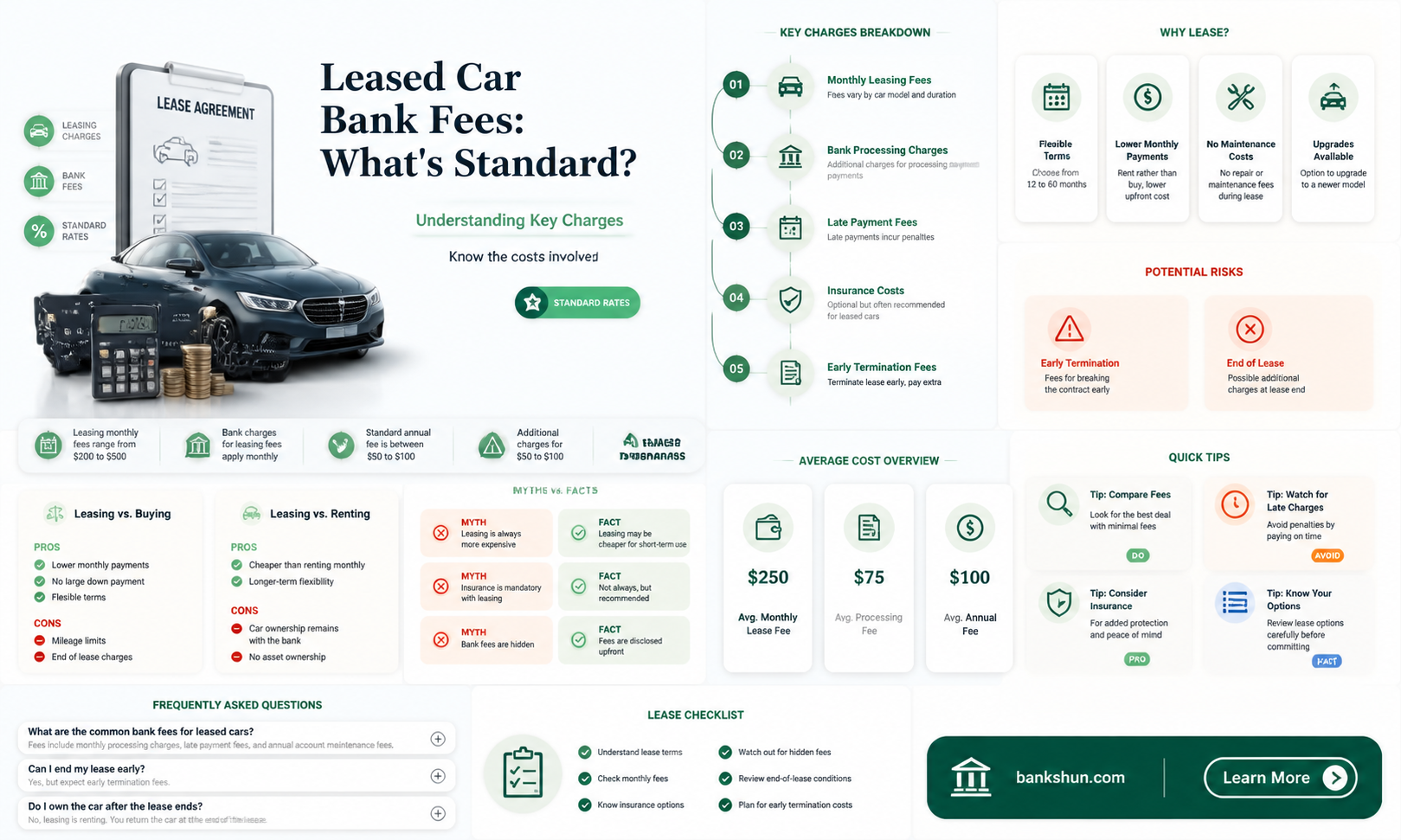

Leasing a car is an appealing alternative to purchasing one. It offers flexibility, allowing you to frequently drive a newer car, often with lower monthly payments. However, while leasing can be more affordable upfront, there are various fees and costs that can quickly diminish those savings. Understanding these fees, especially those in the fine print, is crucial to ensuring your lease remains cost-effective. Bank fees, also known as acquisition fees, are essentially administrative charges set by the lease finance company. These fees are standard on leased cars and can range from a few hundred dollars to as much as $1,000 for a higher-end luxury car.

| Characteristics | Values |

|---|---|

| Down Payment | Optional in many lease agreements, but can lower monthly payments. Usually between $1,500 and $5,000. |

| First Month's Payment | Usually due at lease signing, but some deals offer a one-month discount. |

| Sales Tax | Varies by state. In most states, paid on a portion of the vehicle, but in some states (e.g., Illinois, Texas), paid on the full amount. |

| Mileage Overage | Fees apply if the agreed-upon mileage limit is exceeded. |

| Wear and Tear | Fees charged for excessive wear or damage beyond what is considered normal. |

| Early Termination | Ending the lease early can be expensive, often requiring payment of the remaining lease balance plus additional fees. |

| Disposition Fee | Covers the cost of cleaning and reselling the vehicle after return. Typically ranges from $495 to $995. |

| Security Deposit | Required by some leasing companies, usually similar to or higher than the monthly payment. Refunded at the end of the lease, less any disposition, mileage, or damage charges. |

| Acquisition Fee (Bank Fee) | Administration fee charged by the leasing company, ranging from a few hundred dollars to $1,000 for luxury vehicles. |

| DMV Fees | Include vehicle title, registration, license plates, and other processing fees determined by the dealership. |

Explore related products

What You'll Learn

![]()

Mileage overage fees

There are several ways to reduce or eliminate mileage overage fees. Firstly, it is important to monitor your mileage carefully and try to stay within the agreed limits. If you think you might exceed your limit, you can try to negotiate a higher mileage allowance at the start of your lease or buy additional miles upfront. Some leasing companies may also waive mileage overage fees if you choose to lease or buy another vehicle from them at the end of your lease.

Another option to avoid mileage overage fees is to buy out your lease. When you buy out a lease, there may be no fees for exceeding your mileage limit, as the leasing company passes on the vehicle's lower residual value to you. Additionally, if you purchase your leased vehicle and then sell or trade it, you may come out ahead compared to paying mileage overage fees.

Finally, if you are unable to avoid mileage overage fees, it is important to contact the leasing company to negotiate a lower fee before turning in the car. While it may not be possible to avoid all charges, negotiating can help reduce the financial impact of exceeding your mileage limit.

US Banks in Florida: Where to Find Them

You may want to see also

Explore related products

![]()

Wear and tear fees

Leasing companies expect a certain level of wear and tear on their vehicles, understanding that minor scratches, dings, and mechanical wear will naturally occur during the lease period. However, excessive wear and tear can result in additional charges when the vehicle is returned at the end of the lease. These charges are intended to cover the cost of repairs needed to restore the vehicle to an acceptable condition for the next lessee.

To avoid unexpected wear and tear fees, it is essential to maintain the vehicle properly during the lease. This includes regular servicing, timely repairs, and proactive measures to protect the interior and exterior of the vehicle. Some leasing companies provide specific guidelines on acceptable levels of wear and tear, and it is important to review these terms before signing the lease agreement.

In some cases, lessees may find the wear and tear charges excessive or unfairly assessed. To address this, it is recommended to demand a detailed written estimate of the damages and their associated costs. Lessees can then obtain independent repair estimates from body shops or other dealers to compare with the leasing company's charges. If there is a significant discrepancy, lessees can dispute the excessive wear and tear fees and, if necessary, involve legal counsel.

Additionally, lessees can consider purchasing wear and tear protection for their leased vehicle. This protection plan covers certain damages that exceed normal wear and tear, potentially saving lessees from incurring high fees at the end of the lease. Proper maintenance and a good leasing history can also make it easier to lease another vehicle in the future.

Ally Bank: A History of Innovation and Customer Focus

You may want to see also

Explore related products

![]()

Termination fees

While leasing a car can be more affordable upfront, hidden fees can quickly diminish those savings. Understanding these fees is crucial to ensuring your lease is as cost-effective as possible.

In addition to termination fees, there are other fees to be aware of when ending your car lease. These include mileage overage fees, lease disposition fees, excessive wear and tear fees, and lemon law fees. Mileage overage fees are charged when you exceed the mileage limit set by your lease, which is typically 12,000 miles per year. Lease disposition fees are charged by dealerships when a leased vehicle is returned to cover the costs of reconditioning and cleaning the car. Excessive wear and tear fees are charged when the car is returned with more damage than considered normal. Lastly, lemon law fees are charged by some dealerships for returning a leased vehicle that has experienced significant mechanical issues during the lease term.

It's important to scrutinize every part of a lease agreement before signing to avoid unexpected charges. While some fees may be unavoidable, being aware of potential charges at the end of the lease can help you make informed decisions and avoid unnecessary expenses.

Federal Bank: Who Owns the Renowned Indian Bank?

You may want to see also

Explore related products

![]()

Disposition fees

A disposition fee is an end-of-lease fee charged to consumers to cover the costs of returning a leased vehicle. It is meant to compensate the dealership for the costs associated with reconditioning, cleaning, and prepping the car for resale. This fee is included in the original lease contract, but many customers do not notice it as they are more focused on monthly payments and down payments.

The average lease disposition fee is between $300 and $400, but this amount can vary based on your location, the make and model of the car, and the extent of wear and tear. In some cases, the fee can be as high as $395. While this fee is often unavoidable, there are a few ways to potentially avoid or reduce it.

Firstly, some leasing companies may waive the fee if you choose to lease another vehicle from them. This is a common loyalty program incentive. Secondly, you can try to negotiate the fee before signing the lease. Understanding leasing terminology and being clear about mileage limitations, overage fees, and other fees can help you negotiate a better deal. Thirdly, you can consider buying the car at the end of the lease, which will save the dealership the trouble of cleaning and reconditioning the vehicle for resale.

It is important to scrutinize every part of a lease before signing, as disposition fees are included in the contract and are legally binding once signed. Not paying disposition fees can negatively impact your credit score as it involves unpaid debt, making it more difficult to get favourable auto loan deals in the future.

POD in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

Security deposits

When leasing a car, you may be required to pay a security deposit. This is different from a down payment, which is usually not recommended for car leases. A security deposit can act as a down payment, but you can cancel your order for a new car up until a certain point and you may not get your security deposit back. However, you will get your security deposit back at the end of the lease or if you total the car and the insurance pays it off.

A security deposit can help bring down your interest rate. For example, a $3000 security deposit can bring down your interest rate by 1%. This is because, in most leasing contracts, if a security deposit is required, it will be equal to one month's payment, rounded up to the nearest $50. This can help save money on interest, especially if you make multiple security deposits.

It is important to note that some lenders that allow multiple deposits will limit the number of security deposits you can make. Additionally, spending more money out of pocket to reduce an already low-interest rate might not be the best option for you. For example, you may be able to get a better deal by paying for the whole lease upfront, which is often called a one-pay or single-pay lease. This can help you save money on interest costs and may be a good option if you are new to the country and do not have a credit history.

In addition to security deposits, there are other fees to consider when leasing a car. These include mileage overage, excessive wear and tear, early termination, disposition fees, and various taxes and registration fees. Being aware of these potential charges and understanding the leasing terms and costs can help you avoid unnecessary expenses.

Wealthiest Italian Bankers: Who Topped the List?

You may want to see also

Frequently asked questions

Bank fees, also known as acquisition fees, are administration fees charged by a car leasing company. They are essentially unavoidable and are usually in the range of $495 to $995, with averages in the $595-$795 range.

Yes, bank fees are standard on a leased car. However, they can differ depending on the car company and the financial institution.

There are various other fees associated with leasing a car, including a security deposit, mileage overage, disposition fee, and excessive wear and tear.

While bank fees are usually unavoidable, you may be able to negotiate them down or lease the car through an external bank to avoid paying a high fee.

The bank fee for a leased car is typically due at the end of the lease. However, it is important to carefully read the lease agreement to understand when and how much you need to pay.