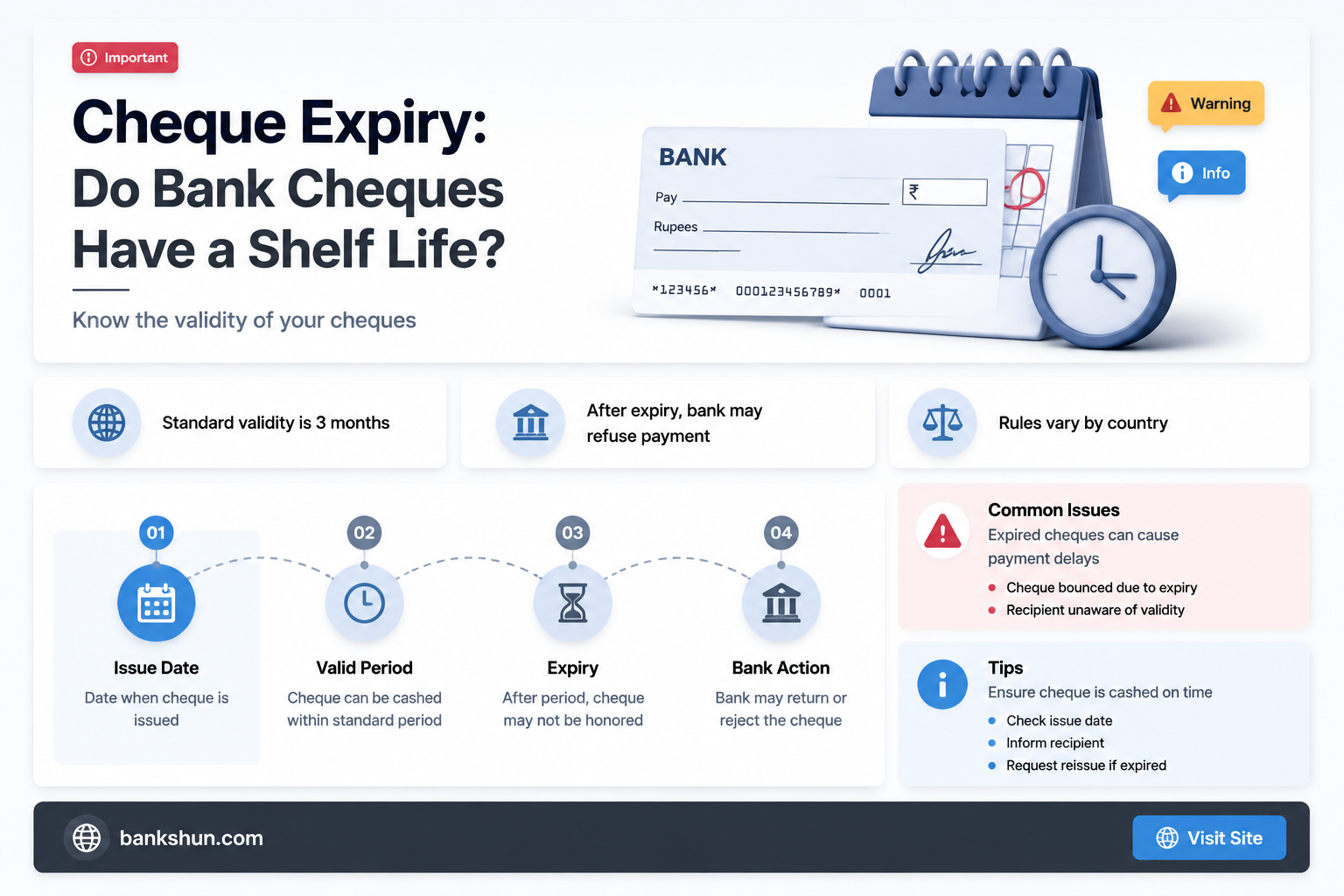

Bank cheques typically have a validity period of six months or 180 days from the date they are issued, after which they are considered stale or expired. However, there is no universal expiration date for all types of cheques, and the validity period can vary depending on the type of cheque and the issuing entity. Personal, business, and payroll cheques usually follow the six-month rule, while some businesses print void after 90 days on their cheques to encourage prompt cashing. U.S. Treasury cheques are valid for a year, and traveller's cheques do not expire as long as the issuing bank is still operating. Understanding cheque expiration dates is essential for effective financial management and avoiding potential issues.

| Characteristics | Values |

|---|---|

| Do bank cheques have an expiry date? | Yes, but it depends on the type of cheque. |

| How long are cheques valid for? | Personal, business, and payroll cheques are valid for 6 months (180 days). Some businesses have "void after 90 days" pre-printed on their cheques, but most banks will honour those cheques for up to 180 days. |

| Are there exceptions? | Yes, traveller's cheques and domestic U.S. Postal Service money orders do not expire as long as the issuing bank is still in operation. U.S. Treasury cheques are valid for one year. |

| What happens if a cheque is not cashed within the validity period? | Legally, banks and credit unions are not obligated to accept stale cheques. However, some banks do accept cheques older than six months. The cheque writer may also decide to put a "stop payment" order on the cheque. |

Explore related products

What You'll Learn

![]()

Personal cheques are valid for six months

Personal cheques are typically valid for six months or 180 days from the date they are issued. After this period, they are considered \"stale\" or expired. While some banks may still honour expired cheques, they are not legally obligated to do so. Therefore, it is recommended to cash or deposit a cheque as soon as possible to avoid any issues.

The six-month validity period for personal cheques is a general rule, but it may not apply to all types of cheques. Some businesses print "void after 90 days" on their cheques, but most banks will still honour these cheques for up to 180 days. This pre-printed language is intended to encourage recipients to cash or deposit the cheques promptly.

It is worth noting that the risk of triggering fees is slightly higher with personal cheques compared to company-printed cheques. This is because companies are less likely to maintain minimal balances in their accounts. Additionally, there is a chance that the cheque writer's account number or routing number may change during the six-month period, or they may have forgotten about the cheque and spent the money elsewhere.

If you have received a personal cheque that is older than six months, you can contact the issuing bank to inquire about their policies regarding stale cheques. Some banks may still accept these cheques, but there is also a possibility that the cheque could bounce due to insufficient funds or a closed account. In such cases, you may need to pay returned cheque fees.

To avoid any complications, it is generally advisable to deposit or cash a personal cheque within six months of receiving it. If you are unable to do so, you can consider contacting the cheque writer to request a replacement cheque with a more recent date.

Written Instructions: Are Banks Legally Bound to Obey?

You may want to see also

Explore related products

![]()

Bank drafts are valid forms of payment

Cheques typically expire after six months, but this can vary depending on the type of cheque and the bank's policies. Some cheques may be valid for up to a year, while others may become stale-dated after 90 days. It's always best to cash or deposit a cheque as soon as possible to avoid any issues.

Bank drafts are a valid form of payment and are often used for large or important transactions where guaranteed funds are required. They are considered more secure than personal cheques because the bank ensures that the payer has sufficient funds before issuing the draft. The funds are withdrawn from the payer's account and held in the bank's reserve account until the draft is cashed by the payee. This provides assurance to the recipient that the payment will not bounce.

Bank drafts are typically used for significant purchases, such as buying property or a car, where the seller wants certainty of payment. They can also be useful when making large transactions in different currencies, as bank drafts can be issued in various currencies. Additionally, bank drafts offer a convenient alternative to carrying large sums of cash.

To obtain a bank draft, individuals must visit their financial institution and provide identification. The bank verifies the availability of funds and then prepares the draft with the payee's name and the payment amount. The draft may also include security features such as serial numbers, watermarks, and micro-encoding. Once issued, the bank draft cannot be cancelled, and it is the purchaser's responsibility to deliver it to the intended recipient.

While bank drafts offer security and peace of mind for large transactions, there are a few considerations to keep in mind. Bank drafts may incur additional fees, and the process of issuing them can be time-consuming. Furthermore, as with any physical document, there is a risk of loss or theft. Nevertheless, bank drafts remain a reliable and secure payment option, especially when dealing with substantial sums of money.

Best Banks for International Travel: No Foreign Transaction Fees

You may want to see also

Explore related products

![]()

Traveller's cheques never expire

Different types of bank cheques have different expiration dates. Personal, business, and payroll cheques typically have a validity of 6 months (180 days), while some businesses issue cheques that are "void after 90 days". US Treasury cheques are valid for a year from the date on the cheque. Cashier's cheques may not have a specified expiration date, but they can become stale or outdated after 60, 90, or 180 days, and banks may put their own expiration dates on these cheques.

Traveller's cheques, on the other hand, do not expire. Issuers like American Express state that their traveller's cheques have no expiration date and remain backed by the company. Traveller's cheques were first issued in 1772 and became widely used from the 1850s to the 1990s as a safer alternative to carrying large amounts of cash when travelling abroad. They were also convenient as they could be exchanged for local currency at banks or merchants, and their value would be reimbursed if stolen.

However, with the introduction of more modern payment methods such as credit and debit cards, prepaid currency cards, and digital wallets, the use of traveller's cheques has declined significantly. They are now considered less common and may not be easily redeemable, even at the issuer or the purchaser's bank. Many former issuers, such as Thomas Cook, Bank of America, Chase, and AAA, have discontinued their traveller's cheque programs or gone out of business.

If you have old traveller's cheques, it is recommended to get the value back as soon as possible. They can be redeemed directly with the issuer or at eligible foreign exchange partners or merchants. It is important to carry the original purchase receipt and present photo identification when redeeming traveller's cheques. Additionally, some banks may allow account holders to deposit traveller's cheques, but fees may apply.

Stop Payment Fees: Banks' Unnecessary Charges

You may want to see also

Explore related products

![]()

Money orders rarely expire

Bank cheques typically have an expiry date of 6 months (180 days). However, this may vary depending on the type of cheque and the issuing bank. Some cheques may be valid for up to a year, while others may become stale-dated after 90 or even 60 days. After the expiry date, banks are under no obligation to honour the cheque, and you may incur additional fees if it is still cashed.

In contrast, money orders rarely expire. They are a safe and affordable alternative to personal cheques, as they are prepaid and guaranteed. This means that the recipient can be confident that they will receive their cash whenever they decide to cash it. Money orders from USPS, for example, never expire and retain their value indefinitely.

However, while money orders do not have an expiration date, there are some considerations to keep in mind. Firstly, some issuing institutions may charge fees for cashing older money orders, reducing their value over time. These fees can eventually render the money order worthless if left for too long. Secondly, by law, if money orders are not cashed within a certain time period, they may be turned over to the state as unclaimed property. Therefore, while money orders themselves do not expire, they may become subject to abandoned property regulations or fees that effectively reduce their value or usefulness.

It is also important to note that money orders can usually be canceled if they are reported lost or stolen. In such cases, you would need to request a new money order from the issuer. Additionally, money orders may have maximum values, such as \$1,000 for USPS money orders.

In summary, while money orders do not typically expire, it is important to be aware of any fees or regulations that may impact their value over time. It is always recommended to carefully review the terms and conditions provided by the issuing institution before acquiring or cashing a money order.

Treasury Departments: A Bank's Essential or Optional Feature?

You may want to see also

Explore related products

![]()

Issuing banks may honour expired cheques

While cheques typically have an accepted expiry date of six months or 180 days, after which they are considered "stale", some issuing banks may still honour expired cheques. This is because, in legal terms, a cheque is valid for as long as the debt between the issuer and the recipient exists. In other words, cheques don't technically expire.

However, it is common banking practice to reject cheques that are over six months old. This is to protect the cheque writer, in case the payment has been made another way or the cheque has been lost or stolen. If a cheque is rejected, the recipient can request a new cheque from the issuer.

If you are in possession of a stale-dated cheque, it is recommended that you contact both your bank and the issuing bank to find out their policies. Even if a cheque is expired, it may still be honoured by either bank. However, there is a possibility that the cheque could bounce if the issuer no longer has sufficient funds to cover the amount or if they have closed their account. It is also important to note that the issuer may have put a stop payment order on the cheque, in which case it cannot be cashed or deposited.

If you are the issuer of a cheque and have been waiting an unusual amount of time for it to be cashed, it is a good idea to contact the recipient to ensure the cheque has not been lost or stolen.

ICS: International Banking's Secret Code

You may want to see also

Frequently asked questions

Bank cheques typically have a six-month expiration date, after which they are considered stale and banks are not legally obligated to accept them. However, some banks may still honour stale cheques, and government cheques can be cashed freely at any time.

Personal, business, and payroll cheques usually have a validity of six months or 180 days. Some businesses print void after 90 days on their cheques, but most banks will still honour them for up to 180 days. U.S. Treasury cheques are valid for one year, while cashier's cheques may have varying expiration dates depending on the issuing bank. Traveller's cheques and domestic U.S. Postal Service money orders do not expire as long as the issuing bank is still operating.

If you have a stale cheque, you should first contact the issuing bank to understand their policies. You may also need to contact your bank to learn about their specific rules regarding stale cheques. While some banks may still honour stale cheques, there is a risk of the cheque bouncing due to insufficient funds or a stop payment order placed by the issuer.