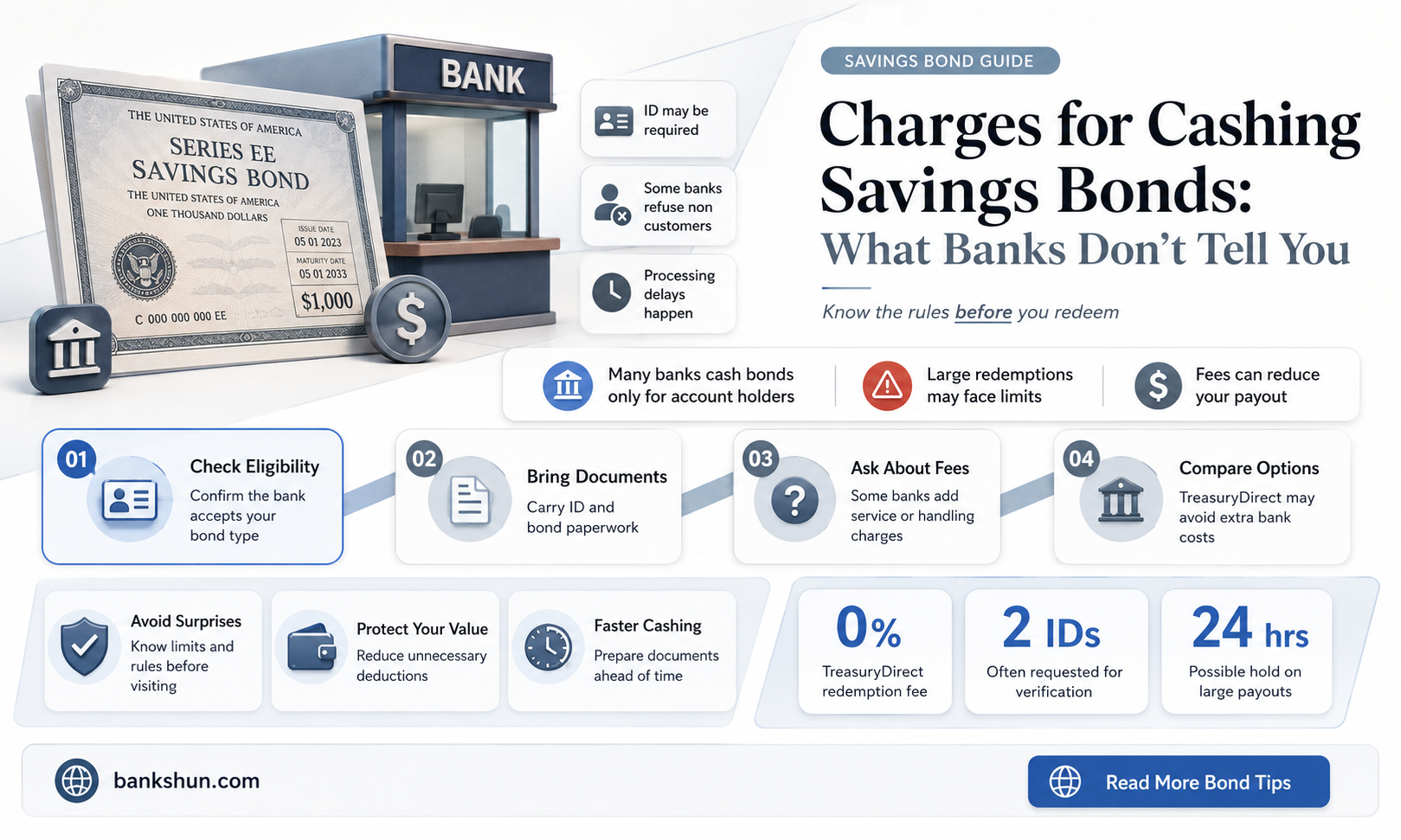

Savings bonds are a low-risk way to save money, and federal law prohibits banks from charging fees to customers for cashing in savings bonds. However, customers may have to pay penalties if they cash the bond before the fifth anniversary of its purchase. There are different types of savings bonds, such as Series E/EE, Series I, and Series H/HH, and they can be purchased electronically or as paper bonds. To cash a savings bond, individuals typically need to present valid identification and may also need to provide additional documentation if the bond does not list their current name.

| Characteristics | Values |

|---|---|

| Fee charged by banks to customers for cashing savings bonds | Federal law prohibits banks from charging fees to customers for cashing savings bonds |

| Penalty for cashing savings bonds too early | If savings bonds are cashed in before the fifth anniversary of their purchase, the bank withholds the last three months of interest |

| Minimum age of savings bonds for cashing | Banks may not cash savings bonds for customers if the bond is less than one year old or, in the case of bonds issued before February 2003, less than six months old |

| Documents required for cashing savings bonds | Photo identification, proof of name change, death certificate (if the beneficiary of the bond is deceased), FS Form 1522 |

Explore related products

What You'll Learn

- Banks cannot charge fees for cashing in savings bonds

- Cashing in a savings bond before the fifth anniversary incurs a penalty

- Paper savings bonds require photo identification to be cashed

- Electronic savings bonds can be cashed without visiting a bank

- Savings bonds can be cashed by non-account holders at some banks

![]()

Banks cannot charge fees for cashing in savings bonds

If you are cashing in a paper savings bond, you will need to take it to the bank, along with photo identification. The name on your ID must match the name on the bond. If your name has legally changed since receiving the bond, you will need to endorse the bond with both your old and new names. If your new name differs significantly from your original name, the teller may not be able to cash it. In this case, you may need to send proof of your identity to the Federal Reserve Board.

If you are cashing a bond for a child under 18, you will need to write your name and "parent of" the child's name. You will also need to show ID to the teller at the bank. The teller will then cash the bond and stamp it so that it cannot be cashed again.

There are also electronic savings bonds available, which can be cashed without visiting a physical bank. These can be cashed via the Treasury Direct website, with the money deposited into your bank account.

US Banking Giant: Who's Leading the Pack?

You may want to see also

Explore related products

![]()

Cashing in a savings bond before the fifth anniversary incurs a penalty

Savings bonds are a great, low-risk way to save money. They are debt securities distributed and backed by the US government. Federal law prohibits banks from charging fees to customers for cashing in savings bonds. However, customers may have to pay penalties if they cash the bond in too early. Banks must pay a fee to the Federal Reserve Board for each treasury bond they cash within a calendar month.

If you cash in a savings bond before the fifth anniversary of its purchase, you must pay a penalty for cashing in the bond too early. In this case, the bank withholds the last three months of interest when it cashes in your savings bond. For example, if you redeem a bond after 24 months, you will only receive 21 months of interest. There's no penalty if you simply hold onto the bond after five years, and there's value in holding onto most bonds. The longer they mature, the more interest they earn.

There are two types of savings bonds: Series EE and Series I bonds. Series EE bonds double in value if held for at least 20 years, while I bonds keep pace with inflation. Both types of bonds are typically seen as long-term investments. You can cash in a bond after holding it for at least one year, but penalties kick in if you redeem a savings bond within five years of buying it.

To cash in a paper savings bond, you should take it to the bank along with your photo identification. The name on your ID must match the name on the bond. If you have legally changed your name since receiving the bond, endorse the bond with both names. If your new name is substantially different from your original name, the teller may not be able to cash it. In these cases, you may have to send proof of your identity to the Federal Reserve Board.

Bank Balance: Pending Transactions Included or Not?

You may want to see also

Explore related products

![]()

Paper savings bonds require photo identification to be cashed

Federal law prohibits banks from charging fees to customers for cashing in savings bonds. However, customers may have to pay penalties if they cash the bond in too early. Banks must pay a fee to the Federal Reserve Board for each treasury bond they cash within a calendar month.

Paper savings bonds can be cashed in after a year of purchase, but they accrue maximum value after 20 years. If you cash in a savings bond before its fifth anniversary, you must pay a penalty in the form of losing the last three months of interest.

To cash a paper savings bond, you must present it at a bank along with a photo identification. The name on the ID must match the name on the bond. If you have legally changed your name since receiving the bond, endorse the bond with both names. If your new name is substantially different from your original name, the teller may not be able to cash it. In this case, you may have to send proof of your identity to the Federal Reserve Board.

If you are cashing a bond for a child under the age of 18, write your name and "parent of" the child's name. For example, "John Smith, parent of Jack Smith." Show your ID to the teller at the bank, and they will cash it for you.

Direct Express: Which Bank is Behind the Card?

You may want to see also

Explore related products

![]()

Electronic savings bonds can be cashed without visiting a bank

Federal law prohibits banks from charging fees to customers for cashing in savings bonds. However, customers may have to pay penalties if they cash the bond in too early. Banks must pay a fee to the Federal Reserve Board for each treasury bond they cash within a calendar month.

If you have a paper E/EE or I bond, you will need to take a few additional steps. Along with the bond, you will need to provide proof of identity, such as a United States driver's license. You will also need to partner with a notary to notarize and certify your signature on an unsigned FS Form 1522 and send it to your local bank or credit union. After completing these steps, you can send the unsigned bonds along with the signed FS Form 1522 and supporting legal evidence or other documentation to show you are entitled to cash the bond to the U.S. Department of the Treasury.

It is important to note that you can only cash in bonds that you own or co-own. If you have legally changed your name since receiving the bond, you may need to send proof of your identity to the Federal Reserve Board. Additionally, there are different types of savings bonds available, such as Series E/EE, Series I, or Series H/HH, each with its own characteristics in terms of interest rates and maturity periods.

Initiating a Food Bank: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Savings bonds can be cashed by non-account holders at some banks

Savings bonds are a great, low-risk way to save money. They are debt securities distributed and backed by the US government. The federal government issues two types of savings bonds: Series EE and Series I bonds. Series EE bonds double in value if held for at least 20 years, while Series I bonds keep pace with inflation.

Savings bonds can be cashed at a bank or credit union, but some financial institutions may not cash savings bonds for non-customers or new customers. It is recommended that a customer be established for 12 months before cashing bonds at a financial institution. Some banks may also only cash in small amounts. If you have a paper E/EE or I bond, you will need to provide proof of identity, such as a US driver's license, and partner with a notary to notarize and certify your signature on an unsigned FS Form 1522. If you are cashing a bond for a child under the age of 18, you will need to write your name and "parent of" the child's name, and show your ID to the teller at the bank.

If you want to cash a paper savings bond, you should take it to the bank along with your photo identification. The name on your ID must match the name on the bond. If your name has legally changed since receiving the bond, endorse the bond with both names. If your new name is substantially different from your original name, the teller may not be able to cash it, and you may have to send proof of your identity to the Federal Reserve Board. Banks may not cash savings bonds for customers if the bond is less than one year old or, in the case of bonds issued before February 2003, less than six months old.

There are also electronic savings bonds available that eliminate the need to go to a physical bank for redemption. To cash these bonds, you can use the Treasury Direct website and have the money put into your bank account. You can also purchase bonds electronically at TreasuryDirect.gov, the US Treasury's electronic savings portfolio platform.

Federal law prohibits banks from charging fees to customers for cashing in savings bonds, although customers may have to pay penalties if they cash the bond in too early. If you cash in a savings bond before the fifth anniversary of its purchase, you must pay a penalty for cashing it in too early. In this case, the bank must withhold the last three months of interest when it cashes in your savings bond.

Bank Jobs: Recession-Proof or Not?

You may want to see also

Frequently asked questions

No, federal law prohibits banks from charging fees to customers if they cash treasury bonds at the bank. Banks must pay a fee to the Federal Reserve Board for each treasury bond cashed within a calendar month.

If you have a paper E/EE or I bond, you need to provide proof of identity, such as a driver's license, and partner with a notary to notarize and certify your signature on an unsigned FS Form 1522. You can then send the unsigned bond along with the signed form to the US Department of the Treasury. If you have an electronic savings bond, log in to your TreasuryDirect account and use the link for cashing securities in ManageDirect.

Yes, if you cash in a savings bond before its fifth anniversary, you must pay a penalty. In this case, the bank withholds the last three months of interest.

There are Series E/EE, Series I, and Series H/HH bonds. Series E/EE bonds earn a fixed rate of interest for up to 30 years, while Series I bonds earn interest based on combining a fixed rate and an inflation rate. Series H/HH bonds are different in that you receive interest payments every six months until maturity or redemption.