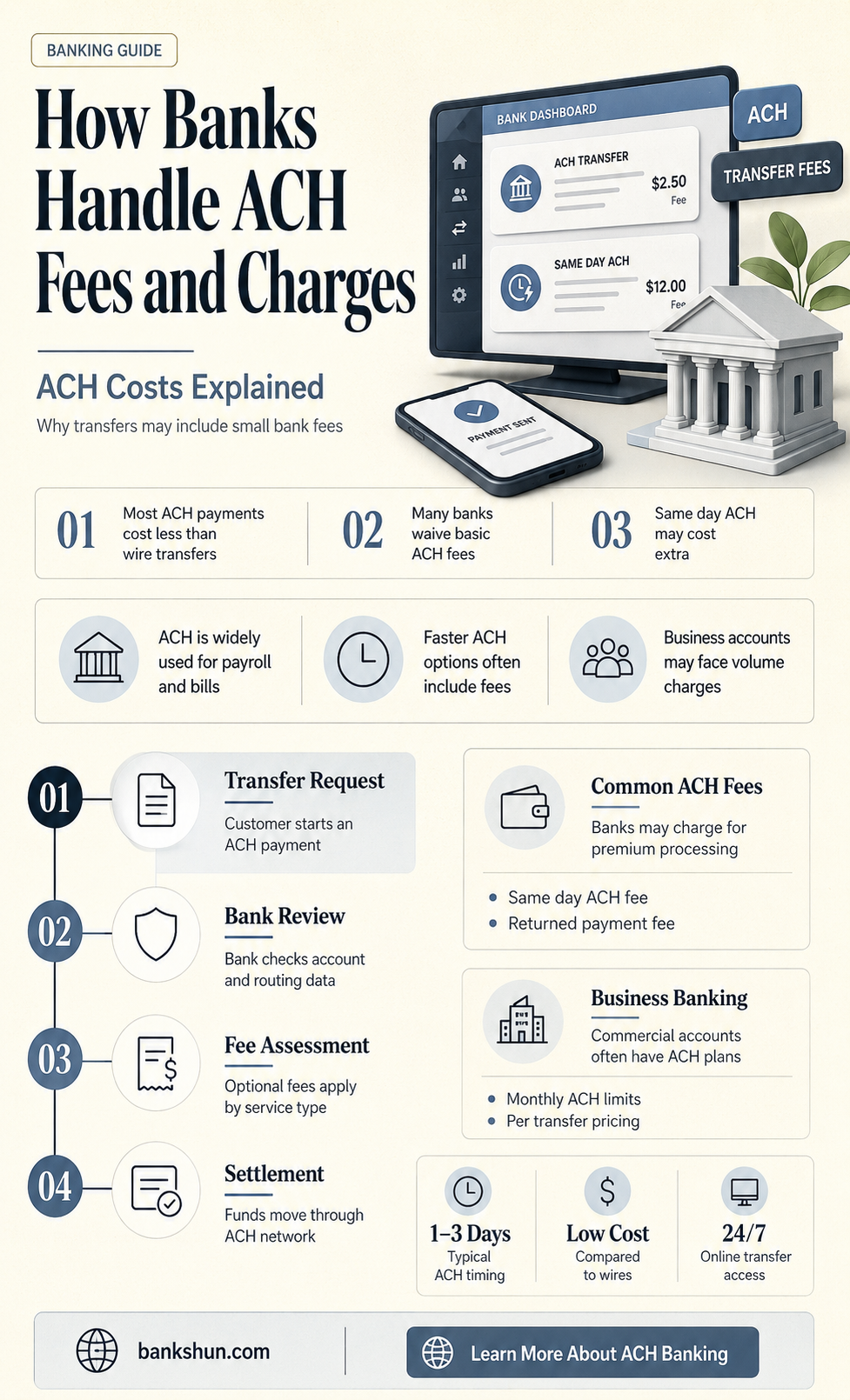

ACH, or Automated Clearing House, is a centralized US financial network that allows banks and credit unions to send and receive electronic payments and money transfers. ACH transfers are generally considered a cheap way to move money, with costs ranging from $0 to $10. However, banks may charge their customers a fee for sending ACH payments, which can be around $3 for sending money between accounts at different banks. On the other hand, banks rarely charge for receiving incoming ACH payments, such as paychecks or tax refunds, though they may choose to pass on the annual fee charged by the ACH payment system for receiving ACH payments.

| Characteristics | Values |

|---|---|

| ACH fee charged by banks | Varies by bank; some banks charge a fee of around $3 for sending money between accounts at different banks, while others offer external funds transfers for free. ACH fees can range between $0 and $10. |

| Fee for receiving ACH transfers | There is usually no fee for receiving ACH transfers. |

| Fee for ACH transfer services | The ACH payment system charges an annual fee to participating banks and credit unions for sending and receiving ACH payments, as well as a fee per transaction. Banks may or may not pass this cost on to their customers. |

| Other limitations/fees | Amount limits, cutoff times, insufficient funds fee, international transfer restrictions. |

Explore related products

What You'll Learn

![]()

ACH transfers are usually free to receive

ACH transfers are a convenient way to send and receive money between banks and credit unions. The Automated Clearing House (ACH) network facilitates electronic money transfers, making it faster and more efficient for consumers to access their funds. While sending money via ACH may incur fees, receiving ACH transfers is typically free of charge.

ACH transfers are generally free to receive, with no additional costs for the recipient. This applies to various types of ACH payments, including direct deposits, tax refunds, child support payments, and peer-to-peer payments through services like PayPal or Venmo. When you receive your paycheck through direct deposit or pay bills directly from your bank account, you are often utilizing the ACH network.

While receiving ACH transfers is usually free, there may be exceptions depending on the bank or credit union's policies. Some financial institutions might pass on the ACH network's transaction fees to their customers. Therefore, it is always a good idea to check with your specific bank or credit union to understand their ACH policies and any associated fees.

It is worth noting that while receiving ACH transfers is typically free, sending money via ACH can sometimes come with costs. These fees can vary depending on the type of transfer, the amount being sent, and the policies of the sending institution. For example, some banks may charge a fee for outbound ACH transfers or wire transfers, while others may offer external funds transfers for free.

Overall, ACH transfers are a convenient and efficient way to send and receive money, with receiving transfers usually being free of charge. By utilizing the ACH network, individuals can benefit from faster access to funds, direct deposits, and secure and reliable transactions. However, it is always recommended to consult with your financial institution to understand their specific policies and any potential fees associated with ACH transfers.

How Banks Verify Employment: Calling Your Employer?

You may want to see also

Explore related products

![]()

Banks may charge a fee for receiving ACH payments

ACH transfers are electronic money transfers between banks and credit unions through the Automated Clearing House (ACH) network. This network is overseen by the National Automated Clearing House Association (NACHA), a government-run, nonpartisan organization.

ACH transfers are generally considered a cheap way to send and receive money, with fees ranging from free to a few dollars at most. However, some banks may charge higher fees for ACH transfers, so it is important to check with your financial institution to understand their specific policies and limitations. These limitations can include amount limits, cutoff times, fees for insufficient funds, and international transfer restrictions.

While banks may charge a fee for receiving ACH payments, this is not always the case. Some banks, such as Bank of America, have been known to waive fees for inbound ACH transfers while charging a fee for outbound transfers. Ultimately, the decision to charge a fee for receiving ACH payments lies with the individual bank or credit union.

CRA in Banking: What It Stands For and Why It Matters

You may want to see also

Explore related products

![]()

The ACH network charges an annual fee to participating banks

The ACH, or Automated Clearing House, is a network of US-based direct member financial institutions and corporations, including banks, credit unions, corporations, e-commerce companies, and payments technology providers. The ACH network charges an annual fee to participating banks and credit unions for the privilege of sending and receiving ACH payments. On top of this, there is also a fee per transaction.

The fee amounts are set to recover the costs of the ACH Network's administrative functions, which are performed by Nacha, the trade group that oversees the network, on an "at-cost" basis. These functions include risk management, quality improvement, research and development of ACH applications, rules, statistics, communications, advocacy, and the administration of national ACH messaging initiatives. The fee amounts are reviewed and approved by the Nacha Board of Directors annually and are amended as deemed necessary by the Board.

Through the Annual Fee, all depository financial institutions that use the ACH Network contribute a minimum amount to maintain the Nacha Operating Rules, which provide the legal and operational foundation for the ACH Network. The Per-Entry Fee is applied to all commercial and government ACH entries transmitted or received by Participating DFIs, except for "on-us" entries. Depository financial institutions with direct send or "on-we" volume exceeding 5 million entries annually are required to file the requisite reporting with Nacha quarterly. Those with direct send volume below this threshold file with Nacha annually and submit transaction volume data and any associated fees directly to Nacha using form N-7.

It is important to note that banks may or may not choose to pass these costs on to their customers. While some banks charge customers an ACH fee as part of bill-paying services, they typically do not charge for incoming ACH payments such as paychecks. ACH transfers are generally considered a cheap way to move money, with fees ranging from $0 to $10, and are often much lower cost than wire transfer fees.

Gold Bars: Which US Banks Sell Them?

You may want to see also

Explore related products

![]()

ACH transfers are often cheaper than wire transfers

ACH transfers are also generally free for consumers, whereas wire transfers are more expensive. The ACH network charges an annual fee to participating banks and credit unions to send and receive ACH payments, and there is also a fee per transaction. Banks may or may not pass this cost on to their customers.

ACH transfers are a safe, secure, and fast way to move money between banks and credit unions across the Automated Clearing House (ACH) network. They are particularly useful for recurring payments, and they can also be used to access your money quickly. For example, instead of waiting for a paycheck to arrive in the mail and then taking it to the bank, your employer can put the money directly into your account.

While wire transfers are generally faster than ACH transfers, they are also more expensive. If you need to transfer a large amount of money or get it to its destination quickly, a wire transfer is the go-to option. However, ACH transfers are becoming faster and more efficient thanks to new solutions built on old infrastructure.

Coders in Banks: Career Opportunities and Insights

You may want to see also

Explore related products

![]()

Some banks charge customers an ACH fee for bill-paying services

ACH, or Automated Clearing House, is a federally regulated network of financial transactions. It is a secure system that directs money from one bank account to another. ACH payments are electronic payments that are sent via the ACH network, which is a paperless way to send money between bank accounts in the US.

ACH payments are a more cost-effective solution than paying by credit card or cheque. Credit card fees can add up, and cheques can cost $5 or more to process. ACH payments, on the other hand, have a median cost of just $0.29 per transaction, with some sources stating that they can range from $0 to $10.

While some banks charge customers an ACH fee as part of bill-paying services, they almost never charge for incoming ACH payments. ACH payments are also usually free to receive. However, banks may charge a fee of around $3 for sending money between accounts that you have at different banks.

ACH transfers are very safe and follow the latest in financial technology requirements. They are also faster and more efficient than cheques. However, there is a risk of rejection or denial with ACH payments, as with any payment method. For example, a request for an ACH payment may be rejected due to insufficient funds or because the account has been closed.

Fintech Firms: Friend or Foe to Traditional Banks?

You may want to see also

Frequently asked questions

Typically, there is no fee for receiving ACH transfers. However, the bank may choose to pass on the cost of the transaction fee charged by the ACH network.

Banks may charge a fee for sending ACH transfers, typically around $3. However, some banks offer free external funds transfers.

ACH transfers cost a few dollars at most. In contrast, bank wire transfers within the US usually cost between $20 and $30.

ACH transfers initiated by external accounts, also known as ACH pushes, usually incur a fee. However, this varies depending on the bank.

ACH transfers initiated by the account holder, or ACH pulls, are usually free. However, banks may charge a fee for insufficient funds or for expedited transfers.