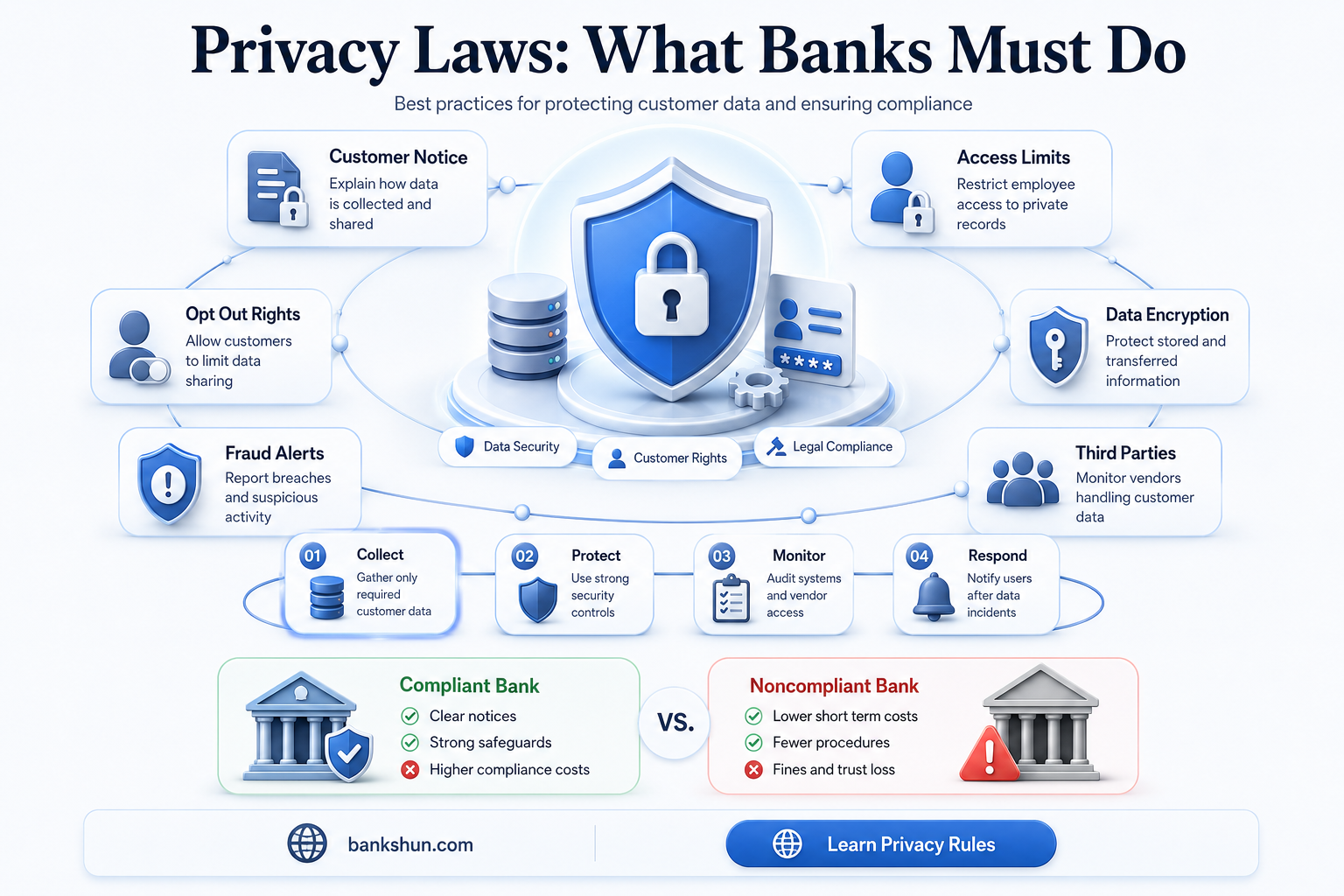

Banks are required to follow privacy laws to protect the privacy of consumers' finances. In the United States, financial privacy is regulated through laws enacted at the federal and state level. Federal laws such as the Bank Secrecy Act, the Right to Financial Privacy Act, the Gramm-Leach-Bliley Act, and the Fair Credit Reporting Act outline privacy requirements for financial institutions, including banks. These laws govern how banks collect, use, and disclose customers' personal financial information, with provisions for protecting nonpublic personal information and restricting information sharing with third parties. While banks have some flexibility in how they implement these laws, non-compliance can result in legal consequences.

| Characteristics | Values |

|---|---|

| Federal laws that regulate information sharing | Gramm-Leach-Bliley Act, Fair Credit Reporting Act, Credit and Debit Card Receipt Clarification Act, Electronic Funds Transfer Act, Financial Modernization Act, Bank Secrecy Act, Right to Financial Privacy Act, Telephone Consumer Protection Act |

| Privacy policies | Financial institutions must provide notices and comply with limitations on the disclosure of nonpublic personal information |

| Consumer rights | Consumers can opt out of the disclosure of their nonpublic personal information to nonaffiliated third parties, stop telemarketing calls, and prevent the government from accessing their financial records |

| Enforcement | Consumer Financial Protection Bureau, Federal Trade Commission, National Credit Union Administration, Securities Exchange Commission, Treasury Department |

| State laws | Vary from state to state, but mostly draw from federal laws and provide more stringent outlines and definitions |

Explore related products

![Information Privacy Law: [Connected Ebook] (Aspen Casebook)](https://m.media-amazon.com/images/I/61KUKAMt-5L._AC_UY218_.jpg)

What You'll Learn

![]()

Banks must notify customers of electronic fund transfer policies

Banks are required to follow privacy laws, which vary from state to state in the US. These laws regulate how financial institutions handle the nonpublic financial information of consumers. The Right to Financial Privacy Act of 1978 (RFPA) was passed to limit the government's ability to freely access nonpublic financial records. The RFPA defines financial institutions as any institution that engages in activities regarding banking, credit cards, and consumer finance.

The Electronic Funds Transfer Act (EFTA), passed in 1978, requires banks to notify customers of any policies regarding the electronic transfer of funds. This includes the requirement to provide a model statement to regulate the language used when presenting these policies to consumers. Banks are also held liable if information is disclosed through the telephone without consent and for any damages that occur as a result of unauthorized access to a consumer's information.

The EFTA and Regulation E apply to the electronic fund transfer that authorizes a financial institution to debit or credit a consumer's account. Regulation E defines a financial institution as a bank, savings association, credit union, or any other entity that directly or indirectly holds a consumer's account or issues an access device and agrees to provide EFT services. Any entity defined as a financial institution under Regulation E has error resolution obligations if a consumer notifies them of an error.

The privacy rule, as outlined in the Privacy Rule Handbook, restricts information sharing with non-affiliated third parties. It also provides a definition of a customer as a consumer with whom a bank has a continuing relationship, which is established when a consumer receives continued service following or in connection with a transaction.

Jesus and Banks: Did They Exist Together?

You may want to see also

Explore related products

![]()

Financial institutions must protect customer information

In the United States, financial privacy is regulated through laws enacted at the federal and state levels. Federal regulations include the Bank Secrecy Act, the Right to Financial Privacy Act, the Gramm-Leach-Bliley Act, and the Fair Credit Reporting Act.

The Gramm-Leach-Bliley Act requires financial institutions to explain their information-sharing practices to their customers and protect their sensitive data. Financial institutions must annually disclose to consumers their policies and practices regarding the protection and disclosure of nonpublic personal information to affiliates and nonaffiliated third parties. This includes any record containing nonpublic personal information about a customer, whether in paper, electronic, or other form, that is handled or maintained by or on behalf of the financial institution or its affiliates.

The Privacy Rule protects a consumer's nonpublic personal information (NPI), which is any personally identifiable financial information that a financial institution collects about an individual in connection with providing a financial product or service, unless that information is otherwise publicly available. Financial institutions must give their customers a clear and conspicuous written notice describing their privacy policies and practices.

The Red Flags Rule, set under FACTA, requires financial institutions and creditors to develop and implement programs to identify and prevent identity theft threats. The Credit and Debit Card Receipt Clarification Act, passed in 2007, requires that account numbers printed on receipts be shortened to five digits to protect consumer privacy.

The Electronic Funds Transfer Act regulates the electronic transfer of funds, requiring banks to notify customers of any policies regarding such transfers. Banks are also held liable in the event that information is disclosed through the telephone without consent and for any damages that arise from unauthorized access to a consumer's information.

Your Savings: Are They Safe in a Bank?

You may want to see also

Explore related products

![]()

Banks can share account numbers for marketing

In the United States, financial privacy is regulated through laws enacted at the federal and state level. Federal regulations are primarily represented by the Bank Secrecy Act, Right to Financial Privacy Act, the Gramm-Leach-Bliley Act, and the Fair Credit Reporting Act.

The Gramm-Leach-Bliley Act of 1999 established a set of comprehensive privacy laws at the federal level applicable to any firm that provides financial services. This law established four new requirements regarding the nonpublic personal information of a consumer, including the annual disclosure of a privacy policy.

The Right to Financial Privacy Act of 1978 was passed primarily as a response to the Supreme Court ruling on United States v. Miller (1976) and to supplement the Bank Secrecy Act. The act was put in place to limit the government's ability to freely access nonpublic financial records.

The Fair Credit Reporting Act contains many important privacy safeguards. It gives consumers the ability to stop the sharing of their credit application information or other personal information obtained from third parties with affiliated companies.

The privacy rule restricts information sharing with nonaffiliated third parties. Banks that share nonpublic personal information about consumers with nonaffiliated third parties must provide consumers with a reasonable opportunity to opt out.

The privacy rule prohibits banks from disclosing account numbers or access codes for credit card, deposit, or transaction accounts to any nonaffiliated third party for use in marketing. However, there are two exceptions to this rule. Banks may share account numbers in conjunction with marketing their own products as long as the service provider is not authorized to directly initiate charges to the accounts. Banks may also disclose account numbers to participants in a private label or affinity credit card program when the participants are identified to the customer.

Huntington Bank Branches: Florida Locations

You may want to see also

Explore related products

$6.04 $6.04

$19.21 $35

![]()

The Right to Financial Privacy Act limits government access

Banks are subject to a variety of privacy laws that govern how they handle their customers' personal and financial information. These laws are in place to protect consumers from improper disclosure of their data to third parties, including the government.

The Right to Financial Privacy Act (RFPA) was enacted in 1978 to limit the government's ability to freely access nonpublic financial records. The RFPA defines financial institutions as any entity that engages in banking, credit card, or consumer finance activities. It also defines financial records as any documentation of a consumer's relationship with a financial institution. The RFPA was designed to reverse the Supreme Court's ruling on United States v. Miller (1976), which stated that individuals had no expectation of privacy regarding records developed or maintained by a third party during the course of an ordinary business relationship.

The RFPA requires federal government agencies to notify customers in advance of requesting their financial records from financial institutions. Customers are then given the opportunity to challenge the government's access to their records before disclosure takes place. The RFPA also requires government agencies to produce an audit trail documenting the disclosure of customer information. It's important to note that the RFPA only governs disclosures to federal government entities and does not apply to state or local governments, or private businesses.

In addition to the RFPA, there are other laws in place to protect financial privacy, such as the Bank Secrecy Act, the Gramm-Leach-Bliley Act, the Fair Credit Reporting Act, the Credit and Debit Card Receipt Clarification Act, and the Electronic Funds Transfer Act. These laws establish privacy policies, restrict information sharing with non-affiliated third parties, and hold banks liable for unauthorized access to consumer information.

While federal laws provide a baseline for financial privacy protection, individual states in the US have their own regulations that often provide more stringent definitions and enforcement mechanisms. For example, the California Consumer Privacy Act protects the nonpublic information of all California residents. Overall, the interplay between federal and state laws helps to safeguard consumers' financial privacy and ensure that banks handle their sensitive information with care.

CIS Framework: A Secure Banking Future?

You may want to see also

Explore related products

$24.99 $27.99

![]()

The Gramm-Leach-Bliley Act requires annual privacy disclosures

In the United States, financial privacy is regulated by laws at both the federal and state levels. The Gramm-Leach-Bliley Act (GLBA), also known as the Financial Services Modernization Act of 1999, is one such federal law that addresses consumer financial privacy concerns. The GLBA requires financial institutions to implement regulations to protect consumer financial information and respect the privacy of their customers.

The GLBA's privacy provisions are enforced by the Federal Trade Commission (FTC) and other government agencies that regulate financial institutions. These agencies ensure that financial institutions comply with the GLBA's requirements, including the annual privacy disclosures. The GLBA also provides a model privacy form that institutions can use to satisfy the disclosure requirements. Financial institutions can also post their annual privacy notices online or use alternative delivery methods if they meet certain requirements.

The GLBA's notice and opt-out provisions are in addition to those imposed by other laws, such as the Fair Credit Reporting Act (FCRA). The GLBA requires financial institutions to make clear and conspicuous disclosures to consumers regarding the sharing of information with affiliates and nonaffiliated third parties. These disclosures must be included in any privacy policy provided to consumers.

Overall, the Gramm-Leach-Bliley Act's annual privacy disclosures are a critical component of financial privacy protection in the United States, ensuring that consumers are informed and empowered to protect their nonpublic personal information.

Wells Fargo in Hawaii: Locations and Services

You may want to see also

Frequently asked questions

Yes, banks are required to follow privacy laws. In the United States, financial privacy is regulated by federal and state laws.

Some federal laws that govern financial privacy include the Bank Secrecy Act, the Right to Financial Privacy Act, the Gramm-Leach-Bliley Act, the Fair Credit Reporting Act, and the Electronic Funds Transfer Act.

The Gramm-Leach-Bliley Act established a set of comprehensive privacy laws for financial institutions, including banks. It requires annual disclosure of privacy policies and practices regarding the protection and disclosure of nonpublic personal information to affiliates and non-affiliated third parties.

Banks are required to take steps to safeguard consumer information, such as implementing security measures and obtaining consent for information sharing. They must also notify customers of any policies regarding electronic fund transfers and are liable for unauthorized access to consumer information.

Violating privacy laws can result in legal consequences, including fines and lawsuits. The specific penalties depend on the laws violated and the severity of the breach. Additionally, banks may face reputational damage and loss of customer trust.