Financing multiple properties can be challenging, and many banks are hesitant to finance more than four investment properties due to increased lending risk. However, several options are available for borrowers seeking to finance more than four rental properties. One option is to consider a blanket mortgage, which allows you to finance multiple rental properties with a single set of fees and closing costs. Another option is to explore portfolio lenders, which include smaller private banks, financial firms, or investors, but they may charge higher interest rates and fees. It is essential to compare loan rates, costs, and terms carefully and to work with an experienced mortgage broker. Additionally, individuals can use their existing assets, such as their primary residence or investment portfolios, as collateral to secure lending for new real estate investments.

| Characteristics | Values |

|---|---|

| N/A | N/A |

Explore related products

What You'll Learn

![]()

Banks' exposure to the CRE market

The CRE financing sector is large, standing at approximately $4.5 trillion. Banks and thrifts hold the largest share of CRE financing at around 40% through a mix of owner-occupied and non-owner-occupied loans. The money center and larger regional banks hold around a quarter of the market for CRE loans. When compared to their respective asset bases, smaller regional and community banks have greater exposures. This is because smaller banks are local lenders and are likely better placed to lend in their local geographies.

The US banking sector is currently facing major stress, particularly in commercial real estate. However, this recent stress in the banking sector is not a systemic commercial real estate (CRE) debt problem, and the risk of loss to lenders is likely to be smaller than many believe. US banks’ holdings of CRE loans are just 13% of their total assets. At the end of 2007, banks held 17% of their total assets in single-family mortgages.

The CRE mortgage market for income-producing properties is roughly $4.5 trillion, based on Mortgage Bankers Association data analysis. There are also $467 billion in construction loans, and the FDIC classifies $627 billion of owner-occupied property loans as commercial mortgages. Banks and thrifts have the greatest share of the lending market at ~38%. While office sector loans (16.7% of the total) receive the most attention, multifamily loans represent the most significant exposure (~44%).

In Hong Kong, the CRE market has entered a period of acute stress, with systemic risks crystallizing in the form of deteriorating loan quality and rising credit defaults. HSBC classifies 73% of Hong Kong CRE loans as high-risk, signaling systemic stress with a 6.7% NPL ratio—the highest since 1999. Key drivers include high debt leverage, 20%+ office rent declines, and geographic concentration in weak secondary markets like Kowloon East. Hong Kong's five domestic systemically important banks (D-SIBs) collectively hold 25.75% of their loan portfolios in CRE, with Hang Seng's exposure at 36.34%.

Medicare and Bank Details: What's the Link?

You may want to see also

Explore related products

![]()

Managing multiple properties

Have a Strong Brand and Marketing Strategy

When people see any of your properties, they should recognise a consistent brand. A strong marketing strategy will help ensure your properties are occupied. Identify your target market and desirable features that your market will want.

Screen Tenants Carefully

Implement a strict tenant screening procedure to ensure you have trustworthy tenants who will care for your property, pay rent on time, and not cause issues. Consider how many people will be living in the space, as the more individuals, the more potential issues.

Have a Maintenance Plan

Prepare a maintenance plan to stay on top of repairs and ensure each property receives the attention it needs. Include seasonal tasks and be prepared for unexpected repairs. Have a network of vetted vendors, such as cleaners, plumbers, roofers, electricians, and HVAC specialists, who you can call for repairs.

Provide Good Communication and Customer Service

It is essential to have good communication channels with your tenants. They should feel comfortable reaching out to you with issues, and you should respond promptly. Offer a 24/7 line they can call, and stay professional and friendly to keep tenants happy and avoid negative reviews.

Hire a Team or Consultant

Consider hiring a team or property management consultant to help you manage everything, including maintenance, rent collection, and tenant screening. Ensure your team is qualified and well-trained to handle property-related tasks.

Use Online Systems and Software

Utilise online systems and software to track tenant information, rent payments, maintenance requests, and financial data. This will help streamline your processes and make it easier to manage multiple properties.

By following these tips and staying organised, you can successfully manage multiple properties and grow your real estate investments.

The Federal Reserve: Central Bank or Not?

You may want to see also

Explore related products

$13.82

![]()

Finding the right lender

Start early

It is recommended that you have your first conversation with a mortgage lender six months before you plan to buy a house. This will give you time to understand the process and ask questions.

Talk to a lender before a realtor

Realtors are most effective with buyers who have already met with a lender and been pre-qualified. Your agent will want to know your budget for your first home, and without having a financial review with a lender, any price range will only be a guess.

Shop around

Mortgage brokers and realtors can be a good source of recommendations for lenders. Ask for a couple of suggestions and get quotes from each. It is also worth checking that the lender is local as the realtors and lenders often work in the same circle and having a group of people who have worked together multiple times can be beneficial.

Ask questions

Ask the lender about the most popular mortgages they offer and why they are so popular. Also, ask which mortgage products they would recommend for your situation. Are their rates, terms, fees, and closing costs negotiable? Do they offer any discounts? Will you have to buy private mortgage insurance? If so, how much will it cost, and how long will it be required?

Communication

It is important that the lender is easy to communicate with and responsive. They should be patient and explain things in a way that is easy to understand. You should not feel rushed or that they are withholding information.

Speed

If you are looking for a quick close, you will need a lender that can get things through the process fast. Some lenders may struggle to complete the process in 30 days, which can cause problems with the seller.

First-time buyers

If this is your first time buying a home, look for a lender that focuses on first-time homebuyers. You may need more time to understand the process and your budget may not be as high, so look for a lender that is patient and treats you well.

Managing Model Risk: A Vital Banking Priority

You may want to see also

Explore related products

![]()

Borrowing against assets

There are several ways to borrow against your assets, including securities-based lending, real estate-backed borrowing, and specialty-asset financing. Each of these options has its own unique risks and requirements. For example, a securities-based line of credit (SBLOC) allows you to borrow against the value of your portfolio, usually at variable interest rates, but it cannot be used to purchase securities or pay down margin loans. A home equity line of credit (HELOC) is another option, where you can borrow against the equity in your home, typically with a variable interest rate.

When borrowing against assets, it is important to understand the risks involved. The market value of the pledged collateral can decrease, which may result in the bank demanding immediate repayment or additional collateral. To mitigate this risk, it is recommended to pledge diversified assets and borrow an amount significantly lower than the pledged value. Additionally, the interest rates and credit spreads charged by lenders may vary, and higher rates can impact the feasibility of borrowing.

Before proceeding with borrowing against assets, it is advisable to consult a financial professional to thoroughly understand the risks and requirements involved. Additionally, consider the tax implications of such transactions and seek guidance from a tax professional to assess how it could affect your tax liability.

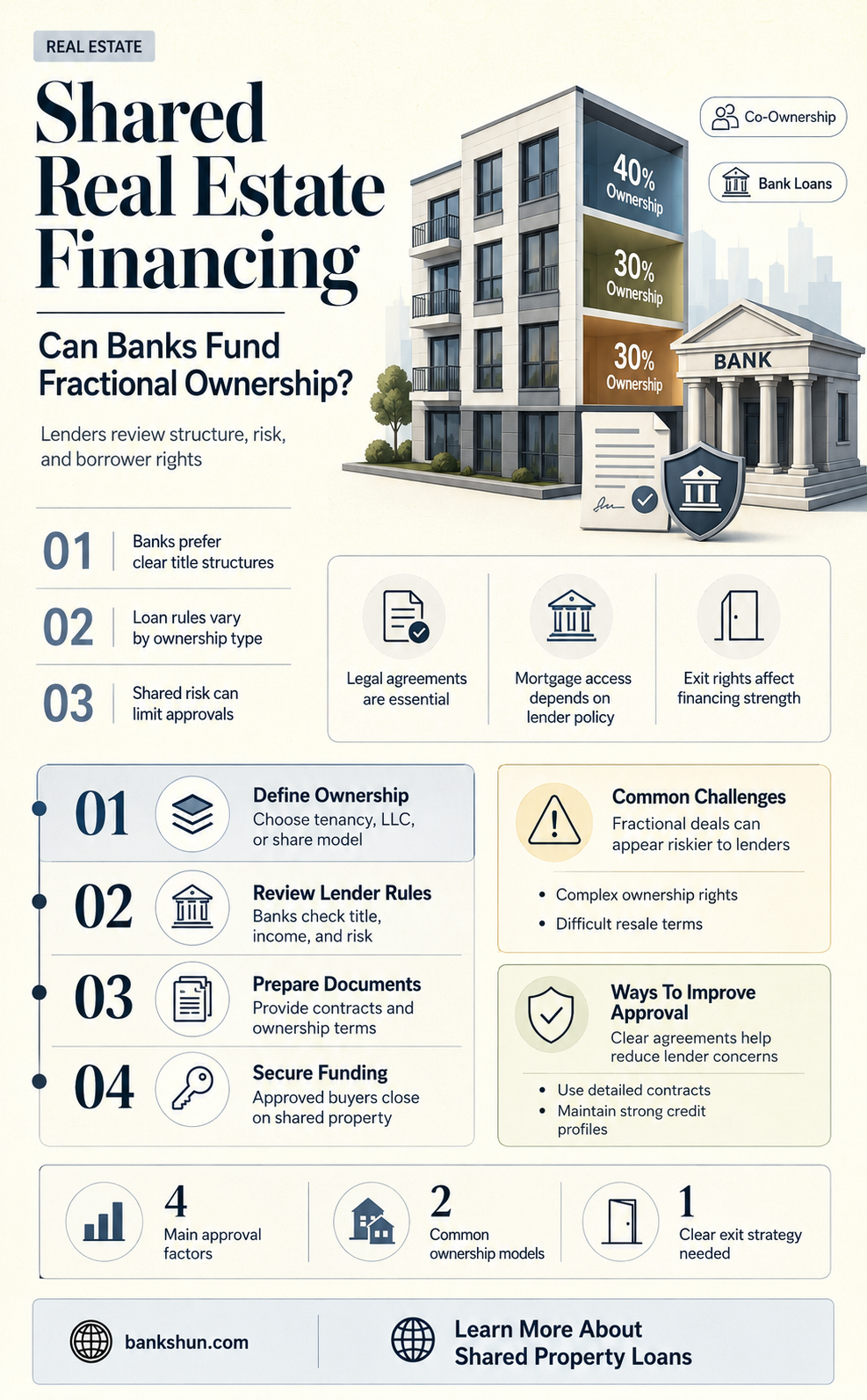

While I cannot provide specific information about 1/4 share real estate, the provided information offers a comprehensive overview of borrowing against assets, which may include real estate holdings.

Banks Sell Mortgages: Why and What It Means for You

You may want to see also

Explore related products

![]()

Banks' role in real estate

Banks play a crucial role in the real estate market, which is a significant driver of the global economy. They provide financing for home purchases and are among the largest providers of mortgage loans worldwide. Banks assess a borrower's creditworthiness, income, and debt-to-income ratio to determine their ability to repay mortgage loans. Additionally, they participate in the secondary mortgage market and finance commercial real estate properties. According to sources, banks and thrifts hold the largest share of CRE financing at around 40%.

Regional banks, in particular, have carved a niche in the commercial real estate sector, contributing significantly to its development and growth. They provide a significant proportion of loans to developers and managers due to their localized knowledge and understanding of specific markets. Regional banks can offer more personalized services and build long-term relationships with clients. However, they may face challenges due to liquidity pressures and regulatory scrutiny, which can impact their lending capacity and, consequently, the real estate market.

The current interest rate cycle has created stress for the US banking sector, especially with the weakening of the commercial real estate (CRE) sector. While this situation is not expected to replicate the residential mortgage crisis, it has led to tighter lending standards and higher interest rates, making it harder for individuals to obtain mortgages and slowing down the real estate market.

Big banks also influence the real estate market through their involvement in real estate investment trusts (REITs) and the appraisal process. REITs are companies that own and operate income-generating properties, such as office buildings and shopping centres. Banks rely on appraisals to ensure they do not lend more than a property is worth, but pressure for high valuations can contribute to a housing bubble. Therefore, policymakers and regulators must monitor the actions of big banks to prevent instability in the housing market.

Overall, banks facilitate real estate transactions, development projects, and sector growth by connecting investors with opportunities. Real estate investment bankers help clients navigate economic fluctuations and market risks while securing the necessary capital for their clients' real estate purchases.

Retail vs Commercial Banks: What's the Difference?

You may want to see also

Frequently asked questions

Many banks and lenders are hesitant to finance multiple investment properties at the same time because it increases their lending risk. This means that finding financing for more than four properties can be challenging.

One option is to use a blanket mortgage, which allows you to finance multiple rental properties with one set of fees and closing costs. However, defaulting on one property could result in the lender claiming all your properties covered by the loan. Another option is to try a portfolio lender, which could be a smaller private bank, financial firm, or investor.

It is recommended to try many different lenders, including local banks, credit unions, and private lenders. It is also important to find an experienced mortgage broker who understands how to navigate these types of loans.

Yes, individuals with a high net worth can use their assets as collateral to secure lending for additional properties. However, this exposes those assets to increased risk, so it is important to carefully consider your financial capacity and investment knowledge before proceeding.