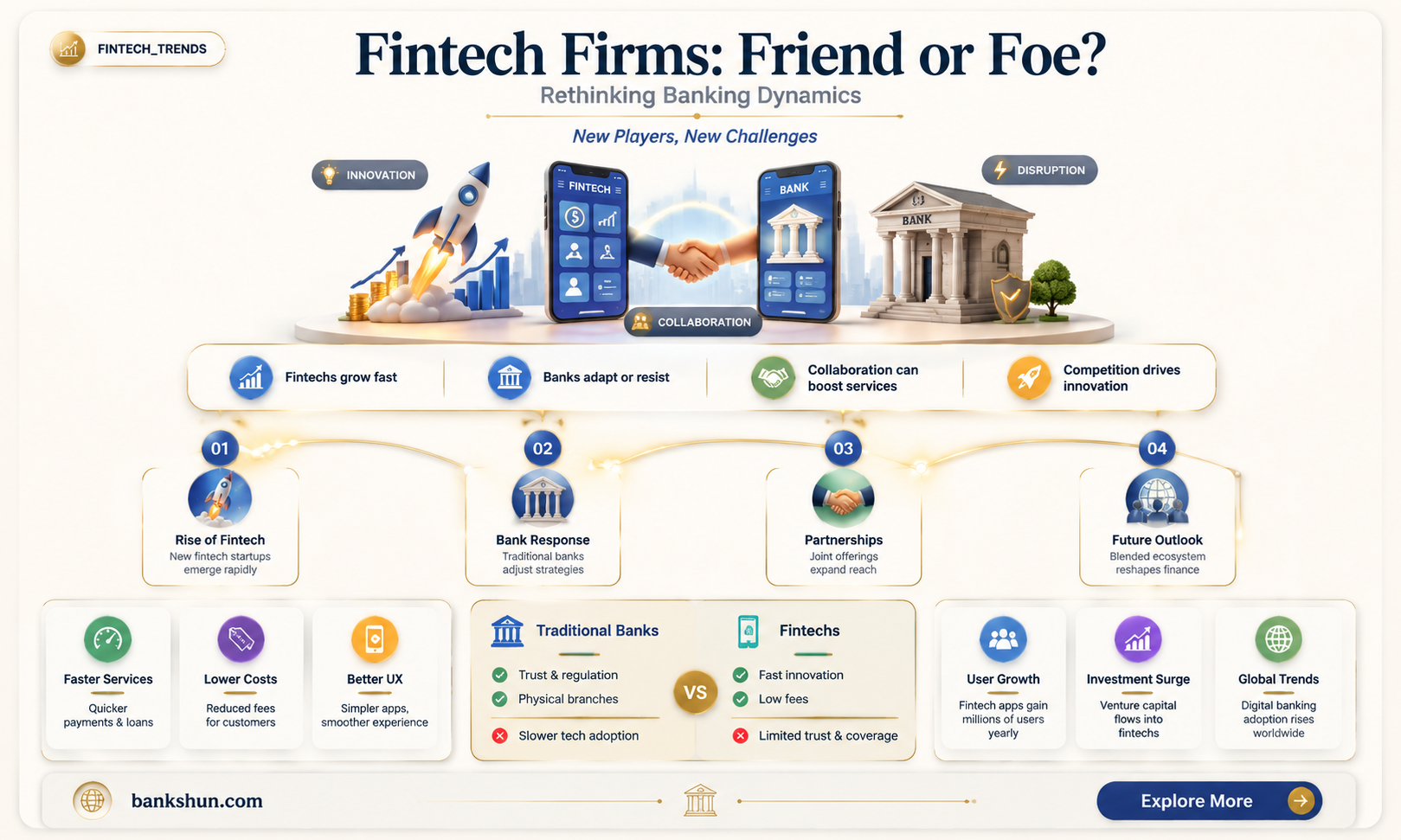

Fintech companies are increasingly encroaching on the turf of traditional banks, but are they a threat? Fintech services have made inroads into online lending and payment services, leveraging digital innovations such as peer-to-peer lending, crowdfunding, cryptocurrencies, blockchain, and machine learning. While the fintech sector's growth has been exponential, it remains small compared to the banking sector, and faces regulatory and funding challenges. However, the potential for disruption is real, and banks are aware that technology could enable new entrants to the industry and threaten their market share.

| Characteristics | Values |

|---|---|

| Fintech market size | Global fintech activity reached around $210 billion in 2021, while the size of global financial services in the same year was $23,319.52 billion |

| Fintech companies' threat to banks | Fintech companies pose a potential threat to the stability of the financial sector by eroding profits and raising operating costs |

| Fintech's competitive advantage | Fintech companies are especially present in banks' traditional markets, such as online peer-to-peer lending platforms that match borrowers with investors |

| Regulatory environment | Fintech companies often face more regulatory obstacles than banks, and the lack of a clear definition of "fintech" may pose challenges for risk assessment and compliance |

| Impact on banks' market share | The growth of fintech firms in payment services may threaten banks' market share in this business line |

| Venture capital funding | Fintech firms rely on outside capital, and a decline in venture capital funding in 2022 hurt their operations |

Explore related products

$16.95 $16.95

$14.99 $29.95

What You'll Learn

- Fintech companies capture market share from traditional banks, threatening their stability

- Fintech's growth in payment services threatens banks' market share in this sector

- Fintech companies face more regulatory obstacles than banks

- Fintech's technological advances disrupt the financial services sector

- Fintech companies' access to venture capital funding is limited compared to traditional banks

![]()

Fintech companies capture market share from traditional banks, threatening their stability

Fintech companies are increasingly capturing market share from traditional banks, causing a potential threat to their stability. Fintech services have made significant inroads into online lending and payment services, with peer-to-peer lending platforms at the forefront of this revolution. These platforms automate the entire lending process, allowing borrowers to access loans from investors without interacting with traditional finance providers like banks. While the fintech sector remains relatively small compared to the banking industry, its exponential growth and encroachment into banks' activities cannot be ignored.

The emergence of fintech companies in banks' traditional markets has led to increased competition for funding loans, which can destabilize the banking sector. As fintech firms attract more customers, banks may face higher operating costs and eroded profits. Additionally, the rise of decentralized finance (DeFi), embedded finance, and new entrants, coupled with changing customer expectations and regulatory shifts, further intensifies the competition.

Fintech companies often face more regulatory obstacles than banks, and the current macroeconomic environment poses additional challenges. However, the sector's potential to increase financial inclusion and lower costs for consumers cannot be understated. While some fintech firms may disappear due to weaker business models, a handful will survive and significantly impact the industry.

To maintain their stability, banks must recognize the disruptive potential of technology and adapt their business models. Traditional banks have the advantage of established brands and customer relationships, as well as access to stable deposit funding. By leveraging their strengths and embracing technological advancements, banks can stay competitive in the face of the growing fintech sector.

In conclusion, while fintech companies are capturing market share and posing a potential threat to traditional banks, the banking sector can safeguard its stability by staying agile and responsive to the changing landscape. The competition between fintech firms and banks may ultimately benefit consumers by driving innovation, increasing financial inclusion, and providing more diverse financial service options.

Monitoring Large Withdrawals: Why Banks Report Over $10,000

You may want to see also

Explore related products

$37.99 $42.39

![]()

Fintech's growth in payment services threatens banks' market share in this sector

Fintech companies are increasingly encroaching on banks' activities, particularly in the payment services sector. This has the potential to threaten banks' market share in this line of business. While the fintech sector remains small compared to the banking sector, its exponential growth and digital innovations in financial services pose a competitive threat to traditional banks.

Fintech firms have made significant inroads into online lending and payment services, leveraging digital algorithms to automate the lending process. This automation eliminates the need for borrowers to interact with loan officers or visit bank branches, enhancing convenience and accessibility. However, commercial banks have also embraced digital technologies, albeit with a more hybrid approach that combines offline processes and staff involvement in credit decisions.

The growth of fintech in payment services is particularly notable. Fintech companies are capturing market share in this sector by offering greater competition and innovative products. The need for increased competition in banking has been recognized, especially in markets dominated by traditional banks with limited offerings. Fintech solutions in payment services include digital identification, mobile applications, cloud computing, and big data analytics, enhancing efficiency and customer experiences.

While regulatory obstacles and macroeconomic conditions may challenge fintech companies, they still have the potential to increase financial inclusion and lower costs for consumers. The lack of a clear definition of "fintech" and inconsistent regulatory standards across jurisdictions can create risks and impact the stability of the financial sector. Nevertheless, fintech's growth in payment services specifically threatens banks' market share in this sector, forcing banks to adapt and innovate to maintain their competitive edge.

To conclude, fintech's expansion in payment services is disrupting banks' traditional dominance. Banks need to embrace digital transformation and enhance their offerings to retain customers and stay competitive in the evolving financial landscape.

Bank Shots: Halo 3's Uncommon Skill

You may want to see also

Explore related products

$12.32 $19.99

![]()

Fintech companies face more regulatory obstacles than banks

Fintech companies have emerged as significant players in the financial services industry, particularly in areas such as online lending and payment services. While they have captured market share from traditional banks, the fintech sector remains relatively small compared to the established banking sector. However, fintech firms often face more regulatory hurdles than banks, which can impact their operations and growth prospects.

One of the key challenges for fintech companies is the varying regulatory landscapes in different jurisdictions. For example, in Australia, regulators updated the licensing framework for new depository institutions in 2021 and are considering enhanced oversight of consumer credit. Such regulatory shifts can create obstacles for fintech firms looking to expand their reach and serve customers in multiple markets.

The lack of a clear definition of "fintech" also poses challenges in regulating these companies. Without a well-defined scope, regulators struggle to implement effective oversight and mitigate potential risks. This ambiguity has led to concerns about a potential bubble in the fintech industry, similar to the "dotcom" bubble of the late 1990s, where investment was driven by faith in technology rather than tangible results.

To address these concerns, some regulators have proposed regulatory sandboxes, which provide a controlled environment for testing fintech solutions and evaluating associated risks. For instance, the Bank of Lithuania is introducing a sandbox to facilitate the exploration of fintech innovations while maintaining a focus on risk management and consumer protection.

While fintech companies face regulatory obstacles, they also benefit from the support of venture capital firms, particularly in regions like Eastern Europe, where traditional funding sources have been limited. This influx of investment enables fintech firms to develop innovative products and services, enhancing competition in the banking industry and driving the adoption of new technologies.

Inheritance in Ireland: Do Banks Know?

You may want to see also

Explore related products

![]()

Fintech's technological advances disrupt the financial services sector

Fintech companies are increasingly disrupting the financial services sector with their technological innovations. These digital innovators are making inroads into banks' traditional markets, particularly in online lending and payment services. Peer-to-peer lending platforms, for instance, match borrowers with investors online, eliminating the need for traditional finance providers. Fintech companies are also making strides in areas such as crowdfunding, blockchain, digital wealth advisory, trading platforms, and mobile payment systems. This has the potential to shake up the banking industry by eroding profits and raising operating costs.

While the fintech sector has experienced exponential growth over the past decade, it remains small compared to the established banking sector. Global fintech activity reached around $210 billion in 2021, while the size of global financial services was $23,319.52 billion in the same year. However, the growth of fintech firms in payment services and the competition they pose to banks cannot be understated.

Fintech companies often face more regulatory obstacles than banks, and the current macroeconomic environment, including rising interest rates, may pose challenges to their operations. For example, in 2022, global fintech funding fell by 46% due to a decline in venture capital funding. Regulatory sandboxes, such as the one introduced by the Bank of Lithuania, aim to provide a safe environment for exploring fintech solutions while managing risks.

Despite these challenges, fintech continues to attract investment from venture capital firms and has the potential to increase financial inclusion and lower costs for consumers. The use of technology in finance has opened up competition and provided consumers with more innovative products and services. As such, fintech's technological advances are disrupting the financial services sector, forcing traditional banks to adapt and innovate to maintain their market share.

Which Bank Has Branches in Every US State?

You may want to see also

Explore related products

![]()

Fintech companies' access to venture capital funding is limited compared to traditional banks

Fintech companies have been making inroads into the financial services sector, particularly in the areas of lending and payment services. Their emergence in banks' traditional markets has led to concerns about their potential to disrupt the banking sector. However, it is important to note that the fintech sector remains relatively small compared to the established banking industry. While fintech firms have experienced remarkable growth, their access to venture capital funding is limited compared to traditional banks.

Fintech companies, particularly those in the early stages, often rely on external capital to fund their operations and acquire clients. In 2022, a decline in venture capital funding impacted fintech firms, as global fintech funding fell by 46% from 2021. On the other hand, traditional banks have benefited from their established brands and customer relationships, allowing them to access stable deposit funding. This funding advantage has given banks an edge over many fintech companies.

The difference in funding sources between fintech companies and traditional banks can be attributed to several factors. Firstly, banks have long-standing relationships with customers, which facilitates access to deposits and other forms of funding. Secondly, banks have a stronger position in the market due to their established brands and trustworthiness in the eyes of investors and customers. Fintech firms, especially those with weaker business models, may struggle to attract the same level of investment due to the higher perceived risk.

Additionally, regulatory requirements and licensing frameworks can vary between fintech companies and traditional banks. Fintech firms may face more regulatory obstacles and are subject to changing requirements in different jurisdictions. For example, in Australia, regulators updated the licensing framework for new depository institutions, creating additional challenges for fintech companies operating in that market. These regulatory factors can influence the availability of funding for fintech firms.

While fintech companies face limitations in venture capital funding compared to traditional banks, it is worth noting that the fintech sector is dynamic and evolving. The use of technology and innovation provides fintech firms with opportunities to attract investment and disrupt the banking sector. For example, the development of private blockchains and the exploration of venture capital investment in Lithuania showcase the potential for fintech to access alternative funding sources and challenge traditional banking models.

Withdrawing Money from Your Bank: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Fintech companies are a potential threat to traditional banks as they capture market share and erode profits. However, the sector remains small compared to the banking sector and does not pose an existential threat.

Fintech companies threaten banks by offering digital financial services such as peer-to-peer lending, crowdfunding, and payment services, which can destabilise the banking sector by increasing the cost of deposits.

The impact of fintech on the banking sector is mixed. While fintech can increase competition and lower costs for consumers, it can also lead to increased operating costs and regulatory challenges for banks.

Fintech companies often face more regulatory obstacles than banks and may struggle with accessing funding, especially during challenging macroeconomic conditions.

The future of fintech and banking is likely to involve increased competition and disruption. Fintech companies will continue to innovate and transform the financial services sector, while banks will need to adapt and embrace technology to remain competitive.