International payments can be costly, with banks charging a variety of fees for sending and receiving money overseas. These fees can include outgoing, incoming, initiation, and tracer fees. The exchange rate at the time of the transaction also influences the amount of money sent and received, and banks may add a currency conversion charge. The type of payment also determines the fees, with three types of payments for international transfers: OUR, SHA, and BEN. OUR means the sender covers all transfer fees, BEN means the receiver covers all transfer fees, and SHA is shared but rarely used. While banks may charge hefty fees, there are alternative options, such as specialist international money transfer services, which offer lower fees and faster transactions.

| Characteristics | Values |

|---|---|

| Types of payments for international transfers | OUR, SHA, BEN |

| OUR | Sender takes care of all transfer fees |

| BEN | Receiver takes care of all transfer fees |

| SHA | Shared |

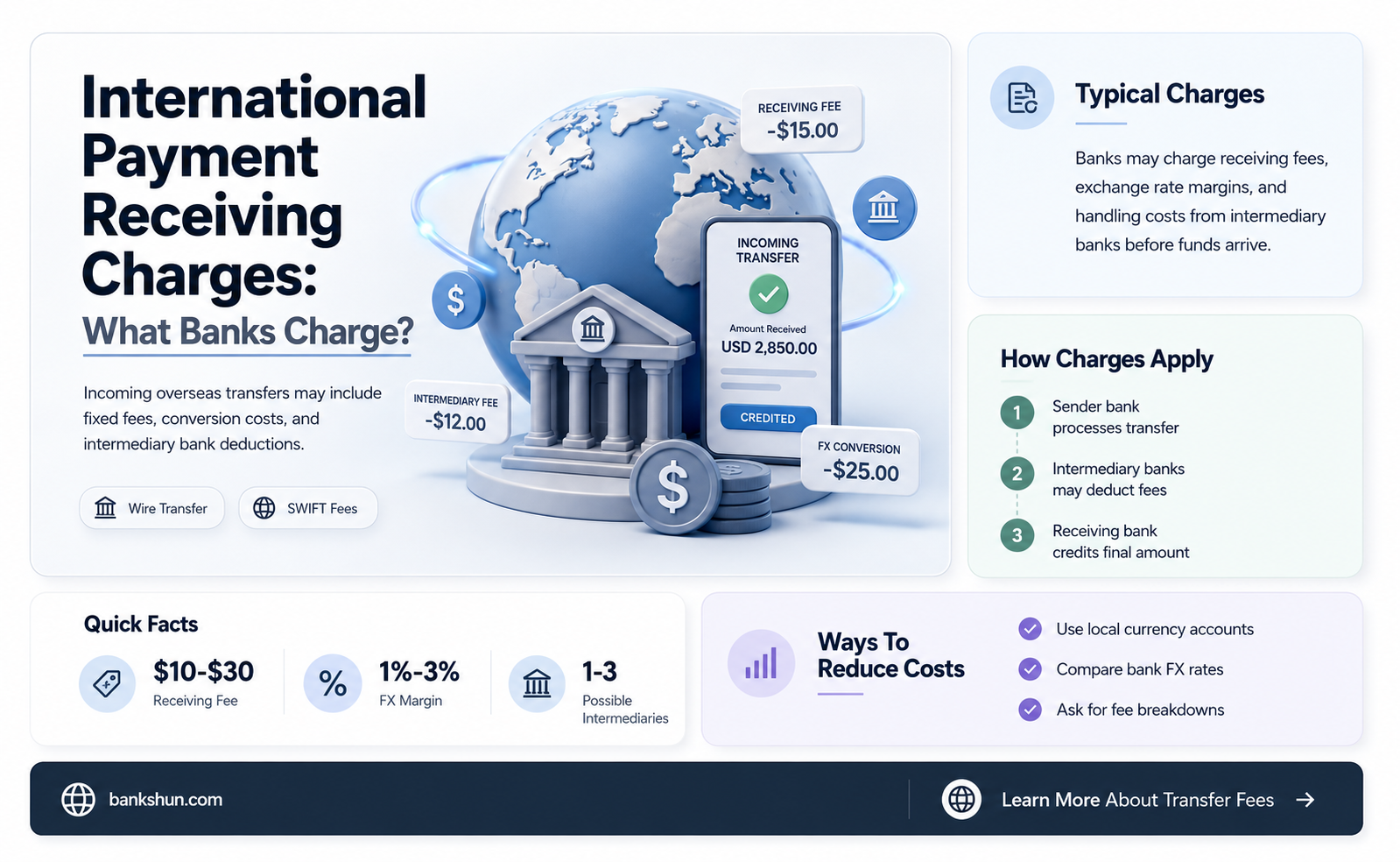

| Bank charges | 3-4% of the total transfer amount |

| Additional charges | SWIFT tracing fee, bank overheads, processing fees |

| Exchange rates | Vary based on the bank and currency |

| Inbound exchange rate | Includes a currency conversion mark-up of 0.5% |

| Outgoing fee | Cost of transferring money to another country |

| Incoming fee | Cost of receiving money from overseas |

| Initiation fee | Setup fee for online, phone, or branch transfers |

| Tracer fee | Fee for tracking the progress of a transfer |

| SEPA payments | Fee-free and arrive on the same day |

Explore related products

What You'll Learn

![]()

Sender vs. receiver fees

When it comes to international payments, banks typically charge both the sender and the receiver in the form of various fees. These fees can vary depending on the bank and the type of transfer.

Sender Fees

As the sender, you are usually responsible for covering the cost of transferring the funds internationally. This is often referred to as an outgoing fee and can be a flat rate or a percentage of the total transfer amount. For example, some banks may charge up to 3-4% of the total transfer amount. Additionally, senders may also be charged a setup or initiation fee, which can vary depending on the method of transfer (online, phone, or in-branch). If the sender wishes to track the progress of the transfer, they may also be charged a tracer or tracking fee. These fees can quickly add up, especially for larger transfers or frequent transactions.

Receiver Fees

On the receiving end, the bank may charge an incoming fee for processing the international payment. This fee is typically incurred by the recipient and is deducted from the total amount received. In some cases, the receiving bank may also apply a currency conversion fee if they convert the funds into the local currency. For instance, Nationwide Bank in the UK mentions a currency conversion mark-up of 0.5% included in their standard inbound exchange rate. Additionally, the receiving party may also be charged a fee by their bank for incoming wire transfers, especially through large banks using the SWIFT network.

Alternative Options

To avoid the high fees associated with traditional banks, many individuals and businesses are turning to specialist international money transfer services, such as WorldRemit or PunkyPay, which offer lower fees and faster transactions. These services often provide more competitive rates and flexible options for sending and receiving money globally.

It is important to note that the specific fees and charges may vary depending on the bank and the location. Therefore, it is always advisable to contact your bank or financial institution to understand the exact charges applicable to your international transactions.

How to Negotiate Better Interest Rates with Your Bank

You may want to see also

Explore related products

![]()

SWIFT payments

SWIFT, founded in Brussels in 1973, is a secure global system that connects banking institutions. It is used by more than 11,000 banking institutions in over 200 countries, with an average of 42 million messages sent per day in 2021.

SWIFT is a vital component of the global payments system, acting as a carrier of messages containing payment instructions between financial institutions involved in a transaction. However, it is important to note that SWIFT does not hold funds, issue or manage accounts, or provide settlement functions for transactions. Instead, it focuses on providing a network for transmitting messages between parties in a secure, accurate, and reliable way.

To make a SWIFT payment, you will need to provide your International Bank Account Number (IBAN) or account number, the name and address of the bank receiving the funds, and the Bank Identifier Code (BIC) of the receiving bank if the payment is not in euros sent to the Single Euro Payments Area (SEPA) Zone. You can only receive a SWIFT payment to your current account, not a savings account.

When receiving an international inbound payment in foreign currency, banks like Nationwide use a standard inbound exchange rate to convert the currency, which may include a currency conversion mark-up. This mark-up is set by a third party and is included in the exchange rate shown on your statement.

The Truth About Ray Gibson and Claude Banks: Fact or Fiction?

You may want to see also

Explore related products

![]()

SEPA payments

SEPA stands for Single Euro Payments Area. It was launched by the European banking and payments industry with support from national governments, the European Commission, the Eurosystem, and other public authorities. SEPA is a European Union (EU) initiative that aims to improve the efficiency of cross-border payments and turn the previously fragmented national markets for euro payments into a single domestic one.

SEPA enables customers to make cashless euro payments to any account located in the SEPA region, using a single bank account and a single set of payment instruments. The SEPA region consists of 41 European countries, including several countries that are not part of the euro area or the European Union.

SEPA Credit Transfer (SCT) allows for the transfer of funds from one bank account to another. SEPA clearing rules require that payments made before the cutoff point on a working day be credited to the recipient's account by the next working day. SEPA Instant Credit Transfer (SCT Inst) provides for the instant crediting of a payee, with a maximum delay of twenty seconds in exceptional circumstances.

To make a SEPA payment, you will need the International Bank Account Number (IBAN) or account number of the recipient, as well as the name and address of the bank receiving the funds. If the payment is not in euros and is being sent to a non-SEPA Eurozone country, you will also need the Bank Identifier Code (BIC) of the receiving bank.

It is important to note that banks offering SEPA payments are not obliged to participate in this scheme, and participation is optional.

Crafting a Piggy Bank: DIY Guide for Beginners

You may want to see also

Explore related products

![]()

Exchange rates

The exchange rate used will depend on the date the currency is converted and the bank processing the payment. For example, the US Internal Revenue Service (IRS) states that if it receives a US tax payment in foreign currency, the exchange rate used to convert it into US dollars is based on the date the currency is converted, not the date it is received.

There are various online tools available to check exchange rates, such as currency converters offered by Xe and OANDA. These sources claim to offer real-time, accurate, and reliable data for hundreds of currencies. OANDA, for instance, provides access to over 31 years of historical data for over 38,000 forex pairs and rates from over 200 currencies.

It is important to note that currency conversion rates differ between companies as each company manipulates the interbank rate to make a profit. Therefore, individuals should be cautious when choosing a company to transfer money internationally, as the rates offered may be drastically changed once the customer is committed.

Understanding NSF in Banking: What It Stands For

You may want to see also

Explore related products

![]()

Specialist transfer services

One such service is WorldRemit, which offers customers the chance to send money anywhere in the world flexibly, at a typical high street bank. WorldRemit charges lower fees than traditional banks, although there will always be some sort of charge.

Another option is Wise, which has over 14.8 million customers in 80 countries and supports 50+ currencies. Wise offers a free mid-market exchange rate with no hidden fees and allows users to pay and withdraw cash worldwide without any foreign transaction fees. Wise also offers an international business account, which allows businesses to make payments and get paid in 40+ currencies.

Xoom is another specialist transfer service, which is a subsidiary of PayPal. Users can send money through the Xoom or PayPal app without registering a new account. Xoom offers fast transfers to many countries and the option to use PayPal or cryptocurrency to fund transfers.

Other specialist transfer services include Remitly, which offers two transfer options: Economy and Express, allowing users to choose between lower fees or faster transfers. MoneyGram Money Transfers is another service that lets users schedule weekly or monthly transfers.

Currency Exchange: Are There Fees and How Much?

You may want to see also