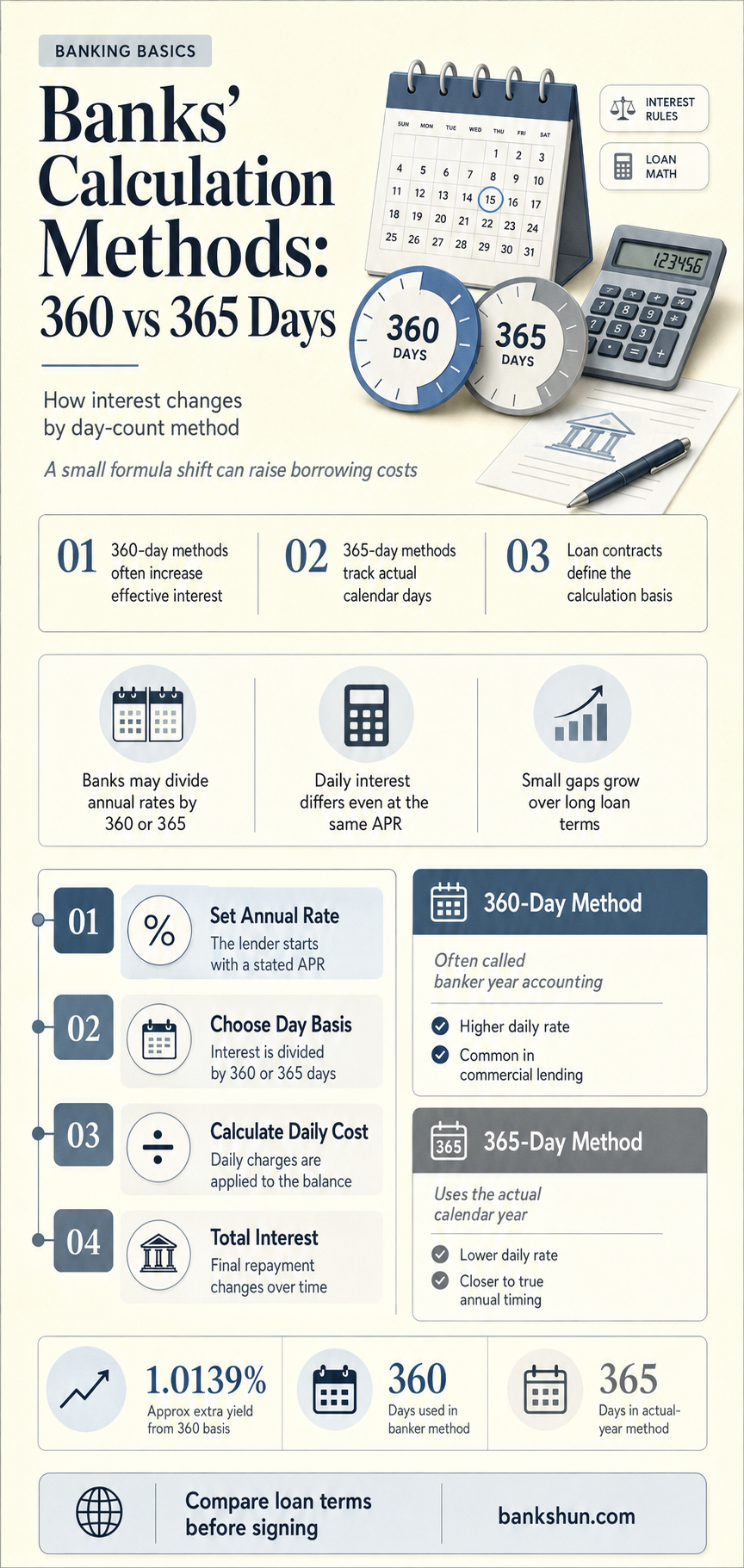

Banks and lenders use different methods to calculate interest accrual on loans, including 30/360, Actual/365, and Actual/360. The 30/360 method is commonly used for consumer transactions like mortgages, while Actual/365 and Actual/360 are used for commercial transactions. The Actual/360 method, also known as the 365/360 rule, is the most prevalent among banks because it results in the most interest paid to them. This method involves dividing the annual interest rate by 360 to obtain a daily interest rate, which is then multiplied by the number of days in the month. In contrast, the Actual/365 method divides the annual interest rate by 365 and then multiplies it by the number of days in the current month. Borrowers should be aware of these different interest accrual methods to understand the real interest rate and the total amount of interest they will pay over the loan term.

| Characteristics | Values |

|---|---|

| Number of day-count conventions | 3 |

| Names of day-count conventions | 30/360, Actual/365, Actual/360 |

| Other names for Actual/365 | 365/365 |

| Other names for Actual/360 | 365/360, Actual/Actual |

| Most commonly used method | Actual/360 |

| Used by | Banks, commercial real estate lenders |

| Used for | Calculating interest accrual, loans |

| Advantage of Actual/365 | Lower daily interest rate |

| Advantage of 30/360 | Borrower pays the least interest |

| Disadvantage of Actual/360 | Borrower pays the most interest |

| Disadvantage of Actual/365 | Borrower pays slightly more interest over the entire year |

Explore related products

What You'll Learn

- Banks use the actual/360 method because it helps standardise daily interest rates

- The actual/360 method results in more interest paid to the bank

- The 30/360 method is used in consumer transactions like mortgages

- The actual/365 method is used in commercial transactions

- The actual/365 method results in slightly higher interest over the entire year

![]()

Banks use the actual/360 method because it helps standardise daily interest rates

The actual/360 method is advantageous to banks as it results in a higher interest amount being paid by the borrower. This is because the daily interest rate is higher than the actual/365 method. The borrower ends up paying a slightly higher amount of interest over the whole year since some months have 31 days instead of 30. This difference in the number of days in a month results in a variation of several thousand dollars in the interest paid, even though the loan amount and the initial interest rate are the same.

The actual/360 method has been challenged in court by borrowers who claim that it is deceptive and hides the true cost of borrowing. However, the lenders have prevailed in these cases as they disclosed the method used to calculate the interest. The actual/360 method is, therefore, a common and accepted method used by banks to calculate interest accrual and standardise daily interest rates.

The actual/360 method is just one of the several methods used by banks to calculate interest. Other methods include the 30/360 method and the actual/365 method. The 30/360 method assumes that each month has 30 days and a year has 360 days. This method is commonly used in bond markets and results in the lowest total interest, making it the most borrower-friendly option. The actual/365 method, on the other hand, uses a lower daily interest rate, which can make monthly payments easier for borrowers. However, over the entire loan term, the borrower ends up paying slightly higher overall costs.

Who Owns FaZe? Banks' Role Explained

You may want to see also

Explore related products

![]()

The actual/360 method results in more interest paid to the bank

Banks use different methods to calculate the interest accrued on loans. The three most common methods are 30/360, Actual/365, and Actual/360. The actual number of days in a year is 365, or 366 during a leap year. However, the 30/360 method assumes that there are 360 days in a year and 30 days in each month. This method is mostly used in consumer transactions, such as mortgages, and results in the least amount of interest paid by the borrower over the life of the loan.

The Actual/365 method calculates the interest accrued by dividing the annual interest rate by 365 to get the daily rate, which is then multiplied by the actual number of days in the month. This method results in a slightly higher amount of interest paid over the entire year since some months have 31 days.

The Actual/360 method, also known as the 365/360 rule, is the most commonly used method by banks to calculate interest accrual. It involves dividing the annual interest rate by 360 to get a daily interest rate, which is then multiplied by the number of days in the month. This method results in a larger dollar amount of interest paid by the borrower because dividing the annual rate by 360 creates a larger daily rate than dividing it by 365 or 366 during a leap year.

The Actual/360 method has been challenged in court by borrowers who argue that it is deceptive and hides the true cost of borrowing. However, banks have prevailed in these cases because the interest calculation method was disclosed. Banks are for-profit institutions and have an incentive to use the Actual/360 method because it results in the most interest paid to them. This method has the highest daily accrual rate because the annual interest rate is divided by 360, and it has the highest monthly accrual amount because it is accrued over the actual number of days in the month. Therefore, the borrower ends up paying the most interest over the entire term of the loan compared to the other methods.

East Bank Club: Classes for All Members

You may want to see also

Explore related products

![]()

The 30/360 method is used in consumer transactions like mortgages

Banks and lenders use different methods to calculate the interest accrued on loans, including the 30/360, Actual/360, and Actual/365 methods. The 30/360 method is typically used in consumer transactions, such as mortgages, while the Actual/365 and Actual/360 methods are more common in commercial transactions.

The 30/360 method is a straightforward process for calculating the accrued interest on a loan. First, the annual interest rate is divided by 360 to obtain the daily accrual rate. For example, if the annual interest rate is 4%, the daily accrual rate would be 0.011% (4% / 360 = 0.011%). Next, the daily accrual rate is multiplied by 30 to calculate the monthly accrual rate (0.011% * 30 = 0.333%). Finally, the monthly accrual rate is multiplied by the outstanding balance to determine the monthly interest accrual amount. For instance, if the outstanding balance is $2,500,000, the monthly interest accrual would be $8,333.33 (2,500,000 * 0.333% = $8,333.33).

The 30/360 method assumes that there are 360 days in a year and 30 days in each month, resulting in a true interest rate. This method is advantageous for borrowers as it typically results in the lowest total interest paid compared to the other methods. For example, if a borrower takes out a $1,000,000 loan at 4% interest for 10 years, they will pay the least amount of interest with the 30/360 method.

While the differences between the 30/360 method and the Actual/365 method may seem minor, they can lead to significant variations in the total interest paid over the life of the loan. This is because the Actual/365 method considers the actual number of days in a month, including months with 31 days. As a result, borrowers may end up paying slightly more interest over the entire year, even though the daily interest rate is lower.

It is important for borrowers to be aware of the interest accrual methodology used in their loan transactions. Understanding the different methods can help borrowers make informed decisions and choose the loan option that best suits their needs. Additionally, borrowers should carefully review the loan documentation to explicitly understand how the interest will be calculated.

Citibank Branches: Tennessee Locations

You may want to see also

Explore related products

![]()

The actual/365 method is used in commercial transactions

Banks and lenders use different methods to calculate interest accrual on loans. The actual/365 method is one of the most common methods used in commercial transactions.

The actual/365 method, also known as 365/365, is used to calculate the interest accrued on a loan by taking the annual interest rate and dividing it by 365, which represents the number of days in a typical year. This results in a daily interest rate, which is then multiplied by the number of days in the current month. This method can be applied to any month, including February, which has 28 days.

Using the actual/365 method results in a slightly higher amount of interest paid over the entire year compared to the 30/360 method. This is because, although the daily interest rate is smaller when divided by 365, multiplying it by the actual number of days in a month (which can be up to 31 days) leads to a slightly higher overall interest payment.

The actual/365 method is particularly relevant in commercial real estate transactions. Commercial real estate lenders commonly calculate loans using three methods: 30/360, actual/365, and actual/360. Real estate professionals need to understand these methods to determine the real interest rate and the total amount of interest paid over the loan term.

It is important for borrowers to be aware of the interest accrual methodology used in their loan transactions. Understanding the different methods can help borrowers save money and make informed decisions when taking out loans.

Bank Fraud and Tax Evasion: Criminal Finances Exposed

You may want to see also

Explore related products

![]()

The actual/365 method results in slightly higher interest over the entire year

The actual number of days in a year is 365, or 366 during a leap year. However, the 30/360 method is used to calculate the interest rate for certain loans, particularly in consumer transactions like mortgages. This method assumes there are 360 days in a year and 30 days in each month.

The actual/365 method, also known as the 365/365 method, is calculated by taking the annual interest rate and dividing it by 365, then multiplying that number by the number of days in the current month. For example, if the annual interest rate is 4%, dividing it by 365 gives 0.0110%. Multiplying this by 28 (the number of days in February, excluding leap years) gives 0.307%.

Using the actual/365 method results in a slightly higher interest rate over the entire year compared to the 30/360 method. This is because, although the daily interest rate is smaller, it is multiplied by the actual number of days in each month, which can be up to 31. In contrast, the 30/360 method assumes every month has 30 days, so interest is only accrued for 30 days each month, even in months with 31 days.

The actual/365 method is used in commercial transactions, and it is important for borrowers to be aware of the interest accrual methodology used in their loan transactions. The differences in interest accrual methods can result in variations of several thousand dollars in interest paid over the term of a loan.

MCAT Question Banks: Are Next Step Worth It?

You may want to see also

Frequently asked questions

These are different day count conventions used by lenders to calculate interest and loans in order to measure risk and the potential return on investment.

The annual interest rate is divided by 360 to get the daily interest rate, which is then multiplied by 30 for a monthly rate.

The annual interest rate is divided by 365 to get the daily interest rate, which is then multiplied by the number of days in the month.

The annual interest rate is divided by 360 to get a daily interest rate. That number is then multiplied by the number of days in the month.

Banks use the Actual/360 method because it helps standardise daily interest rates throughout the year and results in the most interest paid to them.