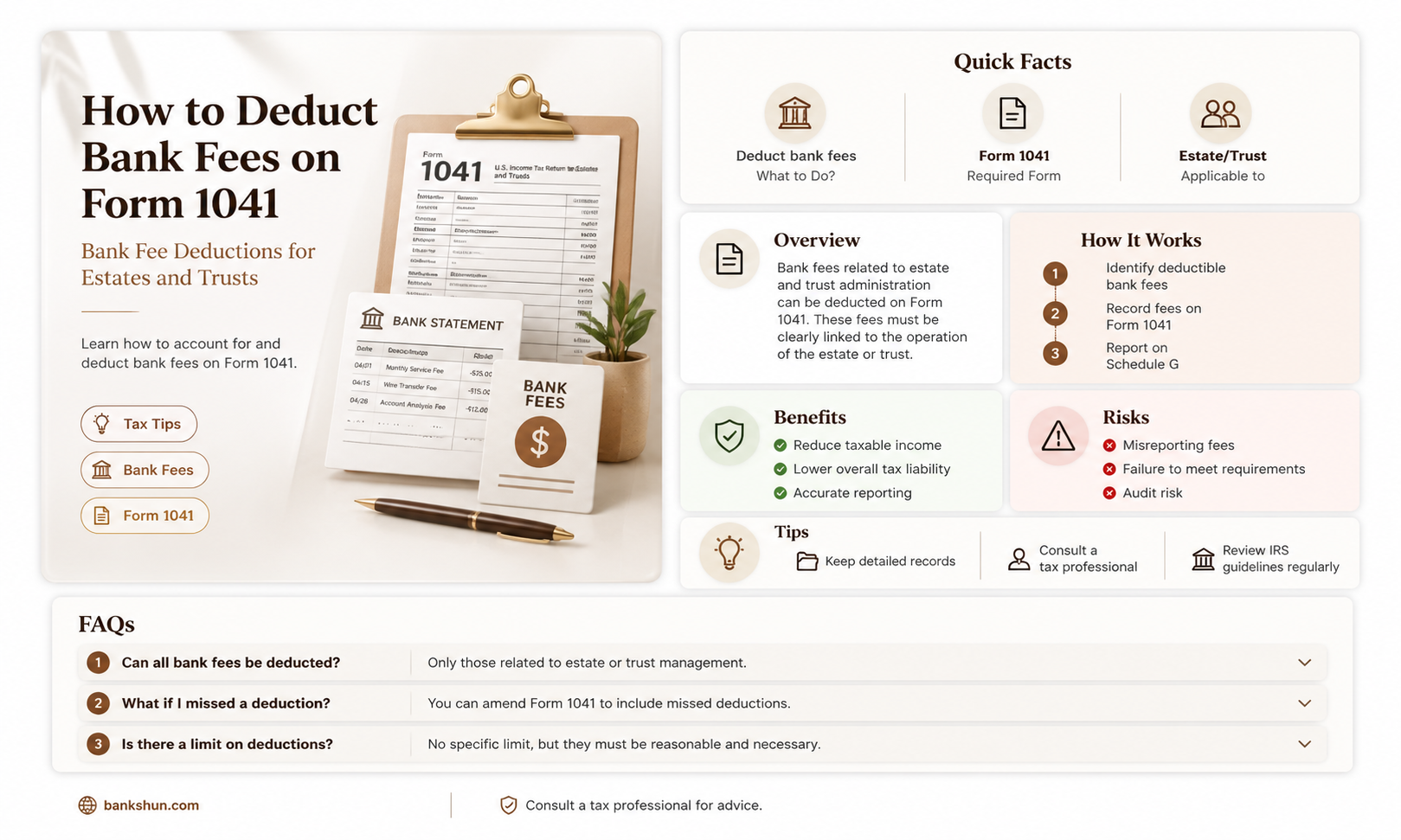

Form 1041 is used to report the income, deductions, gains, and losses of a decedent's estate, trust, or bankruptcy estate. This form allows for various expenses and deductions to be charged against taxable income. So, are bank fees deductible on Form 1041? The answer is yes, but with some conditions and limitations. Bank fees, like other administrative expenses, can be deducted if they are considered ordinary and necessary expenses for the administration of the trust or estate. This includes fees paid to financial advisors and investment advisors, which may be classified as fiduciary fees. These deductions help reduce the taxable income of trusts and estates. However, it's important to consult a qualified tax professional for specific scenarios and to ensure proper documentation and substantiation of these deductions.

| Characteristics | Values |

|---|---|

| Form 1041 Used For | Reporting income, deductions, gains, and losses of an estate or trust |

| Who Files Form 1041 | Fiduciary of a domestic decedent's estate, trust, or bankruptcy estate |

| Deductible Expenses | Ordinary and necessary expenses, interest, charitable contributions, administrative costs, investment expenses, rental property expenses, property taxes, property management fees, repairs and maintenance, fiduciary fees, and executor fees |

| Non-Deductible Expenses | Items of income, deduction, and credit for an electing trust that terminates during the election period |

Explore related products

What You'll Learn

![]()

Professional fees

Form 1041 is used by the fiduciary of a domestic decedent's estate, trust, or bankruptcy estate to report income, deductions, gains, and losses.

Other ordinary and necessary expenses that are deductible include office expenses, such as rent, utilities, and office supplies, as well as travel expenses like transportation, lodging, and meals.

Interest and charitable contributions are also deductible on Form 1041. Interest paid on loans used to acquire property or to carry on a trade or business is generally deductible, and charitable contributions made by the trust or estate are also deductible, subject to certain limitations.

In addition, distributions made to beneficiaries are deductible, provided they are made in accordance with the terms of the trust or estate's governing documents and applicable law. Fees for the services of trustees and executors are also deductible, but these charges must be fair and required for the services rendered.

It is important to keep accurate records of the fees paid and the services provided to properly substantiate any deductions claimed on Form 1041.

Wells Fargo Notary Services: Availability and Requirements

You may want to see also

Explore related products

![]()

Administrative costs

Examples of administrative expenses include fees paid to attorneys and accountants for estate tax return preparation, costs associated with the sale of property, and fees paid to financial advisors. Investment management costs are also considered administrative expenses, including fees paid to investment advisors, custodial fees, and costs associated with investment research.

Other examples of administrative costs include office expenses such as rent, utilities, and office supplies, as well as travel expenses for transportation, lodging, and meals. Depreciation, which is the cost of a capital asset over its useful life, is also considered an administrative expense.

It is important to note that administrative costs are different from other deductible expenses on Form 1041, such as ordinary and necessary expenses, interest, charitable contributions, and distributions made to beneficiaries. These expenses are subject to specific rules and limitations outlined by the Internal Revenue Service (IRS).

To ensure compliance and optimize tax benefits, it is recommended to consult with a qualified tax professional who can provide guidance on the deductibility of specific administrative costs and other expenses related to Form 1041.

Wells Fargo: A Comprehensive Banking Experience

You may want to see also

Explore related products

![]()

Investment expenses

Other deductible investment expenses include ordinary and necessary expenses, which are expenses that are common and accepted in the trust or estate's trade or business, as well as expenses that are helpful and appropriate to the business. Examples of ordinary and necessary expenses include professional fees, such as fees paid to lawyers, accountants, and investment advisors; office expenses, such as rent, utilities, and office supplies; travel expenses, such as transportation, lodging, and meals; and depreciation, which is the cost of a capital asset over its useful life.

Interest and charitable contributions are also deductible expenses on Form 1041. Interest paid on loans used to acquire property or to carry on a trade or business is generally deductible. Charitable contributions made by the trust or estate are also deductible, subject to certain limitations.

It is important to carefully review and document all deductible expenses on Form 1041 to reduce the taxable income of trusts and estates and lower their tax liability. If there are questions about the deductibility of specific expenses, it is recommended to consult a qualified tax professional.

PNC Bank: A Historical Overview of Its Evolution

You may want to see also

Explore related products

![]()

Charitable contributions

Grantor trusts do not claim charitable deductions on Form 1041. Instead, the grantor deducts these contributions on their individual tax return. Estates and trusts may also face limits based on the alternative minimum tax (AMT). Charitable contributions made by the trust or estate are deductible up to 50% of the trust or estate's adjusted gross income.

It is important to note that Form 1041 is used by the Internal Revenue Service (IRS) to report taxable income from estates and trusts. By understanding the different deductions available, including charitable donations, taxable income can be reduced.

Finding Someone's Bank: Strategies and Solutions

You may want to see also

Explore related products

![]()

Executor fees

Form 1041 is used for reporting asset-generated income that an estate or trust earns from the time of an individual's death until assets are distributed to beneficiaries and/or owners. The fiduciary of a domestic decedent's estate, trust, or bankruptcy estate uses Form 1041 to report income, deductions, gains, and losses, among other things.

It is important to note that the fees paid to a fiduciary are considered taxable income to the recipient. The fiduciary must report the fees on their own tax return and pay any applicable taxes on the income. Additionally, accurate records of the fees paid and the services provided are essential to properly substantiate the deduction on Form 1041.

Form 1041 allows for a variety of expenses and deductions to be charged against taxable income. These can include charitable deductions, professional fees (such as those paid to attorneys, accountants, and tax preparers), and money transferred to beneficiaries.

In addition to executor fees, administrative costs incurred in connection with the administration of the trust or estate may also be deductible on Form 1041. Examples of such administrative expenses include fees paid to attorneys and accountants for estate tax return preparation, costs associated with the sale of property, and fees paid to financial advisors.

US Bank: 24/7 Customer Service Availability

You may want to see also

Frequently asked questions

Form 1041 is used for reporting asset-generated income that an estate or trust earns from the time of an individual's death until assets are distributed to beneficiaries or owners.

Bank fees that are deductible on Form 1041 include professional fees (e.g. lawyers, accountants, investment advisors), administrative costs (e.g. estate tax return preparation, property sale costs), and investment expenses (e.g. investment advisor fees, custodial fees). Additionally, fiduciary fees, which are the amounts charged by executors, trustees, or personal representatives for their services, are also deductible.

Yes, it is important to note that the fees must be considered ordinary and necessary expenses that are common, accepted, and appropriate for the trust or estate's business. Furthermore, distributions to beneficiaries must adhere to the terms of the trust or estate's governing documents and applicable laws to qualify as deductible expenses.

To calculate the deductible fiduciary fees, you must first subtract the total income from lines 1 through 8 of Form 1041 from the total taxable income. Then, multiply the result by the total fiduciary fees. Finally, subtract the balance from the total tax-exempt income to arrive at the adjusted tax-exempt income, which is entered on Schedule B, line 2.