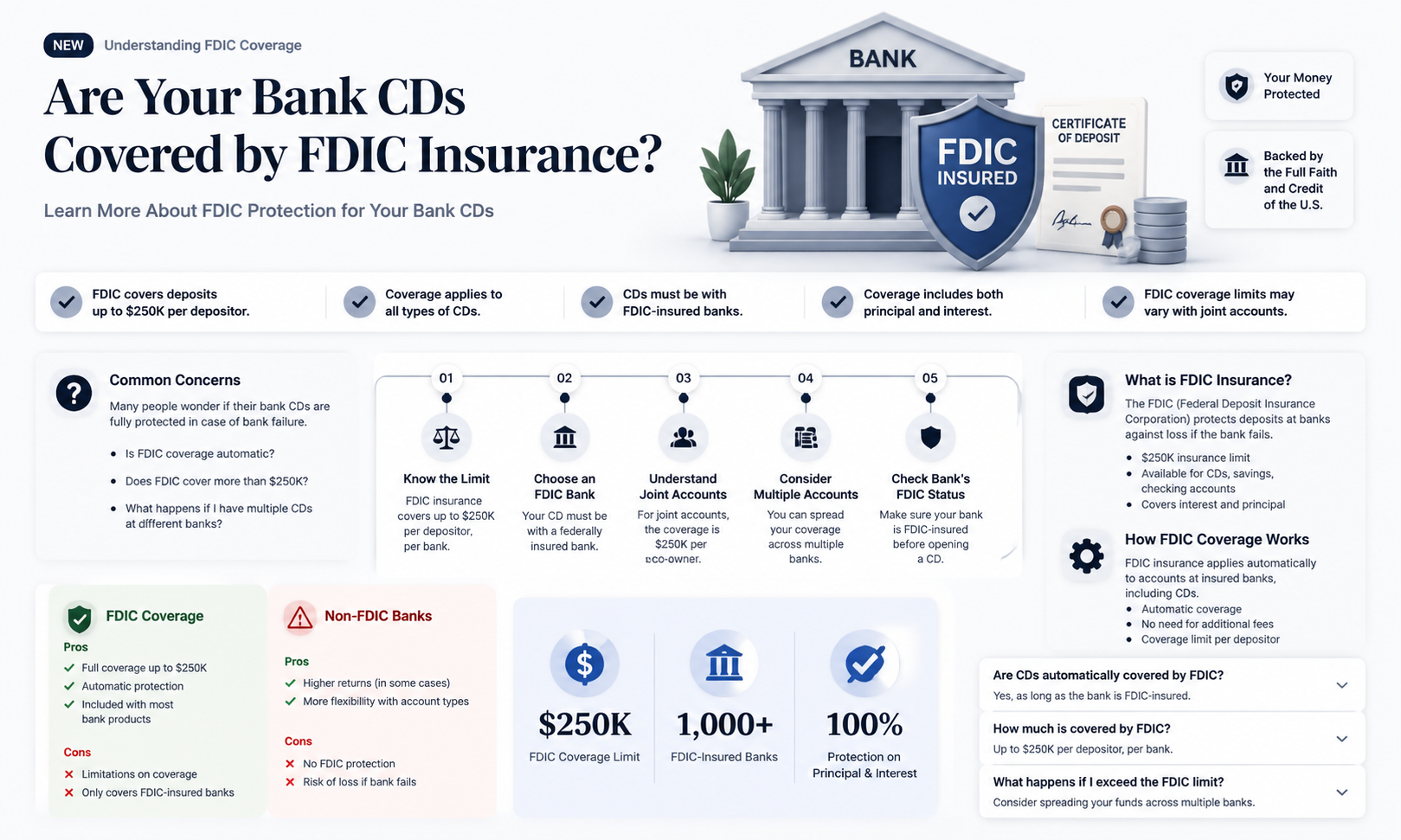

Certificates of deposit (CDs) are federally insured like other bank accounts, but not all CDs are protected by the Federal Deposit Insurance Corporation (FDIC). CDs are insured if the bank is FDIC-insured, with coverage up to $250,000 per depositor per bank. The FDIC provides deposit insurance to protect your money in the event of a bank failure. Foreign banks residing in the US may offer Yankee CD accounts without FDIC insurance, and CDs purchased through a non-bank institution such as a brokerage firm may not carry FDIC insurance.

| Characteristics | Values |

|---|---|

| Are CDs FDIC insured? | Yes, most are. |

| What is FDIC? | The Federal Deposit Insurance Corporation is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. |

| FDIC coverage limit on CDs | $250,000 per depositor per bank. |

| Coverage for joint accounts | Up to $500,000. |

| Coverage for credit unions | $250,000 per credit union per account owner. |

| Coverage for trusts | Up to $1,250,000 (up to five beneficiaries). |

| Are CDs from foreign banks insured? | No. |

| Are CDs from brokerage firms insured? | No. |

Explore related products

What You'll Learn

![]()

FDIC insurance covers up to $250,000 per depositor, per bank

The FDIC (Federal Deposit Insurance Corporation) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government.

It's important to note that FDIC insurance only applies to certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). The coverage limit of $250,000 per depositor, per bank, is for each ownership category. Deposits held in different ownership categories are separately insured, even if they are held at the same bank. For example, if you have a CD as an individual and also maintain a joint savings account with your spouse, these are considered two separate ownership categories and would each be insured up to $250,000.

Additionally, FDIC insurance only covers banks, not products offered by brokerage firms or foreign banks residing in the US. These types of accounts may be insured by other entities, such as the Securities Investor Protection Corporation (SIPC) or the National Credit Union Administration (NCUA), which offer similar coverage limits.

To ensure your accounts are FDIC-insured, look for "Member FDIC" at the bottom of a bank's website or use the FDIC's BankFind database to verify that your bank is a member.

IBT in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

CDs from non-FDIC-member banks are not insured

While most CDs are FDIC-insured, there are exceptions. CDs from non-FDIC-member banks are not insured. This includes CDs purchased through a non-bank institution, such as a brokerage firm, or CDs that involve investing money in foreign banks.

Foreign banks residing in the US may offer Yankee CD accounts, which are in US dollar denominations but do not have FDIC insurance. Similarly, some CDs from FDIC-member banks are not insured. These include CDs that exceed $250,000 and are linked to trust documents or deposits established by a third-party broker.

It is important to understand the terms and conditions of both insured and uninsured CD accounts when comparing interest rates. Uninsured CD accounts may offer higher interest rates to compensate for the lack of coverage and increased risk. Before investing in an uninsured CD account, carefully evaluate your risk tolerance and the issuing bank's stability.

FDIC deposit insurance protects bank customers in the event that an FDIC-insured bank fails. The FDIC responds by either providing each depositor with a new account at another insured bank, equal to the insured balance of their account at the failed bank, or issuing a check for the insured balance. The standard deposit insurance coverage limit is $250,000 per depositor, per FDIC-insured bank, per ownership category.

Capital One's Mascot: A Man of Many Names

You may want to see also

Explore related products

![]()

Foreign banks' Yankee CD accounts are uninsured

Foreign banks residing in the US may offer Yankee CD accounts, available in US dollar denominations but without FDIC insurance. FDIC, or Federal Deposit Insurance Corporation, is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government.

Bank customers don’t need to purchase deposit insurance; it is automatic for any deposit account opened at an FDIC-insured bank. FDIC deposit insurance only covers certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). While many CD accounts come with automatic FDIC coverage, there are exceptions. Some types of CDs don't carry deposit insurance even when held at an FDIC member bank. Uninsured CDs may include accounts where you invest money in foreign banks.

Yankee CDs are certificates of deposit issued by US branches of non-US banks. They are negotiable certificates of deposit that are issued by the United States branches of foreign banks and denominated in United States dollars. Unlike certificates of deposit issued by banks domiciled in the United States, Yankee CDs are not federally insured. In addition to the lack of FDIC insurance, you assume the risk of exchange rates moving up or down during the CD term. Uninsured CD accounts may offer higher interest rates to compensate for the lack of coverage and increased risk.

If you want the peace of mind of FDIC insurance combined with higher earnings than a traditional bank account, check out today's certificate of deposit rates and terms. If your financial institution offers both insured and uninsured CD accounts, understand all the terms and conditions when comparing interest rates between these options.

Locating Sensor 1 on Bank 1: Where is it?

You may want to see also

Explore related products

![]()

Brokered CDs are not covered by FDIC insurance

Brokered CDs are a type of certificate of deposit (CD) that investors purchase through a brokerage firm or a sales representative, instead of directly from a bank. Banks initiate brokered CDs but outsource their sale to firms that attract potential investors. Brokered CDs are generally more flexible than traditional bank CDs, allowing investors to tailor their holdings to their needs and preferences.

While brokered CDs are similar to bank CDs, there are some key differences. Firstly, brokered CDs can be transferred from one brokerage firm to another, allowing the owner to consolidate assets. This is not possible with bank CDs, as the investor would need to withdraw from the CD to move their money. Secondly, brokered CDs can be sold on the secondary market before maturity, whereas bank CDs are typically held until maturity to avoid early withdrawal penalties.

Although brokered CDs are not directly insured by the Federal Deposit Insurance Corporation (FDIC), the broker's underlying CD purchase from the bank is insured up to $250,000 per individual at each bank. This makes it crucial to buy brokered CDs from financially stable companies. Wealthy investors can spread their investments across brokered CDs from various banks, with each bank providing FDIC insurance up to $250,000.

It is important to note that brokered CDs can be riskier than traditional bank CDs if investors are not cautious. Brokered CDs may be callable, meaning the issuer can redeem them before maturity, especially if interest rates decline. Additionally, there may be a small sales fee when selling brokered CDs on the secondary market.

Sasha Banks and Snoop Dogg: Family Ties?

You may want to see also

Explore related products

![]()

FDIC insurance is automatic for deposit accounts

The FDIC insurance limit is generally $250,000 per depositor, per FDIC-insured bank, and per ownership category. This means that if you have multiple accounts with different ownership categories, such as individual and joint accounts, you can qualify for additional coverage. For example, a single-owner certificate of deposit worth $250,000 would be fully insured in the event of a bank failure. Similarly, joint accounts with two owners would be covered for up to $500,000.

It is important to note that FDIC insurance only applies to banks and not to products offered by brokerage firms, which are considered investment products. Therefore, when purchasing certificates of deposit, it is crucial to ensure that they are bought from banks that are FDIC-insured. Foreign banks operating in the US may offer Yankee CD accounts, but these are not FDIC-insured.

While FDIC insurance is automatic, there are exceptions to the coverage. Certain types of CDs, such as those purchased through a non-bank institution like a brokerage firm, may not carry FDIC insurance. Additionally, some CDs may be uninsured, and these accounts may offer higher interest rates to compensate for the lack of insurance and increased risk. It is essential to carefully review the terms and conditions of both insured and uninsured CD accounts before making a decision.

In summary, FDIC insurance provides peace of mind and protection for bank customers with deposit accounts. While it is automatic, understanding the coverage limits, ownership categories, and exceptions is crucial for making informed decisions about your financial choices.

Cross River Bank: Strategic Partnerships and Affiliates

You may want to see also

Frequently asked questions

No, only CDs from FDIC-member banks are insured. This covers up to up to $250,000 per depositor per bank, so it’s good to check if the bank is FDIC-insured.

FDIC insurance is automatic for any deposit account opened at an FDIC-insured bank. You can check if your bank is FDIC-insured by looking for "Member FDIC" at the bottom of their website or by checking the FDIC’s BankFind database.

The FDIC steps in to guarantee the insured amount in existing deposit accounts. The FDIC will first search for another bank willing to assume the insured accounts. When it isn't possible to sell or transfer the deposits, the FDIC reimburses account holders according to insurance limits.