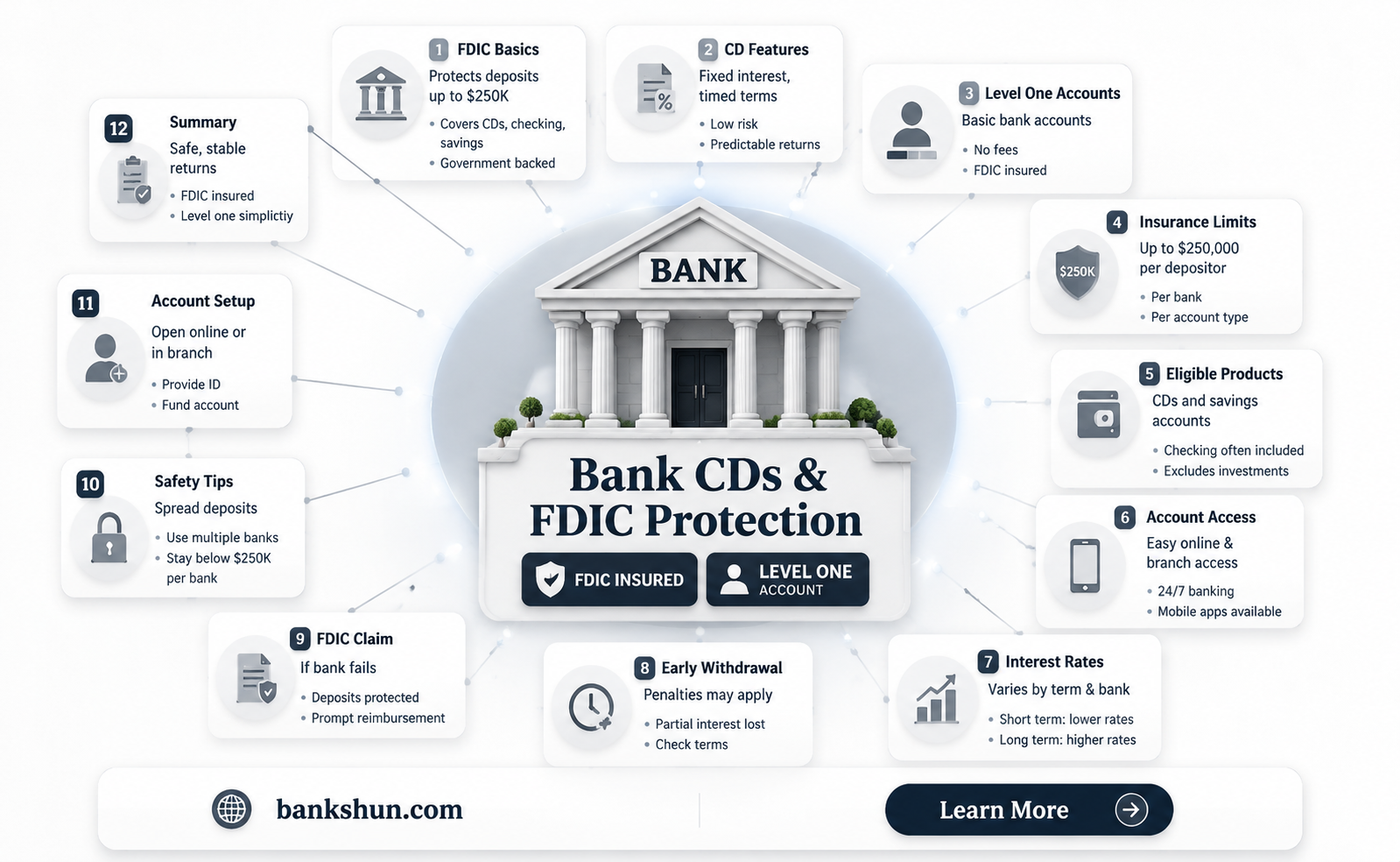

Certificates of Deposit (CDs) are a low-risk alternative to traditional savings accounts. They generally pay higher interest rates in exchange for time-based restrictions on accessing your money. Most CD accounts are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency that provides deposit insurance and maintains the safety of the US banking system. The FDIC insures deposits up to $250,000 per depositor, per FDIC-insured bank, per ownership category. Thus, CDs are a safe option for those looking to save money in the short term.

| Characteristics | Values |

|---|---|

| What is FDIC? | The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. |

| What does FDIC cover? | FDIC deposit insurance covers checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). |

| What is the insurance limit? | The insurance limit is USD 250,000 per depositor, per FDIC-insured bank, per ownership category. |

| How is the insurance limit calculated? | The FDIC adds together all the deposit accounts held in the same ownership category at the same bank, regardless of the deposit type. |

| What happens in the event of a bank failure? | The FDIC acts quickly to ensure that all depositors get prompt access to their insured deposits. It either provides each depositor with a new account at another insured bank or issues a check for the insured balance. |

| Are there any exceptions to FDIC coverage? | Yes, some exceptions include uninsured CDs, deposits that exceed the insurance limit, and deposits established by a third-party broker. |

| How can I calculate my specific insurance coverage? | You can use the Electronic Deposit Insurance Estimator (EDIE) on the FDIC's website to calculate your specific insurance coverage amount. |

Explore related products

What You'll Learn

- CDs are insured by the Federal Deposit Insurance Corporation (FDIC)

- FDIC insurance covers up to $250,000 per depositor, per bank

- FDIC insurance is automatic for deposit accounts at insured banks

- FDIC insurance covers joint accounts up to $500,000

- The National Credit Union Administration (NCUA) insures CDs for credit union customers

![]()

CDs are insured by the Federal Deposit Insurance Corporation (FDIC)

Certificates of deposit (CDs) are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency of the United States government. The FDIC protects bank customers in the event that an FDIC-insured bank or savings association fails. FDIC insurance is automatic for any deposit account opened at an FDIC-insured bank, and deposits are insured up to at least $250,000 per depositor, per FDIC-insured bank, and per ownership category. This limit applies to the total of all deposits that an account holder has at a single bank, and it includes principal and any interest accrued or due to the depositor through the date of default. For example, if a customer had a CD account in her name alone with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

The FDIC covers a range of deposit products, including checking accounts, savings accounts, money market deposit accounts (MMDAs), and CDs. It's important to note that FDIC insurance only applies to certain deposit products, and some financial products and services offered by banks are not deposits and are not insured by the FDIC. Additionally, there are exceptions to CD accounts being insured. Some types of CDs, such as those held in foreign banks or purchased through a non-bank institution like a brokerage firm, may not carry FDIC insurance.

To determine if a bank is FDIC-insured, individuals can ask a bank representative, look for the FDIC sign at the bank, or use the FDIC's BankFind tool, which provides detailed information about FDIC-insured institutions. While CDs are insured by the FDIC, it's important to understand the terms and conditions of different CD accounts, as some may be uninsured, depending on the financial institution offering them.

Explore the Diverse Roles in Banking

You may want to see also

Explore related products

![]()

FDIC insurance covers up to $250,000 per depositor, per bank

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance covers up to $250,000 per depositor, per FDIC-insured bank, per ownership category.

The FDIC only insures your money if it is in a deposit account at an FDIC-insured bank. Banks offer some financial products and services that are not deposits, and the FDIC does not insure them. These include large and small banks across the country that offer deposit accounts backed by FDIC deposit insurance. Coverage is automatic when you open one of these types of accounts at an FDIC-insured bank.

Deposit insurance is calculated dollar-for-dollar, including principal and any accrued interest through the date of the insured bank's failure, up to the insurance limit. For example, if a customer had a CD account in her name alone with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

If you have accounts at different FDIC-insured banks, the limit applies at each bank: $250,000 per depositor for each account ownership category. You can calculate your specific insurance coverage amount using the Electronic Deposit Insurance Estimator (EDIE), a calculator that is available on the FDIC’s website.

In the unlikely event of a bank failure, the FDIC acts quickly to ensure that all depositors get prompt access to their insured deposits. Historically, the FDIC pays insurance within a few days after a bank closing, usually the next business day, by either providing each depositor with a new account at another insured bank in an amount equal to the insured balance of their account at the failed bank, or issuing a check to each depositor for the insured balance of their account at the failed bank.

Transfer Apple Cash to Your Bank: A Simple Guide

You may want to see also

Explore related products

![]()

FDIC insurance is automatic for deposit accounts at insured banks

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. FDIC insurance covers traditional deposit accounts, and depositors do not need to apply for it. FDIC deposit insurance is automatic for any deposit account opened at an FDIC-insured bank.

The FDIC covers the money you hold at an FDIC-insured bank in traditional deposit accounts like checking accounts, savings accounts, and money market deposit accounts (MMDAs). Certificates of Deposit (CDs) are also insured by the FDIC. The amount of FDIC insurance coverage you may be entitled to depends on the ownership category. This generally means the manner in which you hold your funds at the bank. FDIC ownership categories include single accounts, certain retirement accounts, employee benefit plan accounts, joint accounts, trust accounts, business accounts, and government accounts. The standard deposit insurance coverage limit is $250,000 per depositor, per FDIC-insured bank, per ownership category.

In the unlikely event of a bank failure, the FDIC responds in two capacities. First, as the insurer of the bank's deposits, the FDIC pays insurance to depositors up to the insurance limit. The FDIC has protected depositors of insured banks located in the United States since 1934, and no depositor has ever lost a penny of FDIC-insured deposits.

Capitalizing on Banking Failures: Strategies for the Savvy Investor

You may want to see also

![]()

FDIC insurance covers joint accounts up to $500,000

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. FDIC insurance covers deposits up to $250,000 per depositor, per FDIC-insured bank, and per ownership category. This limit applies to all deposit accounts, including checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs).

For joint accounts with two owners, the FDIC provides coverage of up to $500,000 in the event of a bank failure. This means that each co-owner's shares of the joint accounts are added together and insured up to $250,000 per owner, resulting in a total coverage of $500,000 for the couple's joint accounts. It is important to note that the FDIC combines all single accounts owned by the same person at the same bank and insures the total up to $250,000.

The FDIC insurance coverage for joint accounts is not affected by rearranging the owners' names, Social Security numbers, or changing the styling of their names. Additionally, the insurance coverage for joint accounts is calculated separately for each owner, and the FDIC assumes that the owners' shares are equal unless the deposit account records state otherwise. It is worth noting that FDIC insurance only applies to deposits and does not cover other financial products and services offered by banks.

While most CD accounts are FDIC-insured, there are exceptions. Some types of CDs, such as those held in foreign banks or purchased through a non-bank institution, may not carry FDIC insurance. It is important to understand all the terms and conditions when considering a CD account and whether it offers FDIC coverage. In the unlikely event of a bank failure, the FDIC responds by paying insurance to depositors up to the insurance limit, typically within a few days after the bank closing.

Are Elizabeth Banks and Rachel McAdams Related?

You may want to see also

![]()

The National Credit Union Administration (NCUA) insures CDs for credit union customers

Certificates of deposit (CDs) are low-risk alternatives to traditional savings accounts. They generally pay higher interest rates in exchange for time-based restrictions on accessing your money. Most CD accounts are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency that provides deposit insurance and maintains the safety of the US banking system. Deposits at FDIC-insured banks are covered up to $250,000 per person per account ownership type.

Similar to the FDIC, the National Credit Union Administration (NCUA) insures CD deposits for credit union customers. The NCUA was created by Congress in 1970 to insure members' deposits in federally-insured credit unions. The NCUA guarantees that you'll receive the money that you're entitled to from your deposit account if your credit union goes under. It guarantees up to $250,000 per person, per institution, per ownership category.

Credit union failure is rare, but if it does happen, and if your credit union is backed by the NCUA, your deposits are protected. The NCUA will send customers a check for the insured balance of their deposits, usually within a few days of a credit union's closing. The NCUA will notify customers via mail if it requires further action to redeem deposits.

If your financial institution offers both insured and uninsured CD accounts, understand all the terms and conditions when comparing interest rates between these options.

How Banks Detect Fake Silver Coins

You may want to see also

Frequently asked questions

Yes, most CDs are FDIC insured.

The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.

The FDIC (Federal Deposit Insurance Corporation) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails.

FDIC deposit insurance covers the balance of each depositor's account, dollar-for-dollar, up to the insurance limit, including principal and any accrued interest through the date of the insured bank's failure.

In the unlikely event of a bank failure, the FDIC acts quickly to ensure that all depositors get prompt access to their insured deposits. The FDIC pays insurance to depositors up to the insurance limit, either by providing each depositor with a new account at another insured bank or by issuing a check for the insured balance.