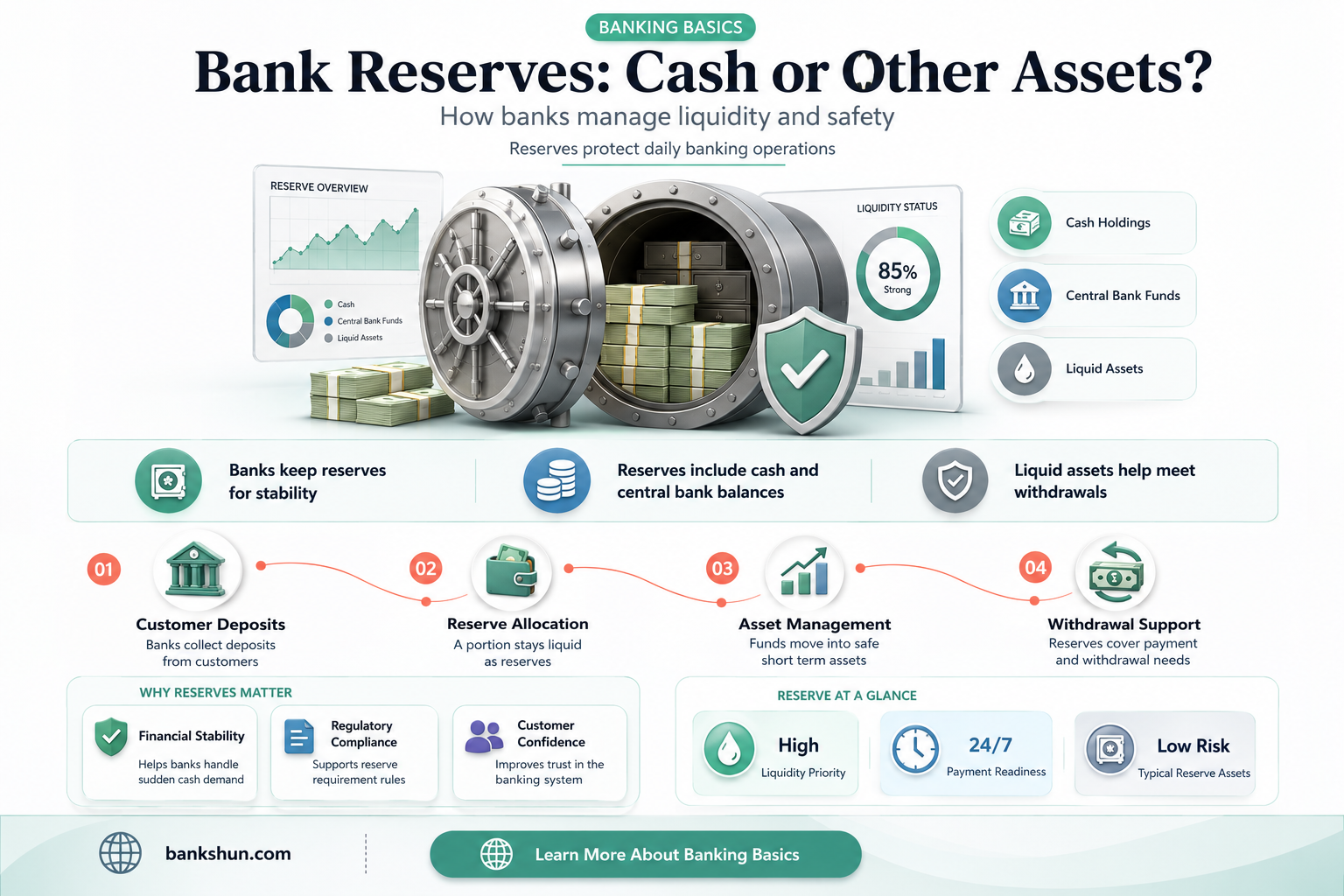

Bank reserves are the minimum amount of cash that financial institutions must retain to meet central bank requirements. They are also referred to as required reserves or excess reserves. The central bank of each country decides the minimum amount, which is typically a percentage of the total bank deposit amounts. Bank reserves are essential to ensure that financial institutions have enough cash to meet consumer withdrawals and withstand financial crises. They also help maintain public confidence in the banking system by ensuring that banks have sufficient cash on hand to prevent bank runs. In some countries, such as the United States, there are currently zero reserve requirements, while in others, such as China and India, the central bank uses changes in reserve requirements to manage inflation and liquidity.

| Characteristics | Values |

|---|---|

| Definition | Bank reserves are the cash minimums financial institutions must retain to meet central bank requirements. |

| Purpose | To ensure that financial institutions have enough cash to meet financial obligations such as consumer withdrawals and to withstand financial crises. |

| Types | Required reserves and excess reserves. |

| Required reserves | The minimum cash the bank can keep on hand. |

| Excess reserves | Any cash over the required minimum that the bank is holding in its vault rather than lending out to businesses and consumers. |

| Reserve requirements | Central bank regulations that set the minimum amount that a commercial bank must hold in liquid assets. |

| Liquidity Coverage Ratio (LCR) | A tool used by banks to prevent financial devastation resulting from a crisis. It helps banks decide how much money they should have based on their assets and liabilities. |

| Central bank role | The central bank of each country decides the minimum amounts for bank reserve requirements. For example, in the US, the Federal Reserve determines all bank reserve requirements for US financial institutions. |

| Interest on reserves | Traditionally, central banks did not pay interest on reserve balances, but such schemes have become increasingly common in the 21st century. |

| Impact on the economy | Bank reserves can help keep the economy functioning efficiently by ensuring consumers have access to their money. |

| Recent changes | During the global pandemic in 2020, the US Federal Reserve cut the reserve requirement ratios to zero percent, eliminating reserve requirements for all depository institutions. |

Explore related products

What You'll Learn

![]()

The reserve ratio is set by the central bank

The reserve ratio, often referred to as the cash reserve ratio, is a critical component dictated by central banks to ensure economic stability. It is the percentage of deposits that banks must hold in cash and not lend out. The reserve ratio is set by the Federal Reserve Board's Regulation D, which sets uniform reserve requirements for all institutions with transaction accounts.

The reserve ratio is a critical tool used by the Federal Reserve to regulate the US money supply and ensure economic stability. It mandates the percentage of deposits banks must retain rather than loan out or invest. In times of economic growth, a lower reserve ratio facilitates increased lending, stimulating the economy by putting more money in circulation. Conversely, during inflationary periods, a higher reserve ratio helps reduce the money supply to stabilize prices.

The required bank reserve follows a formula set by Federal Reserve Board regulations. The formula is based on the total amount deposited in the bank's net transaction accounts, including demand deposits, automatic transfer accounts, and share draft accounts. Net transactions are calculated as the total amount in transaction accounts minus funds due from other banks and cash that is in the process of being collected.

The reserve ratio is sometimes used by a country's monetary authority as a tool in monetary policy to influence the country's money supply by limiting or expanding the amount of lending by banks. For example, the People's Bank of China uses changes in the reserve requirement as an inflation-fighting tool, raising the reserve requirement ten times in 2007 and eleven times since 2010.

Wells Fargo: Are Other Banks Following Their Lead?

You may want to see also

Explore related products

![Bank deposits and legal reserve requirements; a study of the legal reserve requirements of the Federal Reserve System in the light of the composition and behavior of deposits in member [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

$27.95

![]()

Banks must meet LCR requirements

Bank reserves refer to the cash minimums that financial institutions must retain to meet central bank requirements. These reserves are typically stored in a bank vault or held as deposits in the bank's account with the central bank. The required reserve ratio is set by the central bank and is based on the total amount deposited in the bank's net transaction accounts. This includes demand deposits, automatic transfer accounts, and share draft accounts.

The Liquidity Coverage Ratio (LCR) is a requirement that was introduced by the Basel Committee on Banking Supervision (BCBS) as part of the Basel III post-crisis reforms. The LCR is designed to ensure that banks hold a sufficient reserve of high-quality liquid assets (HQLA) to cover their short-term obligations and protect against liquidity risk. The ratio requires banks to hold liquid assets equivalent to at least their expected total net cash outflows over a 30-day stress period.

The LCR became a minimum requirement for BCBS member countries on January 1, 2015, starting at 60% and increasing by 10 percentage points annually until it reached 100% on January 1, 2019. This gradual implementation was intended to avoid disruption to the strengthening of banking systems and the financing of economic activity.

In the United States, the Office of the Comptroller of the Currency (OCC) has issued regulations regarding the applicability of the LCR. Under these regulations, banks with assets between $50 billion and $250 billion are exempt from meeting the LCR requirements. Only the largest U.S. banks, with total assets of $700 billion or more or cross-border activity of $75 billion or more, are required to maintain a 100% LCR ratio.

While the LCR focuses on a bank's ability to meet short-term obligations, capital requirements focus on a bank's ability to absorb losses over the longer term. The largest and most interconnected banks, known as global systemically important banks (G-SIBs), are subject to additional capital requirements due to the potential impact of their failure on the financial system.

International Bank Transfers: How Long Do They Take?

You may want to see also

Explore related products

![]()

Reserve requirements vary by country

Bank reserves are the cash minimums that financial institutions must retain to meet central bank requirements. These reserves are typically held in the bank's vault or in an account with the central bank. The central bank sets the minimum amount, which is usually determined as a proportion of the bank's deposit liabilities. This rate is known as the cash reserve ratio or reserve ratio.

While the central bank sets the minimum reserve requirements, the actual amount of reserves held by a bank can vary. Banks may hold excess reserves, which are any funds above the required minimum. These excess reserves may be kept in the bank's vault or lent out to businesses and consumers. However, banks have little incentive to maintain excess reserves as cash earns no return and may lose value over time due to inflation.

The reserve requirements vary across different countries and are adjusted based on economic conditions and monetary policies. For instance, the People's Bank of China uses changes in reserve requirements to combat inflation, while the Reserve Bank of India adjusts its cash reserve ratio (CRR) to manage liquidity during financial crises. On the other hand, countries like Canada, the UK, New Zealand, Australia, Sweden, and Hong Kong have no reserve requirements.

In the United States, the Federal Reserve sets the reserve requirements for banks. During the 2020 pandemic, the Federal Reserve cut the cash reserve minimum to zero percent. Prior to this, the Federal Reserve had different reserve requirement ratios for net transaction accounts, with a zero percent ratio for accounts below a certain threshold and a higher ratio for accounts above that threshold. The Federal Reserve also used to set reserve requirements based on categories of deposit liabilities, with different percentages for different levels of eligible deposits.

The reserve requirements are an important tool for a country's monetary authority to influence the money supply and control the amount of lending by banks. However, changes in reserve requirements can have disruptive effects on financial markets, so central banks may prefer to use other monetary policy instruments to achieve their goals.

Which Bureaus Do Banks Pull for Job Applicants?

You may want to see also

Explore related products

![]()

Banks hold reserves in vaults or with the Federal Reserve Bank

Bank reserves refer to the cash minimums that financial institutions must retain to meet central bank requirements. These reserves are kept to ensure that banks can meet any large and unexpected demand for withdrawals. In the United States, the Federal Reserve dictates the amount of cash, called the reserve ratio, that each bank must maintain. This reserve ratio has historically ranged from 0% to 10% of bank deposits.

Most institutions hold their reserves directly with their Federal Reserve Bank. As of November 2001, aggregate required reserves of depository institutions were $39.1 billion, with vault cash accounting for $31.2 billion and reserve balances with Federal Reserve Banks at $8.9 billion. Small banks may keep part of their reserves at larger banks and access them as needed. This flow of cash between vaults peaks during holiday seasons when consumers withdraw extra cash. Once the demand subsides, banks ship off some of their excess cash to the nearest Federal Reserve Bank.

The Federal Reserve's role is to provide the nation with a safe, flexible, and stable monetary and financial system. It can achieve this by lowering or raising the reserve requirement to influence economic activity. In recent years, the Federal Reserve has turned to other tactics such as quantitative easing to achieve its goals.

KYC in Banking: What It Stands For and Why It Matters

You may want to see also

Explore related products

![]()

Banks have little incentive to maintain excess reserves

Bank reserves are the minimum amounts of cash that banks are required to keep on hand to meet short-term obligations and prevent panic in the event of unexpected demand or large withdrawals. These reserves are typically held in a bank's vault or at a central bank. The required reserve ratio is set by the central bank and is based on the bank's total liabilities, such as customer deposits. Any funds held above this required amount are known as excess reserves.

Banks have traditionally had little incentive to maintain excess reserves because cash earns no return and is subject to inflation, resulting in a potential loss of value over time. Banks prefer to lend out this money to generate interest income rather than hold it idle in their vaults. Therefore, banks normally minimise their excess reserves, lending out the money to clients instead.

However, this dynamic changed to some extent following the 2008 financial crisis. As part of the Emergency Economic Stabilization Act of 2008, the Federal Reserve began paying banks interest on their reserves for the first time in history. This provided banks with an incentive to hold excess reserves, as they could now earn a small but risk-free return. As a result, excess reserves spiked, reaching a record $2.7 trillion in August 2014.

Nevertheless, the opportunity cost of holding excess reserves remains a consideration for banks. Banks must weigh the benefits of earning interest on reserves against the potential income generated by lending out that money. Therefore, banks will generally keep their cash reserves as low as is prudently necessary to maintain liquidity and cover anticipated short-term transactions. In the end, it is the balance between these factors that determines how much banks choose to hold in excess reserves.

Mortgages: Banking Industry's Core Business?

You may want to see also

Frequently asked questions

Yes, bank reserves are a commercial bank's cash holdings physically held by the bank. However, they can also be in the form of deposits held in the bank's account with the central bank.

Bank reserves are the cash minimums financial institutions must retain to meet central bank requirements. They are also referred to as required reserves or excess reserves.

Bank reserves ensure that financial institutions can support consumer withdrawals and withstand a financial crisis. They also help in keeping the economy functioning efficiently.

The central bank of each country decides the minimum amount of reserves required by commercial banks. For example, in the United States, the Federal Reserve determines all bank reserve requirements for US financial institutions.