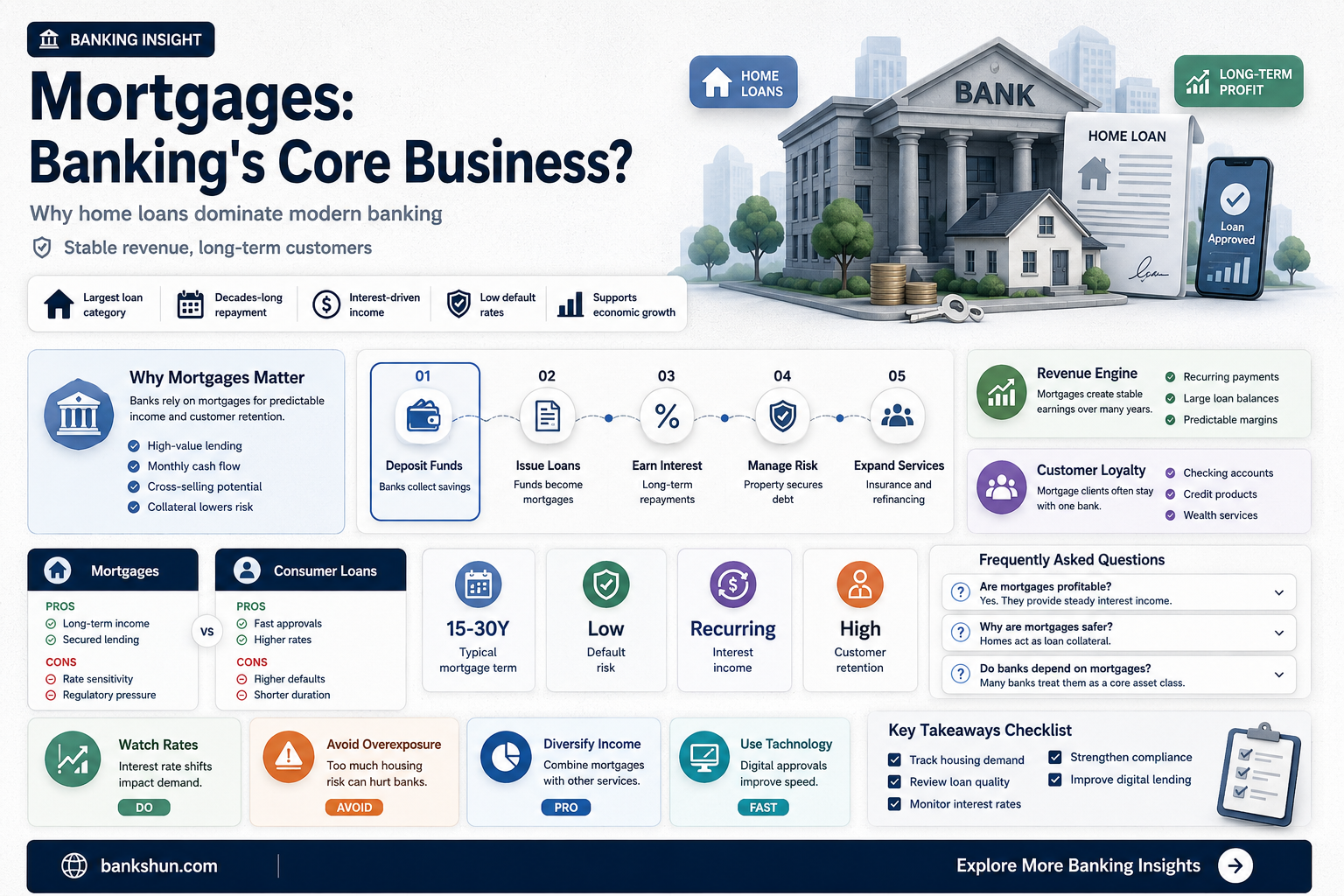

The mortgage industry is a major financial sector that is deeply interconnected with the banking industry. Mortgage bankers are individuals or institutions that originate mortgages using their own funds or funds borrowed from warehouse lenders. They can then sell the loan or retain it in their portfolio. Banks can also engage in mortgage banking by originating, purchasing, and selling loans through the secondary mortgage market. The demand for mortgage services is driven by home sales and refinancing during low mortgage rates. The US mortgage banking industry comprises about 15,000 establishments, generating around $91 billion in annual revenue.

| Characteristics | Values |

|---|---|

| Nature of the relationship between mortgages and the banking industry | Banks and mortgage companies are interconnected. Banks are an important source of funding for mortgage companies. |

| Mortgage companies' reliance on banks | Mortgage companies rely on banks for funding due to their access to deposits and liquidity facilities. |

| Regulatory environment | Banks are more heavily regulated than mortgage companies and are subject to disclosure requirements. |

| Role of banks in the mortgage process | Banks are typically involved in the mortgage origination process as underwriters and may also sell or retain mortgages they originate. |

| Mortgage banking industry in the US | The US mortgage banking industry includes about 15,000 establishments, with a combined annual revenue of about $91 billion. |

| Mortgage bankers | Mortgage bankers are individuals or institutions that originate mortgages using their own funds or those of their institutions. They work with loan applicants throughout the mortgage process and advise them on loan options. |

| Mortgage brokers | Mortgage brokers facilitate loan originations for financial institutions and are required to disclose additional fees charged to consumers under federal and state laws. |

| Impact of regulations | Post-crisis regulations have led to a shift in mortgage originations from banks to non-bank institutions. |

| Government involvement | The federal government has created programs to encourage mortgage lending and home ownership, including the Government National Mortgage Association (Ginnie Mae) and the Federal National Mortgage Association (Fannie Mae). |

| Predatory lending concerns | There are concerns about predatory mortgage lending in the US, where lenders may exploit loopholes to increase profits at the expense of borrowers. |

Explore related products

What You'll Learn

![]()

Banks and mortgage companies are interconnected

Secondly, mortgage companies and banks are interconnected through the buying and selling of mortgages. Mortgage companies often sell the mortgages they originate to investors, including other financial institutions and banks. Banks engaged in mortgage banking may purchase these mortgages or participate in the secondary mortgage market by buying and selling loans. Securitization allows banks to quickly relend money, creating more mortgages than their deposits alone would allow. This process involves pooling mortgages into securities, known as mortgage-backed securities (MBS), and selling them to investors at lower interest rates.

Additionally, banks and mortgage companies are interconnected through the mortgage origination process. Mortgage bankers, who work for financial institutions like banks, play a key role in originating mortgages. They evaluate properties, collect financial information, and advise loan applicants throughout the mortgage process. Mortgage brokers, on the other hand, facilitate originations for other institutions by connecting borrowers with lenders. The underwriter, typically a bank, receives the loan application and documentation to determine whether the loan can be accepted.

The interconnectedness between banks and mortgage companies also extends to regulatory frameworks. Mortgage bankers and brokers must comply with federal and state laws regarding disclosures and fees. Banks, being more heavily regulated than mortgage companies, are required to publicly disclose detailed financial information. Regulatory changes can impact both industries, as seen in the post-2008 era, where many bank-like activities shifted to the less-regulated private credit market.

In summary, banks and mortgage companies are interconnected through funding arrangements, the buying and selling of mortgages, the mortgage origination process, and regulatory frameworks. This interconnectedness has implications for the housing market, the availability of credit, and the broader economy.

Mortgages During COVID-19: Are Banks Still Lending?

You may want to see also

Explore related products

![]()

Mortgage banking and loan originations

The mortgage industry is a major financial sector, with mortgage banking being a key component. Mortgage banking involves loan originations, as well as the purchase and sale of loans through the secondary mortgage market. Banks engaged in mortgage banking may choose to retain or sell the loans they originate or purchase, and they can also choose to sell or retain the servicing rights to these loans.

Loan origination is a critical aspect of the mortgage process. It involves the evaluation and underwriting of loan applications, where underwriters assess the risk and decide whether to approve or decline the loan. The process can be time-consuming and stressful for borrowers, so preparation is essential. Applicants should be ready to provide proof of income, tax returns, and financial documentation.

Mortgage loan originations are closely linked to the state of the housing industry and home sales. High origination volumes indicate a robust housing market, as seen in 2021 when record-low rates fuelled a surge in buying activity. Conversely, lower origination projections, such as those for 2025, suggest a sluggish housing market due to high mortgage rates and economic uncertainty.

The interconnectedness between banks and mortgage companies is significant. While mortgage originations are no longer dominated by banks, mortgage companies rely heavily on bank funding due to their lack of deposits and access to liquidity facilities. This dynamic ensures that banks remain crucial to the housing market and play a vital role in supporting housing affordability.

Regulatory changes and post-crisis measures have led to a shift in the mortgage landscape. Non-bank entities have gained market share in mortgage originations, and the emergence of the private credit market has resulted in bank-like activities migrating to less-regulated environments. Despite these changes, the mortgage industry continues to be a dynamic and influential sector, with banks still playing a pivotal role in facilitating homeownership.

Non-Bank Financial Institutions: What Are They?

You may want to see also

Explore related products

![]()

Mortgages and housing affordability

The mortgage industry is a major financial sector in the United States. Banks play a crucial role in the mortgage market, either directly through mortgage originations or indirectly by providing funding to mortgage companies. While the share of direct mortgage originations by banks has decreased after the 2008 financial crisis, with non-bank entities taking a larger share, banks remain interconnected with mortgage companies and are still key players in the housing market.

Mortgage banking involves loan originations, as well as the purchase and sale of loans through the secondary mortgage market. Banks engaged in mortgage banking can choose to retain or sell the loans they originate or purchase. Securitization allows banks to quickly relend money and create more mortgages than they could with their deposits alone.

Housing affordability is a significant concern, and banks' access to the Federal Home Loan Banks' facilities is essential to maintaining affordability. The Federal Government has also created programs, such as the Government National Mortgage Association (Ginnie Mae) and the Federal National Mortgage Association (Fannie Mae), to promote mortgage lending and homeownership.

To assess housing affordability, tools like the Housing Affordability Index (HAI) are used to determine whether a typical family can qualify for a mortgage loan on a typical home. This index uses income and price data to provide a reference for affordability at the national and regional levels. Additionally, individuals can use mortgage affordability calculators to estimate how much they can afford to borrow based on their income, debt, down payment, and location.

When considering a mortgage, it is important to be aware of the additional costs associated with homeownership. These can include closing costs, moving costs, changes in monthly expenses, maintenance, and unexpected expenses. It is recommended to follow guidelines such as the 28/36 rule, which suggests that housing costs should not exceed 28% of annual gross income, and total debt, including housing, should not be more than 36% of annual income.

Math 1 Scores: Are They Banked in North Carolina?

You may want to see also

Explore related products

![]()

Mortgage lending and regulations

Mortgage lending is a critical component of the banking industry, with banks playing a significant role in the housing market. Banks engage in mortgage banking by originating, retaining, and selling loans through the secondary mortgage market. They also provide funding for mortgage companies, which rely heavily on banks due to their access to liquidity facilities.

Mortgage lending is subject to various regulations at both the federal and state levels in the United States. These regulations aim to protect consumers, ensure fair lending practices, and promote financial stability. Some key regulations include:

- The Truth in Lending Act (TILA) and Regulation Z: This regulation requires lenders to provide clear and accurate information about loan terms, including interest rates and fees.

- The Real Estate Settlement Procedures Act (RESPA) and Regulation X: RESPA ensures that consumers receive detailed information about the settlement process and protects them from unnecessarily high settlement charges.

- The Fair Housing Act (FHA): The FHA prohibits discrimination in the sale, rental, and financing of housing based on race, colour, national origin, religion, sex, familial status, and disability.

- The Equal Credit Opportunity Act (ECOA): ECOA prohibits credit discrimination based on race, colour, religion, national origin, sex, marital status, age, or because an individual receives public assistance.

- The Fair Credit Reporting Act (FCRA): FCRA promotes the accuracy, fairness, and privacy of consumer information contained in credit reports.

- Ability-to-Repay/Qualified Mortgage (ATR/QM) Rule: This rule protects consumers from taking on mortgages they cannot afford by requiring lenders to make a reasonable, good-faith determination of a borrower's ability to repay.

These regulations are essential to maintain a fair and stable mortgage lending environment, protecting both consumers and financial institutions. Non-compliance can lead to significant risks and reputational damage for lenders and adverse financial consequences for borrowers.

Discover Bank Headquarters: Address and Location

You may want to see also

Explore related products

$16.53 $22.99

![]()

Mortgage bankers and brokers

The choice between working with a mortgage broker or directly with a bank depends on an individual's financial situation and preferences. Working with a mortgage broker can be more convenient, especially for those who may have trouble qualifying for a mortgage, as brokers can streamline the process and offer a broader range of options. In contrast, going directly through a bank gives the borrower more control over the homebuying process and may result in cost savings.

Mortgage bankers play a crucial role in the mortgage process. They work closely with realtors and borrowers, guiding them through the entire process. This includes evaluating the property, collecting financial information, and securing the loan. Mortgage bankers can also act as advisors to borrowers, helping them choose the most suitable mortgage product for their needs. They have the authority to approve or deny loan requests and originate the mortgage to facilitate funding for the borrower.

Mortgage brokers also have an important role in the mortgage industry. They assist individuals in navigating the complex process of securing a home loan. Mortgage brokers work with a network of lenders, including banks and other financial institutions, to find the best loan options for their clients. They help borrowers understand their financial situation and gather the necessary documentation, including financial and credit history. By utilising their industry knowledge and relationships, mortgage brokers can streamline the process and improve the chances of a successful loan approval.

The interconnectedness between banks and mortgage companies highlights the significance of the banking industry in the housing market. Banks provide funding for mortgage companies, and regulatory changes can impact the dynamics between banks and non-bank mortgage providers. While direct mortgage originations may no longer be dominated by banks, their involvement in the mortgage market remains crucial.

How Do Shutdowns Affect the Federal Reserve Banks?

You may want to see also

Frequently asked questions

A mortgage banker is a company, individual, or institution that originates mortgages. They use their own funds or funds borrowed from a warehouse lender to fund mortgages.

Mortgage bankers use their own funds, whereas mortgage brokers facilitate originations for other institutions. Mortgage bankers close loans in their names, while mortgage brokers do so in the name of financial institutions.

Mortgage banking is a part of the banking industry. Mortgage banks provide loans to clients purchasing real estate properties. Banks engaged in mortgage banking may retain or sell the loans they originate or purchase.

Banks are important to the housing market. They are involved in originating or servicing mortgage loans, or both. Banks also receive applications and documentation from borrowers and determine whether the loan can be accepted.