Bank errors are not uncommon, and they can have a significant impact on a company's financial statements and reporting. When a bank error occurs, it can lead to reconciliation issues, affecting the accuracy of a company's books. To identify and correct these errors, companies perform bank reconciliation, which involves comparing internal records with bank account statements. This process helps businesses maintain financial accuracy and address any discrepancies between their records and the bank's records. While bank errors can occur, it is important to note that they are less frequent than bookkeeping errors, and proper reconciliation procedures can help prevent and identify issues in either case.

| Characteristics | Values |

|---|---|

| Bank errors | Bank errors can occur due to various reasons, such as transposition errors, lost deposits, or issues with credit cards. |

| Impact | Bank errors can lead to reconciliation errors, affecting financial reporting, accuracy of financial statements, tax complications, and cash flow management. |

| Detection | Detecting bank errors requires regular bank reconciliation, which involves comparing internal records with bank statements and can be done monthly, weekly, or daily. |

| Correction | To correct bank errors, a reconciling item is added to the book side of the bank reconciliation, adjusting the book balance to match the bank statement. |

| Prevention | To prevent bank errors, it is essential to have strong internal controls, train staff on best practices and software use, and implement duplicate transaction detection software. |

Explore related products

What You'll Learn

![]()

Bank errors during manual entry

Bank errors can occur during manual entry, and these can be challenging to identify and rectify. While banks do make errors, the likelihood of an error in their statement is very low, and it is more probable that the mistake lies in the bookkeeping entries.

Manual data entry can lead to errors such as incorrect amounts being recorded, which can be due to processing fees or other factors. For example, a customer payment of $1,200 may have been recorded, but only $1,000 was deposited in the bank, creating a discrepancy. This could also be caused by transaction fees or bank charges. It is crucial to review transaction details and ensure that all entries match the bank statement to maintain accurate account balances.

Another common issue is duplicate entries. This can occur when the same payment is recorded through both manual entry and an automatic bank feed. It is essential to regularly review transactions to identify and rectify such duplicates.

Bank reconciliation is a critical process in identifying and resolving errors. It involves comparing the company's books with the bank's records to ensure accuracy. This can be done manually or through specialised software. By performing regular reconciliations, businesses can identify and address errors promptly.

When a bank error is identified, they typically use two methods to resolve it: reversal and adjustment. In the reversal method, the bank reverses the entire incorrect transaction amount, creating a net of zero. They then process a new transaction for the correct amount. In the adjustment method, the bank creates a new transaction entry to make up for the difference between the original amount and the error. For example, if a payment of $100 was recorded as $10 due to an error, the bank would create an adjustment entry of $90 to correct the mistake.

Notary Services: Banks and Beyond

You may want to see also

Explore related products

![]()

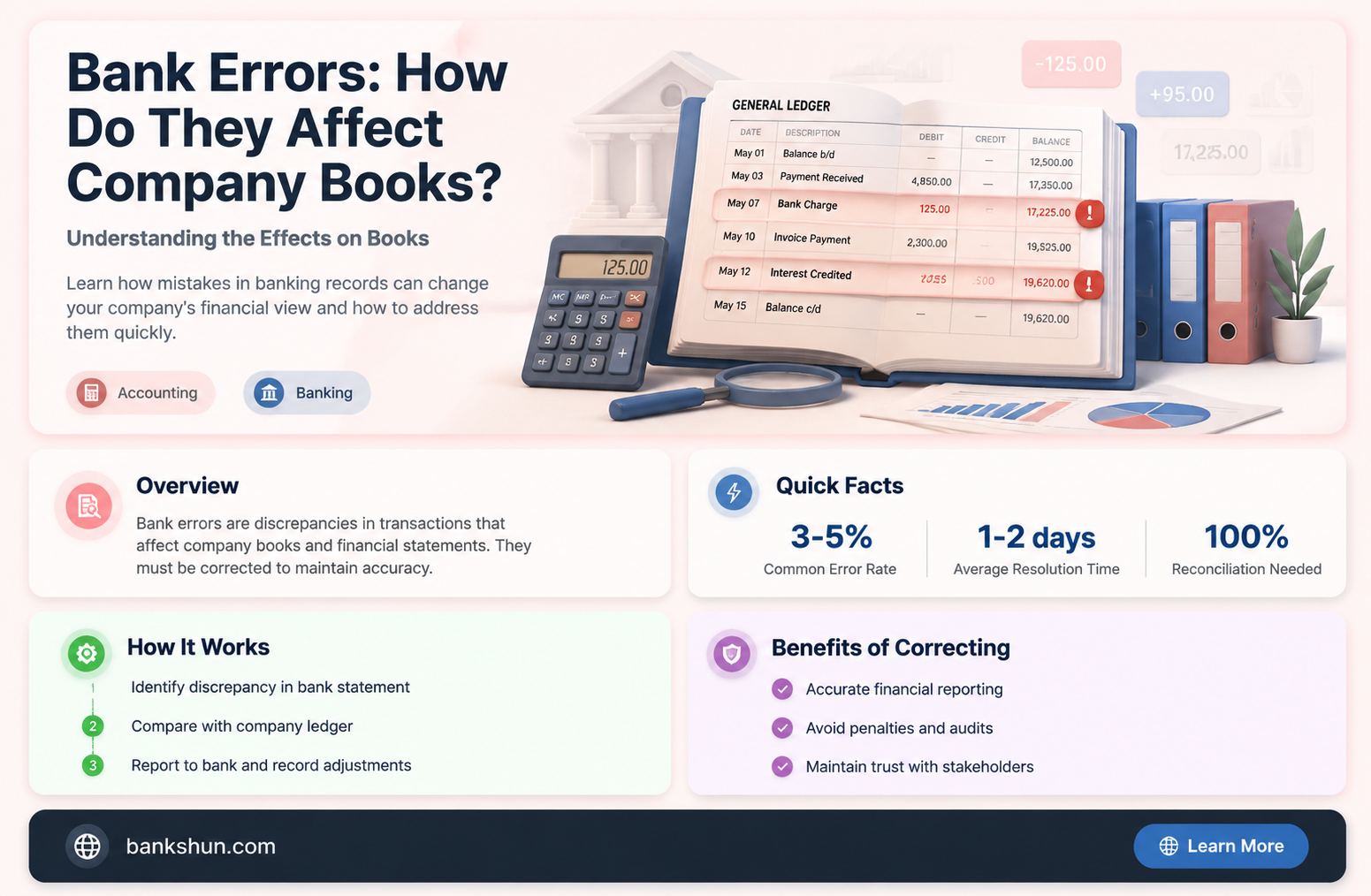

Bank reconciliation statements

A bank reconciliation statement is a financial document that compares an account's balance on a company's books to the balance in that account according to the bank statement. It is a summary document that shows whether the recorded bank account balance of the company matches the balance recorded by the bank. The bank reconciliation process is an important financial control that helps ensure a company's financial records are accurate and that there are no unexplained inconsistencies in day-to-day transactions.

The process involves comparing the transactions recorded in the company's electronic bank statements (EBS) or electronic cash book with its e-passbook or digital passbook. This is done to identify any inconsistencies in the transactions. The statement covers all transactions of the company, including deposits and withdrawals. It typically contains the following information: the opening balance of the bank account according to the accounting system, a list of checks, deposits, or other payments made to and from the bank account that have not cleared the bank, any other transactions not yet reflected in the bank statement, adjustments made to reconcile the differences between the bank statement balance and the accounting system balance, and the final reconciled balance of the bank account according to the accounting system.

While bank errors do occur, they are relatively uncommon, and it is more likely that errors are made in a company's bookkeeping entries. Bank reconciliation statements help to identify these errors so that they can be corrected.

Digital Money: Central Bank's New Currency

You may want to see also

Explore related products

![]()

Transposition errors

A peculiar mathematical phenomenon can help identify transposition errors. The difference between the incorrect and correct amounts will always be evenly divisible by 9. For instance, if a bookkeeper writes 72 instead of 27, the difference is 45, which is divisible by 9, yielding 5. Similarly, if 63 is recorded instead of 36, the difference of 27 divided by 9 gives us 3. This rule can be used to detect transposition errors in accounting.

To identify transposition errors in a trial balance, find the difference between total debits and credits, add 1 to the first digit of the difference, and investigate ledger account balances where the difference between the first and second digits matches this value. For example, if the difference between debits and credits is $540 (5+1=6), investigate accounts with a difference of 6 between the first and second digits. This method helps pinpoint the accounts where transposition errors may have occurred.

To prevent transposition errors, businesses can avoid manual data entry by using expense tracking apps that automatically update accounting software. Additionally, reconciling bank statements with accounting records monthly can help identify and correct errors promptly. Double-entry bookkeeping can also reduce transposition errors by ensuring that errors affecting the trial balance are identified and addressed.

Banks Without FDIC Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Duplicate transactions

Once you have identified duplicate transactions, you have a few options for addressing them. One approach is to delete the duplicate transactions and retain only the original entries. This can be done by marking the transactions you want to keep and utilising the "Keep Marked Transactions" function. However, it is important to note that simply deleting duplicate transactions may not automatically reconcile your accounts. Additional steps may be necessary to ensure that your books are accurate and up to date.

Another option is to undo the entire reconciliation process and start over. This may be necessary if the duplicate transactions have affected your reconciled balances. By undoing the reconciliation, you can correct the errors and ensure that your accounts are properly aligned.

In certain cases, you may also have the option to merge duplicate transactions. This can be useful when dealing with reconciled and unreconciled transactions without having to redo the entire reconciliation process. However, the ability to merge transactions may depend on the specific accounting software you are using and the nature of the transactions involved.

To prevent duplicate transactions in the future, it is recommended to use advanced modes in your accounting software that allow for automatic transaction recognition and matching. This can help streamline the process and reduce the likelihood of errors. Regular bank reconciliations are also crucial in identifying and correcting duplicate transactions or other discrepancies between your internal records and bank statements.

Banking Hours: New Year's Eve Operations

You may want to see also

Explore related products

$12.89 $13.89

![]()

Bookkeeping errors

Reconciliation errors can occur when balances don't add up or there is an unmatched entry. These errors can be caused by duplicated transactions or missing entries that throw your books off balance. It is important to regularly review your bookkeeping to avoid accounting software errors, which can be caused by incorrect settings or a failure to check automated work. Data entry accounting errors occur when inaccurate data or information is entered into your books, such as entering an incorrect number or the correct number in the wrong order.

To correct accounting errors, you can make a "correcting entry" in your journal. This type of entry adjusts an accounting period's retained earnings, or your profit minus expenses. It is part of the accrual accounting system, which uses double-entry bookkeeping. For example, if $1000 worth of salaries payable wasn't recorded, you would need to add a $1000 journal entry under "salary expense" (debit) and another $1000 under "salary payable" (credit).

To avoid bookkeeping errors, it is recommended to perform reconciliations on a monthly and yearly basis, depending on the type of reconciliation. Bank reconciliations can be done at month-end, while fixed asset reconciliations can be done at year-end. It is also important to customize your chart of accounts for your business and stay on top of your expenses and financial statements.

M&T Bank Stadium: A History of Baltimore's Stadium

You may want to see also

Frequently asked questions

It depends on your needs. If you have simple accounting needs, you should reconcile your accounts at least monthly. Businesses with a higher volume of transactions should consider increasing the frequency of reconciliation—either daily or weekly.

A bank reconciliation statement is a financial document that compares an account’s balance on your company’s books to the balance in that account according to your bank statement. It helps to identify and correct errors and uncleared transactions.

Errors during manual entry, duplicate transactions, and forgetting to track issued cheques are some common errors found during bank reconciliation.

To correct this discrepancy, a reconciling item is added to the book side of the bank reconciliation. This adjustment ensures that the book balance reflects the correct amount based on the bank statement.