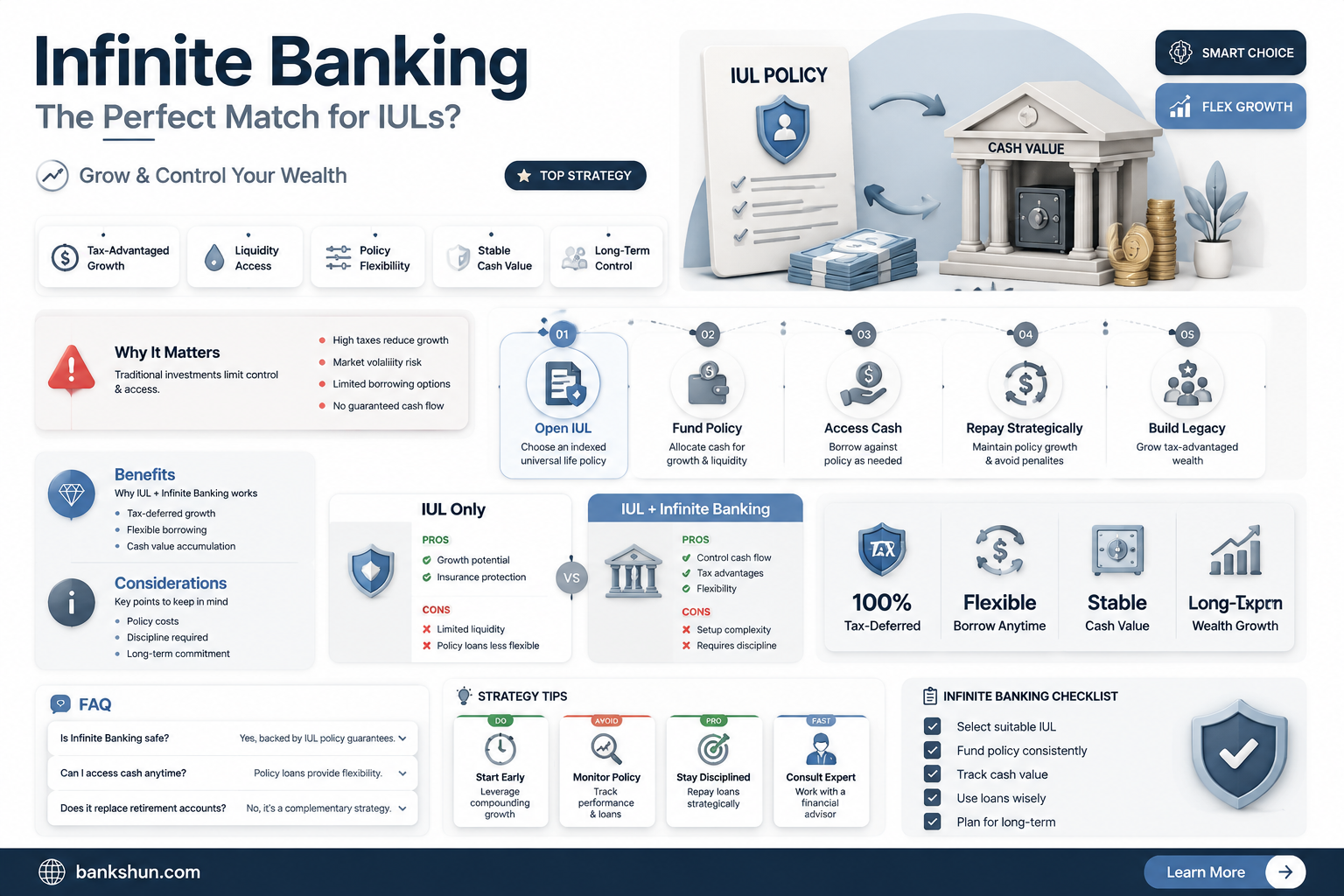

The Infinite Banking Concept (IBC) is a transformative approach to personal finance that leverages the benefits of whole life insurance policies. It involves using life insurance policies as personal banking systems, allowing individuals to access funds for various needs without relying on traditional banking. Indexed Universal Life (IUL) insurance policies are often considered for IBC due to their flexibility and growth potential. IUL policies offer the ability to link cash value to stock market indices, providing a balance of growth potential and risk management. However, there are conflicting opinions on the suitability of IUL for IBC, with some arguing that Whole Life Insurance is preferable due to its guaranteed growth and greater access to early cash value. Ultimately, the decision between IUL and Whole Life Insurance for IBC depends on individual needs, time horizons, and comfort with risk.

| Characteristics | Values |

|---|---|

| Flexibility | IUL offers the ultimate flexibility as no premium is ever due as long as there is sufficient equity within the policy |

| Tax advantages | Policy loans from a cash value life policy are typically tax-free, providing an attractive source of immediate cash funds with easy access and no banking fees |

| Risk | IUL policies are considered riskier than Whole Life policies as they do not have the same guarantees and there is a lack of access to cash value in the beginning years |

| Returns | IUL policies can offer higher returns than Whole Life policies, with the potential to earn 9%-11.25% each year tracking the S&P 500 index |

| Arbitrage | IUL policies can offer positive arbitrage, where the cash value borrowed against can earn more than the loan interest |

| Long-term planning | IUL policies may be more suitable for those with a longer time horizon, whereas Whole Life may be preferable for those seeking immediate access to cash value |

Explore related products

What You'll Learn

![]()

Infinite Banking offers financial autonomy and security

The Infinite Banking Concept (IBC) is a transformative approach to personal finance and wealth management. It revolves around using permanent life insurance policies as financial instruments to accumulate wealth and access capital. This concept was created by R. Nelson Nash during the 1980s and involves becoming your own banker by using index universal life policies or whole-of-life dividend-paying policies to access loans.

The appeal of Infinite Banking with IUL lies in the potential for positive arbitrage, where the cash value borrowed against can earn more than the loan interest. Additionally, IUL policies offer the flexibility of no required annual premiums as long as there is sufficient equity within the policy. IUL policies also have the advantage of being linked to market indices, providing the opportunity for higher returns compared to traditional whole life insurance policies.

However, it is important to note that IUL policies may not be suitable for everyone. They are considered riskier due to the surrender period, which restricts access to cash value in the initial years. Additionally, IUL policies do not offer the same guarantees as whole life insurance, and proper management is required to maximize their benefits.

Seeking guidance from qualified financial advisors and understanding the intricacies of life insurance products are crucial steps before implementing Infinite Banking with IUL.

Central Banks' Stock Market Intervention: What's the Plan?

You may want to see also

Explore related products

$9.99 $15.99

![]()

IUL offers flexibility and higher returns

Indexed Universal Life (IUL) insurance policies are dynamic financial tools designed to build wealth, offer flexibility, and serve as personal banking systems. IUL offers flexibility in terms of premium payments, allowing clients to skip payments for 2-3 years if they fund their IUL to the maximum in the first year. This flexibility makes it a more attractive option for those who are reluctant to commit to the rigid annual premium payments associated with Whole Life insurance policies.

The cash value component of IUL policies is a key advantage, providing individuals with access to funds for various needs without relying solely on traditional banking and retirement saving methods. This cash value can be leveraged to borrow against the policy, granting individuals access to capital from their policy, often tax-free, to invest in assets, pay off high-interest debt, or fund major purchases.

IUL policies offer growth potential by linking the cash value to the performance of market indices, such as the S&P 500 index, which has historically delivered returns ranging from 5% to 11.25%. This potential for higher returns compared to Whole Life insurance makes IUL a powerful tool for accumulating wealth and pursuing financial goals.

The combination of flexibility and higher returns makes IUL a compelling option for individuals seeking to maximize their financial autonomy and growth within the framework of infinite banking. However, it is important to carefully design and manage IUL policies to optimize their benefits and mitigate potential risks.

Good Friday: Are Banks Open or Closed?

You may want to see also

Explore related products

![]()

Whole Life Insurance offers guaranteed growth and peace of mind

Whole life insurance is a permanent life insurance plan that provides coverage for your entire life. It offers guaranteed growth and peace of mind through its death benefit and cash value accumulation features.

The death benefit in a whole life insurance plan is a guaranteed payout to your loved ones when you pass away. This benefit is certain, regardless of the timeframe, providing financial protection and peace of mind for your dependents.

Whole life insurance also accumulates cash value over time, which is guaranteed to grow year over year. This cash value can be used for anything, such as unexpected expenses, college tuition, or supplementing retirement income. The cash value grows tax-deferred, providing additional financial flexibility and peace of mind.

The premiums for whole life insurance are typically fixed and do not change over time. This consistency in expenses allows for better financial planning and peace of mind, knowing that your coverage is secure.

While whole life insurance offers guaranteed growth and peace of mind, it is important to consider your unique circumstances when deciding on any insurance product. Consulting with a financial advisor can help you make an informed decision about whether whole life insurance is the best option for your needs.

Additionally, when considering infinite banking, some people explore alternatives to whole life insurance, such as Indexed Universal Life (IUL) policies. IUL policies offer flexibility and the potential for higher returns, but they may not have the same level of guarantees as whole life insurance. Ultimately, the decision between whole life insurance and IUL for infinite banking depends on individual preferences, financial goals, and risk tolerance.

US Bank Foreign Transaction Fees: What You Need to Know

You may want to see also

Explore related products

![]()

IUL has unique features but also additional downside risks

Indexed Universal Life (IUL) insurance is a type of universal life insurance that provides a cash value component and a death benefit. The cash value in an IUL policy has the potential to grow based on the performance of a stock market index, such as the S&P 500. IUL insurance offers unique features that make it an attractive option for certain individuals.

One of the most appealing aspects of IUL is its potential for higher returns compared to other types of permanent life insurance. The cash value is linked to a stock market index, offering significant growth opportunities during solid market years. IUL also offers downside protection through a "floor", which is a minimum guaranteed return on the cash value. This means that even if the stock market performs poorly, the cash value won't decrease below this floor, providing protection against market downturns.

However, IUL also has additional downside risks and considerations. Firstly, IUL is not an investment but an insurance product, and it should not be considered a replacement for traditional investing. While IUL offers growth opportunities, it comes with additional complexity and a lack of guarantees. The potential for greater cash value accumulation in IUL compared to Whole Life insurance is traded off with more intricate options-hedging strategies employed by insurance companies.

Another downside risk of IUL is the cap on gains. While IUL policies guarantee a minimum interest rate through the "floor", they also typically cap the maximum rate of return that can be earned in a given period. This means that even if the index returns a higher value, the policyholder will only receive up to the capped amount. This cap on gains limits the upside potential in bull markets, which is a trade-off for the protection offered in bear markets.

Additionally, IUL policies may have varying tax implications depending on the region and specific terms of the policy. While policy loans from IUL cash value are often tax-free, there may be potential taxes on the loan in certain jurisdictions. It is crucial to consult a financial professional to understand the tax rules and implications before making any decisions regarding IUL policies.

In conclusion, while IUL has unique features that make it a compelling option for certain individuals, it is important to carefully consider its downside risks and complexities. IUL may provide growth opportunities and downside protection, but it also involves additional risks and considerations that should be evaluated as part of a comprehensive financial plan.

IT Outages: Banks' Biggest Vulnerability?

You may want to see also

Explore related products

![]()

Whole Life Insurance is a safe asset with consistent returns

Whole life insurance is a type of permanent life insurance that provides coverage for an individual's entire life, as opposed to term life insurance, which only covers a specific number of years. It is considered a safe asset due to its guaranteed returns and the financial protection and legal safeguards it offers.

One of the key features of whole life insurance is its cash value component, which allows the policy to accumulate cash value over time. This cash value grows at a fixed rate guaranteed by the insurer, providing consistent returns. Policyholders can borrow against this cash value, utilizing it as a financial asset during their lifetime. The ability to borrow against the policy provides flexibility and can help meet financial goals, such as funding major purchases or providing for a family or business.

Whole life insurance also offers tax advantages. The cash value grows tax-free, and the interest earned may be tax-exempt, depending on the jurisdiction. Additionally, life insurance protection is often given tax benefits not available with other financial instruments. This makes whole life insurance an attractive option for building wealth and supplementing retirement income.

However, it is important to note that whole life insurance tends to have higher premiums than term life insurance, and the low rates of return may not always offset the high costs. Whole life insurance may not be suitable for everyone, and it is essential to carefully consider one's financial goals and risk tolerance before choosing a policy.

In conclusion, whole life insurance is a safe asset with consistent returns due to its guaranteed growth, financial protection, legal safeguards, and tax advantages. It provides individuals with a reliable way to build wealth and protect their loved ones, making it a valuable tool for financial planning and security.

The Evolution of Banks: A Definition and History

You may want to see also

Frequently asked questions

Infinite Banking is a transformative approach to personal finance and wealth management. It involves using permanent life insurance policies as financial instruments to accumulate wealth and access capital.

IUL stands for Indexed Universal Life. It is a type of permanent life insurance policy that offers both financial protection and investment opportunities.

Yes, IULs can be compatible with Infinite Banking. IUL policies offer flexibility, growth potential, and access to cash value, which aligns with the principles of Infinite Banking. However, it is important to work with professionals to design an IUL policy tailored for Infinite Banking.

IULs offer the potential for positive arbitrage, where the cash value can earn more than the loan interest. IULs also provide flexibility in premium payments and the opportunity to lock in low loan rates for life.

IULs may have limited access to cash value in the early years due to surrender periods. Additionally, IULs do not have the same guarantees as Whole Life Insurance and may be subject to market risks. It is important to carefully consider the risks and work with a qualified financial advisor before implementing any strategies.