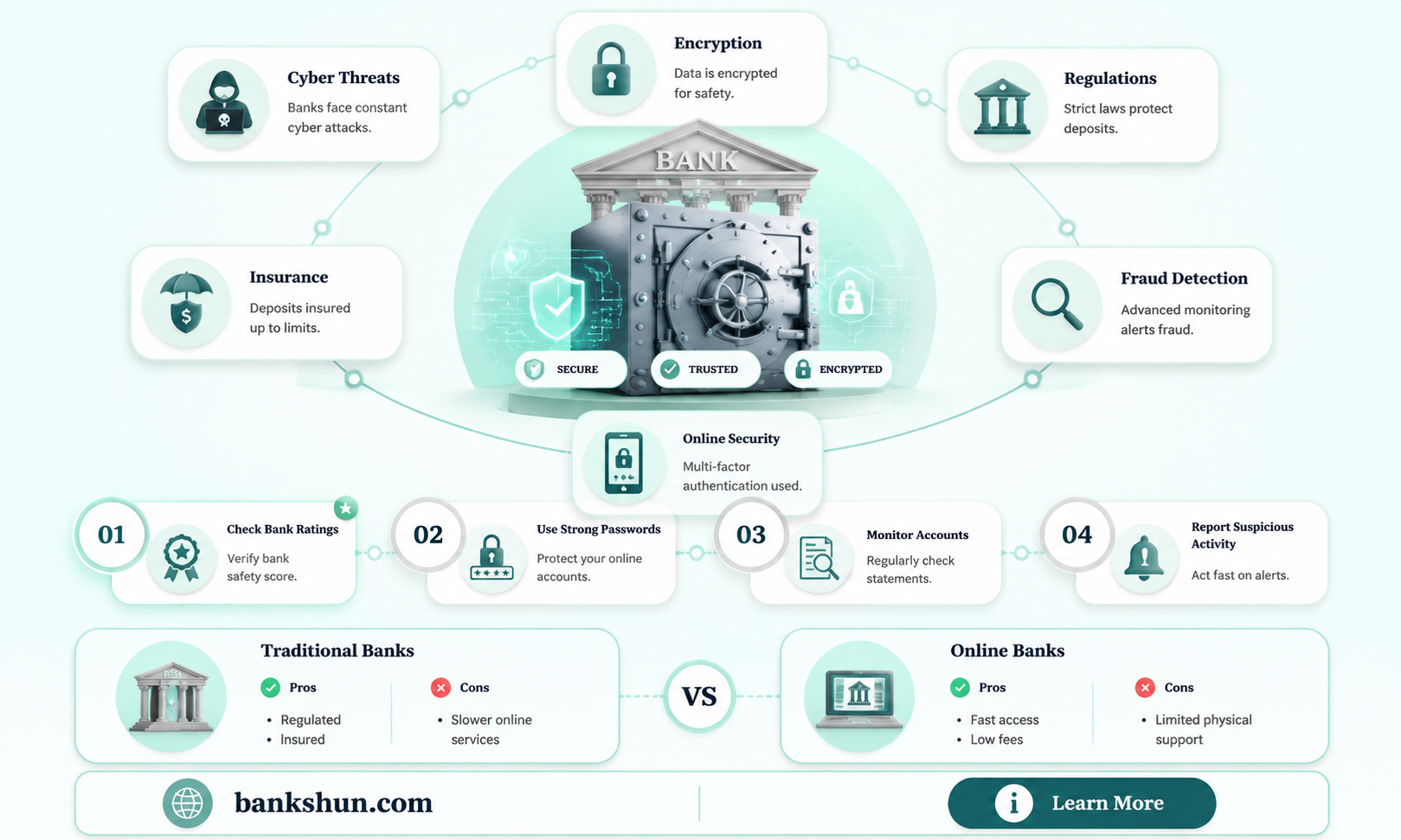

In light of recent global events, such as the COVID-19 pandemic, bank failures, and economic uncertainty, it's understandable to question the safety of your money in banks. While no financial institution is entirely without risk, banks in the United States are generally considered safe places to keep your money. The Federal Deposit Insurance Corporation (FDIC) was established in 1933 to protect consumer bank accounts through deposit insurance, and since then, no one has ever lost money in an FDIC-insured bank. Additionally, banks have implemented advanced security features to protect your data and funds from digital theft and fraud. However, it's important to diversify your investments and stay informed about economic trends to make the most informed decisions regarding your finances.

| Characteristics | Values |

|---|---|

| Number of bank failures in 2023 | 2 |

| Names of banks that failed in 2023 | Signature Bank, Silicon Valley Bank |

| Factors that led to bank failures | Relying on less stable funding such as uninsured deposits, ineffective management of external risks, sharp tightening of monetary policy, decline in asset values |

| Safest banks in the US | JPMorgan Chase, Bank of America, Chase Bank, SoFi, American Express National Bank |

| Factors that make a bank safe | FDIC insurance, encryption, multi-factor authentication, biometric recognition, transaction alerts, responsive customer support |

Explore related products

What You'll Learn

![]()

Banks with long histories are safer

Banks with long histories are generally safer than their newer counterparts. Banks that have existed for several decades have weathered financial storms, built trust over time, and consistently prioritised customer security. These institutions have proven their strength by navigating through recessions, wars, and even a pandemic. As a result, they have established a strong reputation and track record of financial resilience.

Longevity in the banking industry indicates stability and the ability to adapt to changing economic conditions. Banks with long histories are more likely to possess significant assets, such as cash, investments, and real estate, demonstrating their diversification and financial health. Their long-standing presence in the market also suggests that they have consistently prioritised customer security and have strong bank fundamentals.

One example of a bank with a long history is Wells Fargo, which is considered a safe bet for finances due to its substantial resources and 24/7 customer service. Capital One 360 Performance Savings is another option that combines the benefits of online banking with the security of a traditional bank. Regional banks are also worth considering for those who value a more personalised experience without compromising safety.

When evaluating the safety of a bank, it is essential to look for security features such as encryption, multi-factor authentication, biometric recognition, and transaction alerts. Additionally, FDIC insurance is a critical factor, as it provides an extra layer of protection for your deposits. Banks with strong credit ratings from independent agencies, such as Moody's, Standard & Poor's, and Fitch, are also considered safer choices.

While bank failures are rare in the United States due to strong regulations and FDIC protections, it is still important to diversify your investments and savings across different institutions to minimise risk. Overall, banks with long histories have stood the test of time and are more likely to be trusted guardians of your finances.

The Uncanny Resemblance Between Rachel McAdams and Elizabeth Banks

You may want to see also

Explore related products

![]()

FDIC insurance

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance to protect your money in the event of a bank failure. FDIC insurance covers money held in traditional deposit accounts, such as checking and savings accounts, at FDIC-insured banks. Coverage is automatic when you open one of these accounts, and your deposits are insured up to $250,000 per depositor, per FDIC-insured bank. FDIC insurance provides peace of mind, as it ensures that your money is safe even if the bank fails.

The FDIC offers an Electronic Deposit Insurance Estimator (EDIE) on its website, which is a useful tool for calculating the insurance coverage of your deposit accounts. This calculator helps you understand how the insurance rules and limits apply to your specific group of deposit accounts and whether any portion of your funds exceeds the coverage limits. This can be especially helpful if you have multiple accounts or large deposits.

It's important to note that FDIC insurance only applies to deposit accounts at FDIC-insured banks. Banks may offer other financial products and services that are not deposits, and these are not insured by the FDIC. Therefore, it is essential to understand what types of accounts and investments are covered by FDIC insurance. Additionally, FDIC insurance does not cover money held in investment accounts, such as stocks, bonds, or mutual funds.

While FDIC insurance provides a safety net for depositors, it's important to remember that it may not cover all depositors in the event of a systemic crisis. As mentioned in the sources, FDIC insurance "doesn't have nearly enough to cover all depositors." Therefore, it is designed to protect individual depositors rather than provide coverage for everyone simultaneously. Diversifying your assets across multiple institutions or investing in alternative assets like gold, land, or cryptocurrencies can further protect your wealth.

Rolled Coins: Are Banks Accepting Them During COVID?

You may want to see also

Explore related products

![]()

Online-only banks

While some people worry about security with online-only banks, online banking may be the safest way to manage your money. Online banks are generally very safe, carrying FDIC insurance of up to $250,000 per depositor, per bank, per account ownership type. This means your money is federally protected if the bank goes out of business. Many online banks offer this protection, just like traditional banks.

However, some fintech companies advertising accounts online aren't technically chartered banks themselves. Instead, they partner with banks that can provide FDIC insurance and then deposit your money with those institutions. This is completely legitimate, but it does introduce an additional actor between your funds and the FDIC-insured account.

To ensure the safety of your online accounts, you should always use safety precautions such as using a VPN, avoiding public networks, using a secure password, and setting text message alerts for suspicious activity. You can also use a password manager like Bitwarden or Proton Pass, which makes it easy to generate secure passwords and store them for easy use.

Online banks also offer a number of extra security measures to protect your finances and maintain consumer trust. The top three most common security features offered by banks are username and password entry, security questions, and multi-factor authentication. Bank sites also come with data encryption and tokenization, which ensures that your personal data is protected from unauthorized access.

River Banks in Washington: Who Owns Them?

You may want to see also

Explore related products

$14.99 $19.99

![]()

Banks with multi-factor authentication

While no security system is foolproof, adding multi-factor authentication is an effective way to enhance security and reduce the risk of account takeover. This is because multi-factor authentication requires extra verification to access accounts, making it harder for hackers to gain access.

Some banks that offer multi-factor authentication include:

- JPMorgan Chase: This bank offers multi-factor authentication, virtual card numbers, account alerts, and debit card locking for increased digital safety.

- Wells Fargo: This bank provides security features such as multi-factor authentication and activity alerts.

- American Express National Bank: This bank offers FDIC-insured accounts, top-tier fraud detection, and industry-leading customer service.

- Capital One: This bank offers Capital One Cafes and branch locations for in-person support.

Additionally, some banks support Google Authenticator for two-factor authentication without relying on SMS. While SMS-based two-factor authentication is still common, it is being discouraged due to security concerns.

Parking Options Near Citizens Bank Park

You may want to see also

Explore related products

![]()

Credit unions

In addition to safety, credit unions typically charge lower fees and offer better dividends on savings products and lower interest rates on loans than banks. Credit unions also often provide a more personalised service, tailored to individual needs.

However, credit unions may have fewer branches and ATMs than banks, which could be a deciding factor for those who require the convenience of a large branch network.

Infinite Banking: The Perfect Match for IULs?

You may want to see also

Frequently asked questions

Yes, according to financial experts, your money is safe in the bank. It is protected from theft, loss, and natural disasters.

Your money is safe in a bank, even during an economic decline like a recession. Up to $250,000 per depositor, per account ownership category, is protected by the FDIC or NCUA at a federally insured financial institution.

Banks have security features such as encryption, multi-factor authentication, biometric recognition, transaction alerts, and chip cards with secure ATMs.