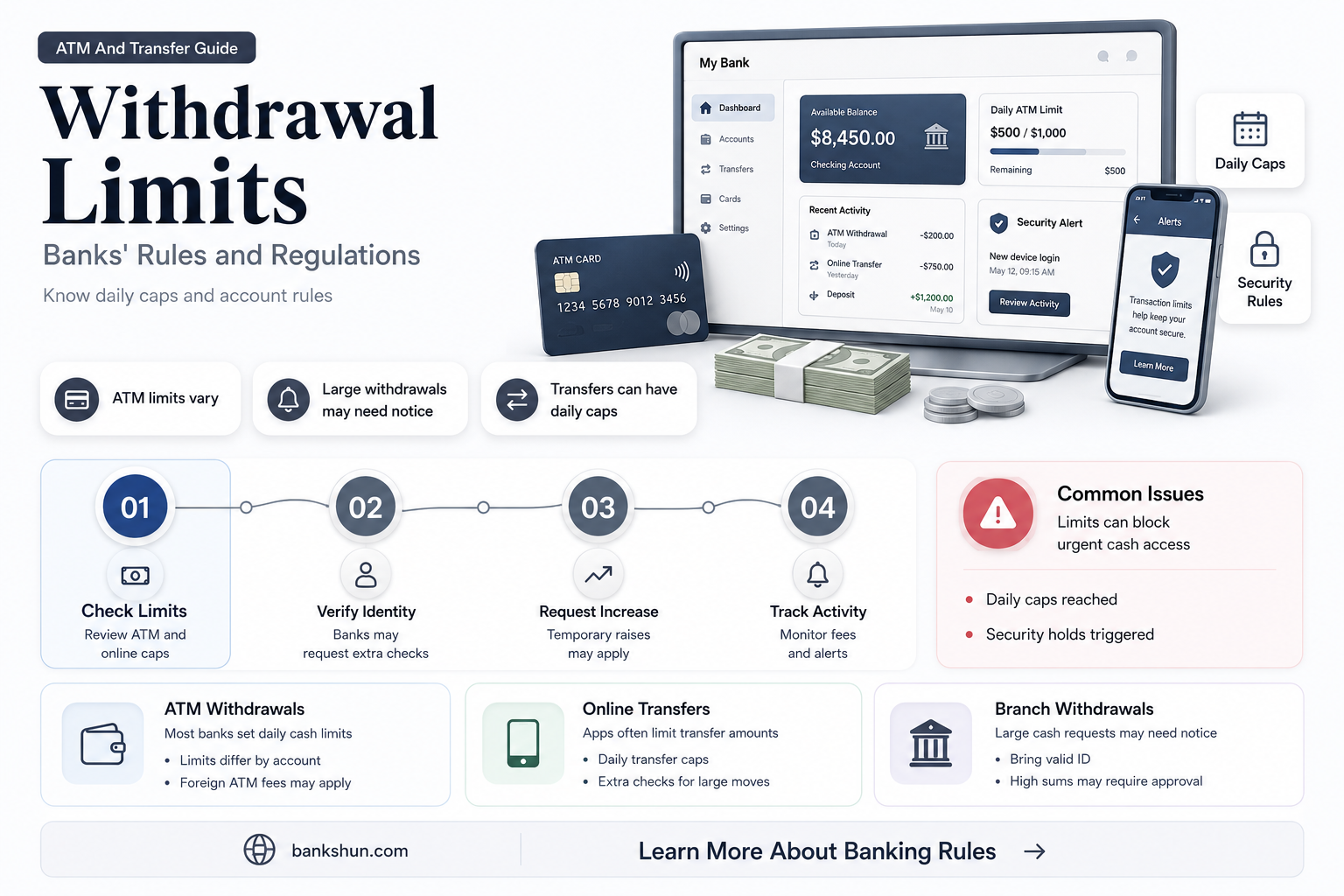

Banks usually impose withdrawal limits to monitor and control liquidity and to protect account holders from fraud. These limits vary depending on the type of account and the method of withdrawal. ATM withdrawals typically have the lowest limits, ranging from $300 to $1000 per day. Debit card transactions have higher limits, often around $5000 per day, while in-person withdrawals at a bank branch usually have the highest limits. Some banks may allow customers to request temporary or permanent increases in their withdrawal limits for specific purposes, such as vacations or jobs that require high cash spending. Additionally, savings accounts may have monthly withdrawal limits, with a legal maximum of six transactions per month. Understanding your bank's specific withdrawal limits and policies is essential for effective financial planning and security.

| Characteristics | Values |

|---|---|

| Purpose of withdrawal limits | Monitor and control liquidity, protect account holders from fraud |

| Types of withdrawal limits | ATM withdrawal limit, debit withdrawal limit, total spending limit |

| ATM withdrawal limit | Typically ranges from $300 to $1,000 per day, varies by bank and account type |

| Debit withdrawal limit | Typically higher than ATM withdrawal limit, often around $5,000 per day |

| Total spending limit | Cumulative limit on all transactions in a day |

| Savings account withdrawal limit | Typically no more than six transactions per month, some banks may have monthly withdrawal limits |

| Increasing withdrawal limit | Request a temporary or permanent increase from the bank, may depend on factors like account type and banking history |

Explore related products

What You'll Learn

![]()

ATM withdrawal limits

Banks impose ATM withdrawal limits to restrict the amount that can be withdrawn from an ATM in a day. These limits vary by institution and account type, with basic accounts having lower limits than premium accounts. ATM withdrawal limits typically range from $300 to $1,500 per day, but some banks allow withdrawals of up to $5,000 per day.

The reasons for ATM withdrawal limits are twofold: firstly, to ensure there is enough cash available for all customers, as ATMs can only hold a limited amount of cash; secondly, to protect customers' accounts from fraudulent activity. If a thief were to gain access to your card and PIN, a withdrawal limit would prevent them from draining your account.

Some banks may allow customers to request a temporary or permanent increase in their ATM withdrawal limit, especially for one-time purchases or emergencies. It is important to familiarise yourself with your bank's withdrawal limits and plan your purchases accordingly.

Bank Fees for Patreon: What You Need to Know

You may want to see also

Explore related products

![]()

Debit card spending limits

Banks impose debit card spending limits to safeguard customers from excessive or unauthorised spending in case their card or account details are stolen. These limits vary depending on the financial institution, with daily purchase limits ranging from $300 to $10,000, and ATM withdrawal limits ranging from $200 to $5,000.

Some banks offer higher debit card limits for premium accounts that maintain higher account balances. Additionally, certain banks set separate limits for ATM cash withdrawals, while others include ATM withdrawals within their debit card spending limits.

It is important to note that debit card limits are not usually displayed on statements or mobile apps. To check your daily spending limit, you may need to contact your bank directly. If you anticipate making a large purchase that exceeds your daily limit, you can request a temporary or permanent increase from your bank.

When travelling, it is recommended to carry an alternative method of payment as a backup. Additionally, informing your bank of your travel plans can help minimise any potential issues when using your debit card internationally.

Union Bank and US Bank: Merged or Not?

You may want to see also

Explore related products

![]()

Cash withdrawal limits

Banks typically impose cash withdrawal limits for two main reasons: to monitor and control liquidity, and to protect account holders from fraud. By limiting the amount of cash that can be withdrawn per customer, banks can ensure that they have enough cash on hand for all customers.

Most banks set the lowest limits on ATM withdrawals, which can range from $300 to $1,000 per day. ATM withdrawal limits may also depend on the account type, with new or basic accounts having lower limits than premium accounts. Some banks may allow customers to request a temporary or permanent increase in their ATM withdrawal limit, especially for emergency spending or last-minute funding. For example, if you're going on vacation and need more cash on hand, you may be able to get a temporary increase.

Banks also set limits on debit card transactions, which are usually higher than ATM withdrawal limits. These limits typically range from $3,000 to $5,000 per day. Debit card spending limits are in place to address security concerns, as debit card purchases pose the same security risks as ATM withdrawals.

In addition, banks may set limits on the number of transactions that can be made from a savings account each month, usually allowing up to six transactions. While banks rarely set withdrawal limits on savings accounts, some may impose monthly withdrawal limits, and ATM withdrawals may contribute to this limit.

Who Funds Federal Banks? Government Funding Explained

You may want to see also

Explore related products

![]()

Withdrawal limit exemptions

Banks typically impose withdrawal limits for two main reasons: to monitor and control liquidity, and to protect account holders from fraud. While there are no longer federal requirements for banks to enforce withdrawal limits, individual banks may still set their own restrictions.

In 2020, the Federal Reserve removed the requirement for banks to enforce a limit on withdrawals. This was done to give consumers greater access to their cash during the coronavirus pandemic and its related economic impact. Despite this, some banks and credit unions have maintained the six-transaction limit, while others do not enforce the rule.

The previous federal rule, known as Regulation D, limited certain types of withdrawals, known as "'convenient transactions," to no more than six a month. These included using a debit card, writing a check, overdraft-related transfers, bill payments, and other money transfers done online, by phone, or by fax.

While banks often have some sort of cash withdrawal limit, these are typically much higher than ATM withdrawal limits. Banks may also set their limits around immediate transactions, meaning that you can still withdraw large amounts of cash but will need to make a request in advance.

The lowest limits are usually set for ATM withdrawals, which can range from $300 to $1,000 in a 24-hour period. ATM withdrawal limits are the maximum amount of physical cash you can take out of an ATM. These limits are set by both the bank and individual ATM operators, so if your bank has a higher withdrawal limit than a particular ATM, you can withdraw the amount allowed by that ATM and then visit another ATM to withdraw the remaining amount.

Debit card transactions usually have higher limits than ATM withdrawals, commonly around $5,000 per day. In-person withdrawals at a bank teller typically have the highest limits.

If you need to withdraw more cash than your account allows, you can request a temporary increase from your bank. This decision may depend on factors such as your banking history, the type of account you hold, and the amount of the increase requested.

Canadian Banks in Cuba: Exploring the Presence

You may want to see also

![]()

Savings account withdrawal limits

Savings accounts are designed to help customers save money and grow their balance over time. Banks may impose withdrawal limits to prevent customers from dipping into their savings too often. While there are no longer federal regulations limiting the number of withdrawals from savings accounts, individual banks may still enforce their own restrictions.

Federal Regulations

Before 2020, Regulation D restricted consumers from making more than six withdrawals a month from certain deposit accounts, including savings and money market accounts. This regulation was intended to encourage Americans to save money and ensure banks had enough cash reserves. However, as of April 2020, the Federal Reserve removed the requirement for banks to enforce this limit. Now, financial institutions can allow customers to make an unlimited number of withdrawals from their savings accounts.

Bank-Imposed Limits

Despite the change in federal regulations, some banks and credit unions have chosen to maintain withdrawal restrictions. These limits typically apply to "convenient transfers," such as using a debit card, writing a check, making transfers online or over the phone, and bill payments. Banks may also impose a minimum monthly balance requirement.

If you exceed the withdrawal limit set by your bank, you may face fees, interest rate reductions, account restrictions, or even account closure. These fees are typically charged per transaction and can range from $3 to $5, although some banks may charge more. To avoid these fees, it is recommended to use a checking account for most transactions and only use your savings account for emergencies or long-term goals.

It is important to note that withdrawal limits do not usually apply to ATM withdrawals or in-person bank withdrawals. Additionally, banks may impose separate withdrawal limits for ATM transactions due to the risk of fraud.

While federal regulations no longer restrict the number of withdrawals from savings accounts, individual banks may still enforce their own limits. These limits are intended to help customers save and ensure banks have sufficient reserves. To avoid fees and penalties, it is essential to understand your bank's specific policies and plan your transactions accordingly.

PNC Bank: Where is it Located?

You may want to see also

Frequently asked questions

Yes, banks do have withdrawal limits. These limits vary depending on the type of account and the bank itself. ATM withdrawals typically have the lowest limits, ranging from $300 to $1,000 per day. Debit card transactions have higher limits, often around $5,000 per day. In-person withdrawals at a bank branch usually have the highest limit.

Your bank's withdrawal limit should be included in the documents provided when you open your account or receive your debit card. Alternatively, the limit may be mentioned in your bank's official banking app. If you cannot find the information, you can always contact your bank to clarify your individual withdrawal limit.

Some banks allow customers to request a temporary or permanent increase in their withdrawal limit. This decision is typically made on a case-by-case basis and may depend on factors such as your banking history and the type of account you hold.