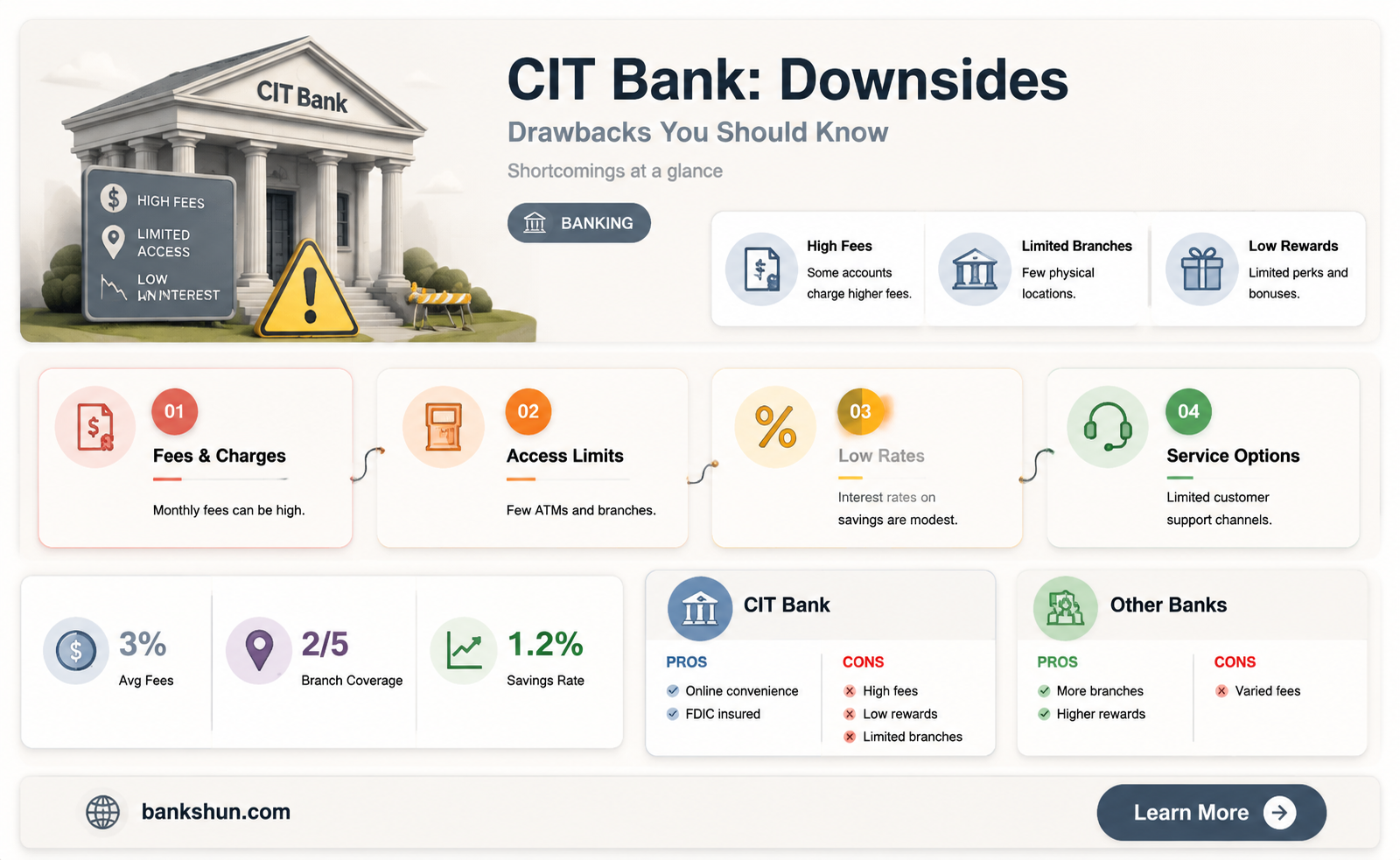

CIT Bank offers a range of financial products, including high-yield savings accounts and certificates of deposit (CDs), with competitive interest rates and yields. However, several downsides to banking with CIT have been noted by customers. Firstly, there is no physical branch network, and while the bank offers 24/7 online account access, customer support is limited to phone and email during specific hours. Additionally, CIT's user interface has been criticised as confusing, and customers have reported issues with login and transactions. The bank also has high minimum opening deposits for certain accounts, and some of its CD rates are considered low compared to competitors.

| Characteristics | Values |

|---|---|

| Interest rates | Competitive for some CDs and savings accounts |

| Fees | No monthly fees, overdraft fees, or incoming wire transfer fees |

| ATM fees | $30 reimbursement for out-of-network ATM fees |

| Minimum deposit | $100 to open an account |

| Customer service | No 24/7 support, no live chat on the website or app |

| Online banking | Easy-to-navigate website and mobile app |

| Physical branches | No physical branches |

Explore related products

What You'll Learn

![]()

Poor customer service

CIT Bank has been criticized by some customers for its poor customer service. The bank has no physical branches, and while customers can reach a customer service representative by phone between 9 a.m. and 9 p.m. Eastern Time on weekdays and for shorter hours on Saturdays, there is no 24/7 support. This is in contrast to many other financial institutions, including online banks, that offer live customer support at any time. CIT Bank also does not offer live chat on its website or mobile apps, which may be a drawback for those who prefer this method of communication.

Some customers have reported long wait times for responses from CIT Bank's customer service team. In one case, a customer reported that it took the bank 8 business days to respond to an issue with their new account and funds being placed on hold. The customer was required to submit bank statements to the fraud department to prove that they owned the funding accounts, which caused a delay in accessing their money.

The bank's website and online interface have also been criticized as difficult to use and not intuitive. One customer reported having login issues and finding the portal challenging to navigate. Another mentioned that the FDIC Bank Find website did not recognize cit.com and citbank.com as valid bank websites, indicating a potential issue with CIT's online presence.

Overall, while CIT Bank offers competitive rates and products, some customers have expressed dissatisfaction with the level of customer service and support they have received, particularly regarding response times, website functionality, and the lack of 24/7 live support options.

International Banking Regulations: Standardization Attempts Examined

You may want to see also

![]()

No physical branches

CIT Bank is an online bank and does not have any physical branches for customers to visit and do their banking in person. This means that customers cannot deposit cash and must instead transfer money from another bank account or via wire or mail. While this may be a downside for some, CIT Bank does offer a range of other services that may make up for the lack of physical branches. These include high-yield savings accounts, competitive interest rates, and the waiving of most fees, including monthly service fees, overdraft fees, and incoming wire transfer fees.

One advantage of having physical branches is the ability to deposit cash. Without physical branches, CIT Bank customers must find alternative ways to deposit cash, such as through electronic transfers, wires, or mail. This may be inconvenient for customers who prefer to deposit cash directly at a bank branch or who do not have easy access to other banks' ATMs or mail services.

Another potential downside of not having physical branches is the lack of in-person customer support. While CIT Bank offers customer service via phone and its mobile app, some customers may prefer to speak to a representative in person to resolve more complex or sensitive issues. The lack of physical branches may also make it more difficult for customers to access certain services or products that are typically offered in-branch, such as safe deposit boxes or certain types of loans.

Furthermore, not having physical branches can limit the bank's ability to build personal relationships with its customers. In-branch banking allows customers to develop relationships with bank staff, which can lead to a better understanding of their financial needs and goals. This personal touch can be important for customers who value a more tailored and human-centric banking experience.

Lastly, the absence of physical branches can impact the bank's presence and visibility in the community. Physical bank branches often serve as a hub for local economic activity and can contribute to a sense of financial stability and trust. Without a physical presence, CIT Bank may find it more challenging to establish itself as a trusted and integral part of the communities it serves. This could potentially affect the bank's ability to attract and retain customers who value community engagement and local investment.

Banco Popular's Customer Service Availability: 24/7 Support?

You may want to see also

![]()

No free ATM network

One downside to CIT Bank is that it does not have its own free ATM network. This is unusual among online banks with checking accounts. However, CIT Bank does offer reimbursements of up to $30 per month for outside ATM fees, and it does not charge any ATM fees itself. This means that customers can use out-of-network ATMs without incurring a fee from CIT Bank, and they can also receive reimbursement for any fees charged by the ATM owner.

The lack of a free ATM network may be a minor inconvenience for some customers, but the reimbursements offered by CIT Bank can help to offset any costs incurred from using out-of-network ATMs. It's worth noting that many other online banks partner with networks that offer tens of thousands of free ATMs nationwide, so customers who rely heavily on ATM access may prefer a bank with this feature.

CIT Bank is an online-only bank, which means that there are no physical branches to visit for in-person banking. This may be another factor to consider when weighing the convenience of accessing cash through ATMs. Without a free ATM network, customers who prefer in-person banking and easy access to cash may find the lack of physical branches and the need to use out-of-network ATMs inconvenient.

However, it's important to note that CIT Bank offers other convenient features, such as mobile check deposit and electronic transfers, which can be used as alternatives to withdrawing cash from ATMs. The bank also has a mobile app that earns high ratings from users, providing easy access to account information and transactions.

In summary, while CIT Bank does not have its own free ATM network, it offers reimbursements for outside ATM fees and does not charge any ATM fees itself. Customers who occasionally use out-of-network ATMs may find this arrangement sufficient, especially with the convenience of online and mobile banking options. However, those who rely heavily on ATM access and prefer the convenience of a wide, free ATM network may find this to be a more significant downside.

Central Banks: Government Partners or Independent Actors?

You may want to see also

![]()

High minimum opening deposits for some accounts

CIT Bank requires a minimum deposit to open an account. While some accounts can be opened with a $100 deposit, others require a minimum of $5,000 to start earning interest. For example, the CIT Bank Platinum Savings account offers a competitive annual percentage yield (APY) of 4.00% to 4.10% for balances of at least $5,000. However, if your balance is below this threshold, you will only earn 0.25% APY, which is significantly lower than the best high-yield savings accounts available. Therefore, this account may not be suitable for those who cannot maintain a minimum balance of $5,000.

The CIT Bank Savings Connect account also requires a minimum deposit of $100 to open, with no minimum balance requirements to earn its 4.00% APY. In comparison, other online banks may offer the option to open a savings account with $0 upfront, providing more flexibility for customers who want to start with a smaller amount.

CIT's eChecking account has a minimum opening deposit of $100, while some competitors in the market allow customers to open a checking account without any minimum deposit requirement. Additionally, to earn a higher APY on this account, a balance of at least $25,000 is necessary.

The minimum deposit requirements at CIT Bank may be a consideration for potential customers, especially those who are looking to start with a smaller amount of money. While the bank offers competitive yields and interest rates, the ability to access these benefits may depend on the customer's ability to meet the required minimum opening deposits and subsequent balance requirements.

Joseph A. Bank Suit Sale: Dates and Deals Revealed

You may want to see also

![]()

Low interest rates on some accounts

CIT Bank offers a range of savings accounts and certificates of deposit (CDs) that provide above-average yields and competitive interest rates. However, it's important to note that not all accounts have equally attractive interest rates.

The Platinum Savings account, for instance, offers a competitive annual percentage yield (APY) of 4.00% to 4.10% for balances of at least $5,000. This APY is significantly higher than the national average. However, for those who cannot maintain a balance of $5,000 or more, the interest rate drops substantially. Balances below this threshold only earn 0.25% APY, which is relatively low compared to other high-yield savings accounts available in the market. Therefore, the Platinum Savings account may not be the best option for individuals who are unsure about maintaining the minimum balance requirement.

The CIT Bank Savings Connect account also offers a competitive APY of 4.00%, and there is no minimum balance requirement to earn this rate. However, a minimum deposit of $100 is required to open this account.

CIT Bank's eChecking account offers a lower APY compared to other online checking accounts. It provides an APY of 0.10% for balances under $25,000 and 0.25% for balances of $25,000 or more. While there are no monthly fees associated with this account, the interest rates are not as competitive as those offered by other banks.

CIT Bank's standard CD rates are also considered low. While the bank offers a no-penalty CD with a solid yield, its jumbo CDs have lower yields than some regular CDs. Additionally, the minimum deposit requirement for opening a CIT CD is $1,000, which may be higher than what some online banks and credit unions offer.

Overall, while CIT Bank provides competitive interest rates on some of its accounts, there are certain accounts with lower interest rates that may not be as attractive to potential customers. It is important for individuals to consider their financial goals and compare the interest rates offered by different financial institutions before deciding to open an account with CIT Bank.

Barclays Bank: Who Owns This Financial Giant?

You may want to see also

Frequently asked questions

CIT Bank falls short compared to its competitors as it doesn't offer 24/7 live customer support. You can access your account information anytime online, through the mobile app or by phone, but actual communication with representatives is restricted to weekdays from 9 a.m. to 9 p.m. Eastern Time and shorter Saturday hours.

CIT Bank's website and app have been criticised for being unintuitive and difficult to use. Some users have also reported login issues.

CIT Bank's accounts have high minimum opening deposits compared to its competitors. The bank also does not provide ATM or debit cards or check-writing privileges.