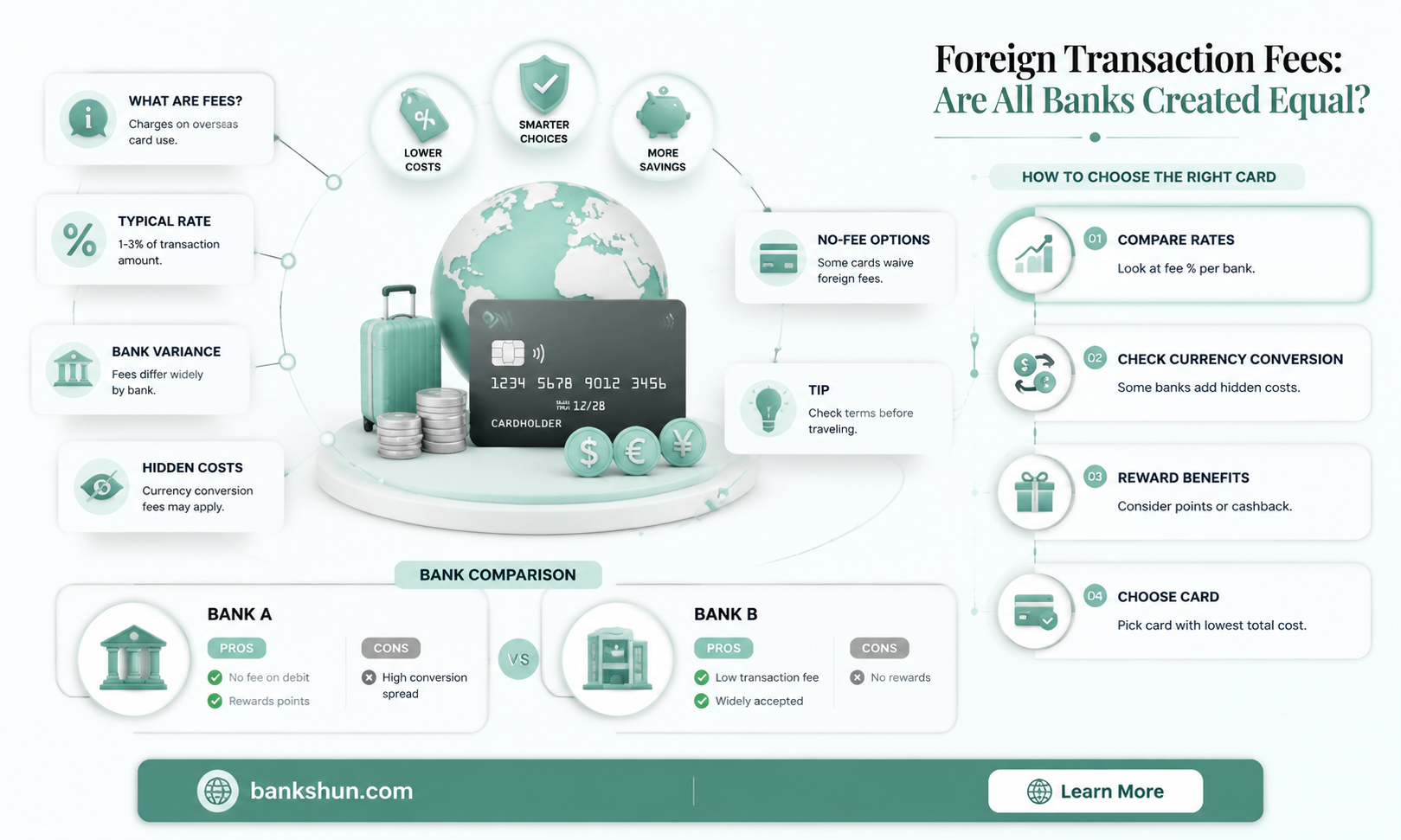

Foreign transaction fees are a charge that your bank or credit card issuer adds to your bill when you make a purchase in a foreign currency or through a foreign bank. These fees are typically around 1% to 3% of the purchase amount, although they can be higher or lower depending on the bank and the type of card. Some banks and credit card issuers do not charge foreign transaction fees, especially those designed for international travel. It is important to check the terms and conditions of your card to see if you will be charged foreign transaction fees, as these fees can add up quickly when travelling abroad.

| Characteristics | Values |

|---|---|

| What are foreign transaction fees? | A surcharge that a credit card issuer adds to purchases made outside the United States. |

| How much are the fees? | Typically around 1% to 3% of the purchase amount. |

| When are these fees charged? | When purchases are processed through overseas banks or in foreign currencies. |

| Are there any banks that don't charge these fees? | Yes, some banks like Capital One and Discover do not charge foreign transaction fees on any of their cards. |

| How to avoid these fees? | Use a card that doesn't charge foreign transaction fees, such as travel cards. |

| What other fees might be charged when using an ATM abroad? | Flat withdrawal charges, currency conversion fees, and fees from the ATM owner. |

Explore related products

What You'll Learn

- Foreign transaction fees are typically 1% to 3% of the purchase amount

- Foreign ATM fees are not the same as foreign transaction fees

- Some banks are part of the Global ATM Alliance, allowing customers to use ATMs worldwide without out-of-network fees

- Dynamic currency conversion (DCC) fees are charged for converting one currency to another

- Foreign transaction fees can be avoided by using a card that doesn't charge them

![]()

Foreign transaction fees are typically 1% to 3% of the purchase amount

Foreign transaction fees are a surcharge levied on purchases made in a foreign currency or processed by a foreign bank. These fees are typically applied when travelling or shopping online from international retailers. Foreign transaction fees are usually imposed by credit card issuers, and they can range from 1% to 3% of the purchase amount, with 3% being a common fee. Visa and Mastercard, for example, charge a fee of 1% on all transactions. On top of the network fee, some issuers add their own charge, which is usually around 2%.

It is important to note that not all cards impose foreign transaction fees. Some cards are specifically designed for international travel and do not charge these fees. For instance, Capital One and Discover are known for having zero foreign transaction fees across all their credit cards. Additionally, some debit cards, such as the Schwab Bank Investor Checking account, will refund any fees incurred from using ATMs abroad.

When planning international travel, it is advisable to review your debit and credit cards to understand the types of fees you may incur on foreign transactions. Using a card that does not charge foreign transaction fees can save you a significant amount of money during your trip.

Furthermore, when making purchases or withdrawing cash abroad, you may be given the option to pay in your home currency. This is known as dynamic currency conversion (DCC), and it often comes with an additional fee, typically around 1% of the transaction amount. You have the right to decline this service and pay in the local currency to avoid the DCC fee.

To summarise, foreign transaction fees can add up quickly, so it is essential to be aware of the fees associated with your cards before travelling. By choosing cards without foreign transaction fees or using ATMs within your bank's network, you can minimise these extra costs and make your money go further during your trip.

US Bank: 24/7 Customer Service Availability

You may want to see also

Explore related products

![]()

Foreign ATM fees are not the same as foreign transaction fees

Foreign ATM fees and foreign transaction fees are two distinct types of charges. Foreign transaction fees are applied by your bank or card issuer when you make a purchase in a foreign currency. This fee is usually a percentage of the purchase amount, typically ranging from 1% to 3%. For example, if you spend $100 abroad and your foreign transaction fee is 3%, you will be charged an additional $3, which will appear as a separate item on your bill. Foreign transaction fees can apply to various transactions made in a foreign country, such as dining at restaurants, staying in hotels, or shopping at retail stores.

On the other hand, foreign ATM fees, also known as international ATM fees, are charged when you use an ATM outside of your home country or bank's network. These fees can be either a flat rate, often ranging from $2 to $5 per withdrawal, or a percentage of the total withdrawal amount, generally between 1% to 3%. For instance, Bank of America charges a $5 fee for global withdrawals. Additionally, there may be a 'conversion fee' or dynamic currency conversion (DCC) fee for converting your transaction into your home currency, which can be as high as 7%. This DCC fee is typically around 1% of the transaction amount, and you have the option to decline it and pay in the local currency to avoid this extra cost.

It is important to note that foreign ATM fees and foreign transaction fees are separate charges. Your bank may charge both types of fees when you use a foreign ATM with your debit or credit card. To avoid unexpected fees, it is recommended to review your cardholder agreement or contact your bank to understand their specific policies on foreign transaction and ATM fees. Some banks, such as Capital One and HSBC, offer accounts with no foreign transaction or ATM fees, while others provide travel credit cards that waive these fees. Additionally, using ATMs within your bank's network or partner banks can help minimize these charges.

Federal Regional Banks: How Many Are There?

You may want to see also

Explore related products

![]()

Some banks are part of the Global ATM Alliance, allowing customers to use ATMs worldwide without out-of-network fees

When travelling abroad, it's important to be aware of the various fees that may be incurred when using your bank card. Foreign transaction fees are usually a percentage of the purchase amount and typically range from 1% to 3%. These fees are considered "out-of-network" fees and are charged when you use your credit or debit card to make a purchase in a foreign currency.

To avoid these fees, some banks are part of the Global ATM Alliance, which is a partnership between major world banks that allows customers to use ATMs worldwide without paying out-of-network fees. For example, Barclays account holders can use ATMs operated by Consorsbank in Germany, Westpac Bank in Australia, New Zealand and several other countries, and Scotiabank in Canada, Mexico, Peru, and several Caribbean countries without incurring transaction charges. Similarly, Scotiabank customers can use ATMs operated by Barclays in the UK and Bank of America in the US without paying additional fees. Bank of America also has a partnership with China Construction Bank, allowing its account holders to use their ATMs in mainland China without incurring usage fees.

It's important to note that while the Global ATM Alliance waives the "out-of-network" ATM fee, you may still be charged a foreign currency transaction fee by your home bank. Additionally, individual ATMs may have their own limits and accepted card types, so it's recommended to research fee-free ATMs before travelling and always choose to be charged in the local currency to avoid unexpected fees.

By choosing a bank that is part of the Global ATM Alliance or opening a checking account that doesn't charge foreign transaction fees, you can minimise the costs associated with using your card abroad.

Banking in New York: US Banks Available

You may want to see also

Explore related products

![]()

Dynamic currency conversion (DCC) fees are charged for converting one currency to another

Dynamic currency conversion (DCC) is a process that allows customers to see the cost of their purchase in their home currency at the point of sale. While this offers transparency and convenience, it often comes with additional fees and an unfavourable exchange rate, resulting in a higher charge on their credit card.

DCC is typically provided by third-party operators in association with the merchant and not the card issuer. The exchange rate offered through DCC includes a markup to the merchant and/or service provider, which can make the rate less attractive than the market rate. This markup is not always disclosed to the customer, and they may end up paying significantly more than the standard exchange rate.

The DCC fee is usually around 1% of the transaction amount, but it can vary depending on the business and the DCC service provider. This fee is bundled into the exchange rate offered to the customer, making it difficult to identify the additional cost. In some cases, the total cost of the transaction with the DCC fee and the foreign transaction fee can be between 2% and 3% or even up to 7% or more.

Customers have the choice to accept or decline DCC when making a purchase. It is important to note that even if they decline DCC and pay in the local currency, they may still be charged a foreign transaction fee by their card issuer. To avoid unnecessary fees, customers can consider using a card that does not charge foreign transaction fees or using a bank that is part of a global ATM alliance, allowing them to withdraw cash without paying out-of-network fees.

Carmax Bank Drafts: Safe to Accept?

You may want to see also

Explore related products

![]()

Foreign transaction fees can be avoided by using a card that doesn't charge them

Foreign transaction fees are a surcharge that banks and credit card issuers add to purchases made outside of the card's home country. These fees are typically around 1% to 3% of the purchase amount but can be as high as 5% or more. Foreign transaction fees can add up quickly, especially when travelling or making multiple purchases in foreign currencies.

To avoid paying foreign transaction fees, it is recommended to use a card that does not charge these fees. There are several credit cards that do not charge foreign transaction fees, including some offered by Capital One, Discover, Bank of America, and American Express. These cards can be a great option for international travellers or those who frequently make purchases in foreign currencies.

In addition to credit cards, there are also some debit cards that do not charge foreign transaction fees. For example, the Schwab Bank Investor Checking account from Charles Schwab offers a debit card that refunds any fees incurred from using ATMs abroad. Some banks, such as Barclays, Scotiabank, and Bank of America, are part of the Global ATM Alliance, which allows customers to use ATMs of other alliance banks worldwide without paying out-of-network fees.

When choosing a card that doesn't charge foreign transaction fees, it is important to consider the acceptance of the card outside of your home country. The four major U.S. networks—Visa, Mastercard, American Express, and Discover—all have an international presence, but their acceptance can vary by merchant and location. It is also worth noting that foreign transaction fees are different from foreign ATM fees, which are charged by banks when using an ATM that is not affiliated with them.

By using a card that doesn't charge foreign transaction fees, individuals can save money when making purchases or withdrawals in foreign currencies. It eliminates the extra cost added to each transaction, providing a more cost-effective option for international transactions.

FIA Question Bank: How Extensive?

You may want to see also

Frequently asked questions

A foreign transaction fee is a surcharge that a credit card issuer adds to purchases made outside the United States. This fee is usually a percentage of the purchase amount and typically ranges from 1% to 3%.

No, not all banks charge foreign transaction fees. Some banks, such as Capital One and Discover, do not charge foreign transaction fees on any of their cards. Additionally, some banks are part of the Global ATM Alliance, which allows customers to use ATMs of other alliance banks worldwide without paying out-of-network fees.

To avoid paying foreign transaction fees, you can use a credit or debit card that does not charge these fees, such as those specifically designed for international travel. You can also withdraw larger amounts of cash less frequently from ATMs to reduce the number of foreign transaction fees incurred.