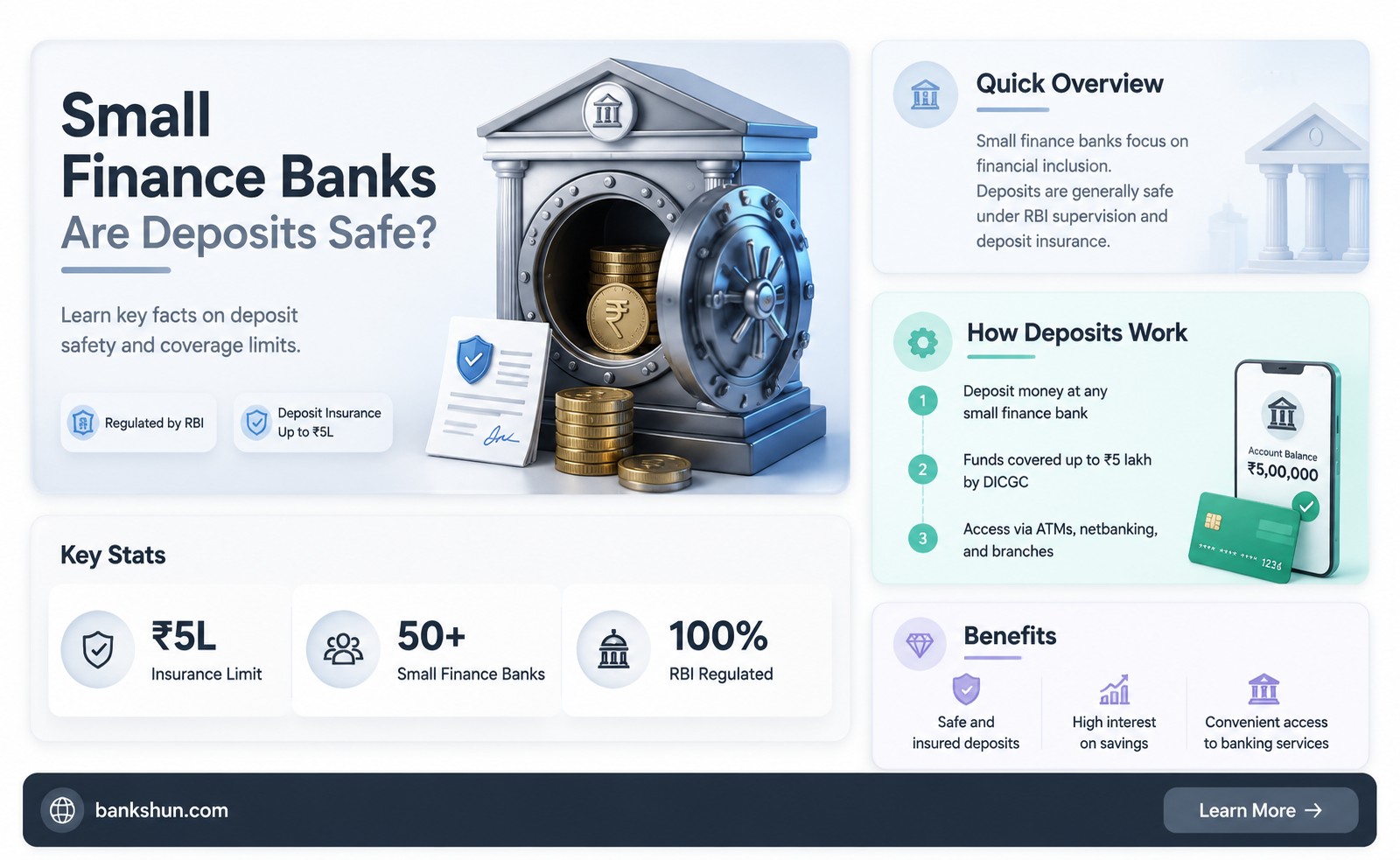

The Deposit Insurance and Credit Guarantee Corporation (DICGC) provides insurance coverage to depositors when banks fail to repay them. It is governed by the provisions of the Deposit Insurance and Credit Guarantee Corporation Act, 1961, and insures all deposits such as savings, fixed, current, and recurring. Each depositor in a bank is insured up to a maximum of ₹5,00,000 (Rupees Five Lakhs) for both the principal and interest amount held by them in the same right and capacity. AU Small Finance Bank, for example, is a small finance bank whose customers' deposits are covered by the DICGC insurance scheme.

| Characteristics | Values |

|---|---|

| What is DICGC? | Deposit Insurance and Credit Guarantee Corporation |

| Who does it cover? | All commercial banks including branches of foreign banks functioning in India, local area banks, regional rural banks, and co-operative banks. |

| How much does it cover? | Up to ₹5,00,000 (Rupees Five Lakhs) for both the principal and interest amount held by the depositor. |

| What types of deposits are covered? | Savings, fixed, current, recurring, etc. |

| What types of deposits are not covered? | Deposits of foreign governments, inter-bank deposits, etc. |

| When was DICGC formed? | 1961 |

Explore related products

What You'll Learn

![]()

Small finance banks are covered under the DICGC Act, 1961

The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a subsidiary of the Reserve Bank of India (RBI) that provides insurance for deposits and credit facilities to commercial banks registered under the RBI Act. The DICGC was formed under the provisions of the DICGC Act, 1961, and the Deposit Insurance and Credit Guarantee Corporation General Regulations, 1961, which are framed and regulated by the RBI.

The DICGC insures all types of deposits, including savings, fixed, current, and recurring accounts. Each depositor in a bank is insured up to a maximum of ₹5,00,000 (Rupees Five Lakhs) for both the principal and interest amount held in the same right and capacity. This insurance covers deposits kept in different branches of a bank, with the total amount insured not exceeding Rupees Five Lakhs.

Small finance banks, such as AU Small Finance Bank, are indeed covered under the DICGC Act, 1961. This coverage is provided for individual bank depositors, including the principal and interest up to ₹5,00,000. In the event of a bank's liquidation, the DICGC will verify the list of outstanding deposits and pay the insured amount to the depositor within 90 days.

Furthermore, the DICGC Act, 1961, mandates that newly established commercial banks must register with the DICGC immediately after receiving their banking license from the RBI. This ensures that small finance banks, as well as other eligible cooperative banks and new regional rural banks, are registered and covered under the DICGC scheme.

Protecting Your Millions: Strategies for Financial Security

You may want to see also

Explore related products

![]()

The DICGC insures deposits up to 5 lakhs

The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a subsidiary of the Reserve Bank of India. It provides insurance coverage for bank deposits up to ₹5 lakh per depositor, per bank. This insurance covers all commercial banks, including foreign banks operating in India, local area banks, and regional rural banks. The insurance covers savings, fixed, current, and recurring deposits.

The DICGC insures all deposits such as savings, fixed, current, recurring, etc., except certain types of deposits such as deposits of foreign governments and inter-bank deposits. Each depositor in a bank is insured up to a maximum of ₹ 5,00,000 (Rupees Five Lakhs) for both the principal and interest amount held by them in the same right and capacity. The deposits kept in different branches of a bank are aggregated for the purpose of insurance cover, and a maximum amount of up to Rupees five lakhs is covered.

For example, if an individual has an account with a principal amount of ₹ 4,95,000 plus accrued interest of ₹ 4,000, the total amount insured by the DICGC would be ₹4,99,000. However, if the principal amount in that account was ₹ 5 lakhs, the accrued interest would not be insured because it exceeds the insurance limit. All funds held in the same type of ownership at the same bank are added together before deposit insurance is determined.

If an individual opens more than one deposit account in one or more branches of a bank, all these are considered accounts held in the same capacity and right. Therefore, the balances in all these accounts are aggregated, and insurance cover is available up to a maximum of Rupees five lakhs. If the individual opens other deposit accounts in a different capacity, such as a partner of a firm or guardian of a minor, these accounts are considered held in a different capacity and right. Accordingly, these deposit accounts will also enjoy insurance cover up to Rupees five lakhs separately.

US Banking System: How Many Banks Are There?

You may want to see also

Explore related products

![]()

DICGC covers all co-operative banks

The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a subsidiary of the Reserve Bank of India (RBI) that provides insurance for deposits and credit facilities to commercial banks registered under the RBI Act. The DICGC insures deposits such as savings, fixed, current, and recurring accounts, covering both the principal and interest amounts up to a maximum of ₹5,00,000 (Rupees Five Lakhs) per depositor. This limit applies to the total amount held by an individual across different branches of the same bank.

In addition to commercial banks, the DICGC also covers cooperative banks, including primary, state, and central cooperative banks, also known as urban cooperative banks. These cooperative banks must function in states or union territories that have amended their Cooperative Societies Act to empower the RBI to regulate the winding up or superseding of cooperative banks. At present, all cooperative banks are covered by the DICGC, as long as they meet the eligibility criteria defined under Section 2(gg) of the DICGC Act, 1961.

The DICGC Act, 1961, mandates that newly established cooperative banks must register with the DICGC within three months of receiving their banking license from the RBI. This ensures that depositors' funds are protected in the event of bank liquidation or other financial difficulties. By insuring deposits in cooperative banks, the DICGC provides confidence and security to customers who choose to keep their savings in these financial institutions.

It is important to note that the DICGC scheme is mandatory, and banks are required to pay an insurance premium semi-annually to settle any claims made by depositors. In the case of liquidation or cancellation of a bank's registration, the DICGC continues to cover deposits until the date of cancellation. However, primary cooperative societies are not insured by the DICGC, and it is essential for depositors to understand the specific coverage provided by the DICGC for their respective banks.

The Fed's Role: Bank Examinations and Their Importance

You may want to see also

Explore related products

![]()

Newly established banks must register with the DICGC

The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a subsidiary of the Reserve Bank of India (RBI) that provides insurance for bank deposits and guarantees credit facilities. The DICGC insures all types of deposits in almost all commercial and cooperative banks, including savings, fixed, recurring, and current accounts. Each depositor in a bank is insured up to a maximum of ₹5,00,000 (Rupees Five Lakhs) for both the principal and interest amounts held in the same right and capacity.

However, the DICGC does not provide coverage for all banks. Notably, banks that are not registered under the DICGC include primary cooperative banks and, most importantly for this context, newly established banks. This means that if an unregistered bank fails or closes unexpectedly, its customers will not receive any money from the DICGC. Therefore, it is crucial for newly established banks to register with the DICGC to offer protection to their customers and ensure their deposits are secure.

To confirm DICGC coverage, investors can check with their bank, ensuring their funds remain safe in case of financial difficulties. Additionally, banks will be able to provide a certificate confirming their DICGC registration. This certificate is furnished by the DICGC upon registration and outlines the protection offered to depositors.

By registering with the DICGC, newly established banks can provide their customers with the assurance that their savings are protected. This accreditation plays a crucial role in instilling confidence in account holders that their deposits are insured up to the specified limit.

Who Holds the Reins at the World Bank?

You may want to see also

Explore related products

![]()

DICGC pays the depositor within 90 days of liability

The Deposit Insurance and Credit Guarantee Corporation (DICGC) is a subsidiary of the Reserve Bank of India (RBI) that insures deposits and guarantees credit facilities to all commercial banks registered under the RBI Act guidelines. Each depositor in a bank is insured up to a maximum of 5,00,000 Indian Rupees (INR) for both the principal amount and the interest accrued.

In the event of a bank's liquidation, the DICGC is liable to pay the depositors the eligible amount, subject to the insurance cover limit, within 90 days of the imposition of All-Inclusive Directions (AID). The process involves the Liquidator, appointed by the respective RCS or CRCS, preparing a list of depositors and their corresponding claim amounts. This list is then sent to the DICGC for scrutiny and payment within 90 days. The DICGC is responsible for verifying the authenticity and genuineness of the claims within 30 days of receiving the list and making the payment to depositors within the subsequent 15 days.

The DICGC's liability in cases of bank liquidation is limited to the extent of deposits at the time of the bank's cancellation of registration as an insured bank. The corporation has no liability in cases of de-registration due to non-payment of premiums or the bank ceasing to be an eligible cooperative bank under the DICGC Act.

It is important to note that the deposit insurance scheme is compulsory, and no bank can opt out of it. The DICGC may cancel the registration of an insured bank if it fails to pay the premium for three consecutive periods, and the public will be notified through newspapers.

Routing Numbers: A US Banking System Exclusive?

You may want to see also

Frequently asked questions

DICGC stands for Deposit Insurance and Credit Guarantee Corporation. It is a subsidiary of the RBI that provides insurance of deposits and credit facilities to commercial banks registered under the RBI Act.

Yes, small finance banks are covered under DICGC. DICGC covers all commercial banks, including small finance banks, functioning in India.

DICGC insures all types of deposits such as savings, fixed, current, and recurring deposits. However, certain types of deposits, such as deposits of foreign governments and inter-bank deposits, are not covered.

DICGC provides insurance coverage of up to ₹5,00,000 (Rupees Five Lakhs) for both the principal and interest amount held by a depositor in the same right and capacity.

When a bank is registered under DICGC, they receive a printed certificate displaying the protection offered to depositors under the DICGC scheme. You can also contact the bank officials to confirm their DICGC coverage.