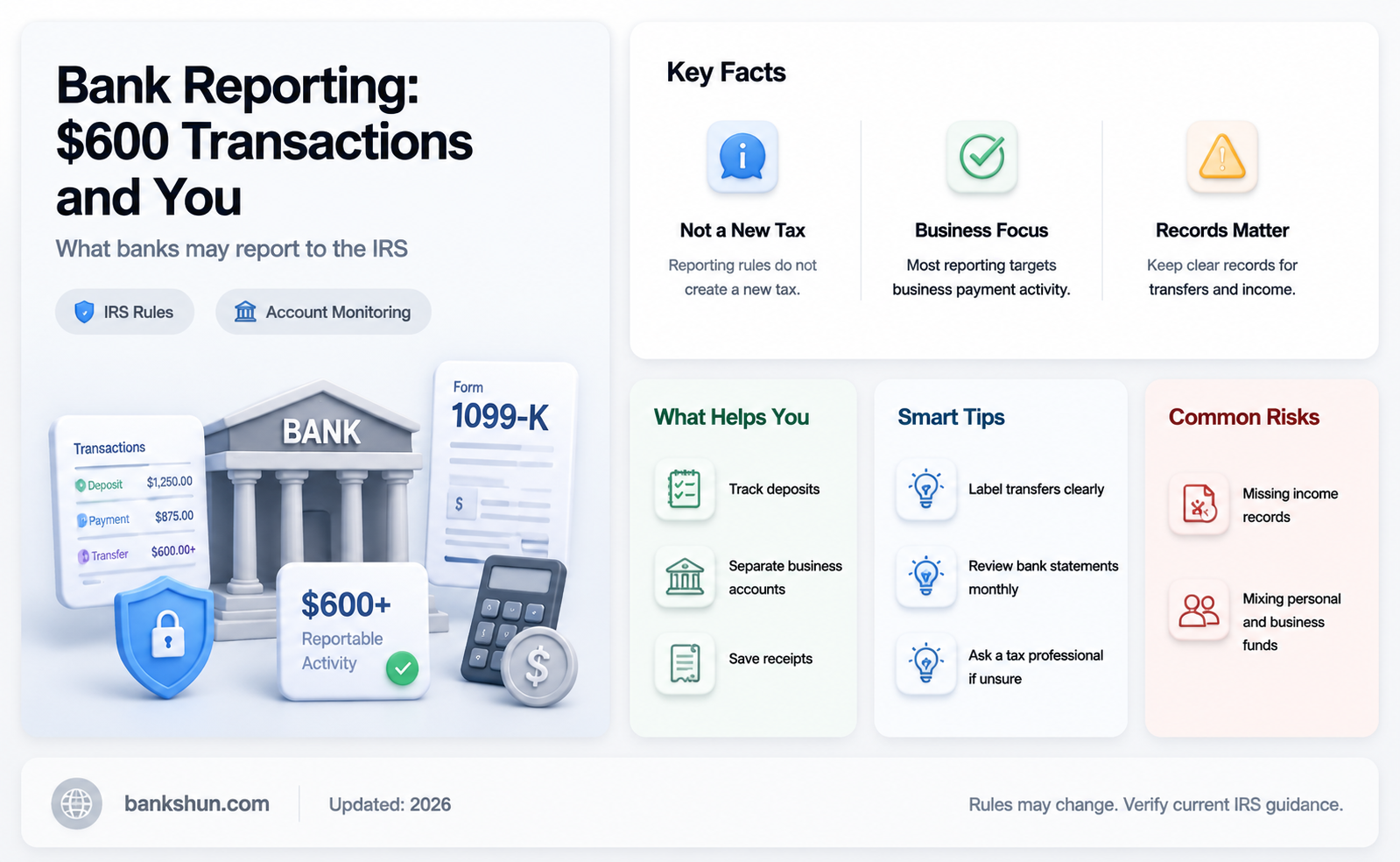

The Biden Administration's American Families Plan proposed that banks report all transactions from personal and business accounts above $600 to the IRS. This proposal was met with criticism, with many claiming it was an invasion of privacy. However, supporters of the proposal argued that it was a way to track those breaking the law and not paying their taxes. Ultimately, the proposal did not pass, and banks are not required to report transactions above $600. However, it's important to note that this is different from the $600 reporting rule for third-party payment settlement organizations like PayPal, Venmo, and Cash App, which has been delayed until 2024.

| Characteristics | Values |

|---|---|

| Proposal | Banks to report transactions over $600 |

| Status | Proposal never passed or became law |

| Affected transactions | All transactions from personal and business accounts |

| Reporting period | Annually |

| Reporting format | Aggregated numbers, not individual transaction information |

| Affected entities | Banks and third-party payment settlement organizations |

| Examples of third-party payment settlement organizations | PayPal, Venmo, Cash App, Stripe, Square, Shopify |

| Impact | Increased regulatory burden on banks and TPSOs, potential privacy concerns |

| Opposition | Independent Community Bankers of America (ICBA), Ways and Means Republican Leader Rep. Kevin Brady |

Explore related products

What You'll Learn

![]()

The $600 reporting threshold is no longer in effect

The $600 reporting threshold, enacted under Biden's American Rescue Plan, is no longer in effect. This threshold applied to third-party settlement organisations (TPSOs), which include popular payment apps and online marketplaces such as PayPal, Venmo, Cash App, Stripe, Square, and Shopify. Under this threshold, TPSOs were required to report transactions exceeding $600 in aggregate payments over the course of the year, regardless of the number of transactions. This applied to both businesses and individuals using these platforms for reimbursements or personal purchases.

The $600 reporting threshold faced criticism for being invasive and creating unnecessary complications for taxpayers. In response, the Internal Revenue Service (IRS) delayed the implementation of this threshold for the 2023 tax year, opting for a transition year to update its operations and make the reporting process easier. The IRS recognised the complexity of the new provision and the need for additional time to effectively implement the reporting requirements.

For the 2023 tax year, the previous reporting thresholds remain in place. This means that TPSOs are only required to send out Forms 1099-K to taxpayers who receive over $20,000 and have over 200 transactions. This change provides relief to taxpayers, TPSOs, and small businesses, reducing the burden of regulatory obligations.

Moving forward, the IRS plans to phase in a new threshold of $5,000 for the 2024 tax year. This gradual approach allows for a smoother transition and ensures that taxpayers, tax professionals, and software providers have the necessary time to adjust to the updated requirements. The increased threshold is expected to simplify tax compliance and reduce the burden on taxpayers, while still effectively capturing relevant tax information.

It is important to note that banks are not subject to the $600 reporting threshold. While there was a separate proposal for banks to report transactions above $600, this proposal did not pass and did not become law. Banks and financial institutions have separate reporting requirements for large cash transactions, typically involving amounts greater than $10,000.

The Two Elizabeths: Any Relation?

You may want to see also

Explore related products

![]()

Banks would have reported aggregated numbers, not individual transactions

The $600 reporting threshold was an IRS attempt to target low-income earners, freelancers, and small businesses. It was proposed that financial institutions report all transactions from personal and business accounts worth more than $600 to the IRS. However, this proposal was misleading. While the IRS would have access to more information on cash flows above $600, they would not have access to all transactions. Banks would have reported aggregated numbers, not individual transactions.

The proposal stated that banks would report gross inflows and outflows for all business and personal accounts to the IRS, "with the exception of accounts below a 'low de minimis gross flow threshold of $600 or fair market value of $600." This means that only the total amounts entering and leaving accounts would be reported, not individual transactions. The proposal indicated that the administration would be flexible on raising the $600 minimum.

The $600 reporting threshold has faced criticism for being an "unprecedented invasion of privacy." The Independent Community Bankers of America (ICBA) campaigned against it, asking communities to send letters to Biden to prevent the proposal. It has also been described as a bureaucratic nightmare, particularly for small and independent businesses.

The $600 reporting threshold was never passed into law. Instead, the threshold was restored to a far more reasonable $20,000, providing relief to self-employed individuals, small businesses, and TPSOs.

PNC Banks in Dallas, Texas: Locations and Services

You may want to see also

Explore related products

![]()

The proposal was criticised as an invasion of privacy

The proposal for banks to report transactions over $600 was criticised as an invasion of privacy. The proposal was part of the Biden administration's plan to target businesses outside of large corporations that underreport their income by approximately $166 billion per year. The proposal would require banks to report all transactions over $600 to the Internal Revenue Service (IRS).

The Independent Community Bankers of America (ICBA) campaigned against the proposal, calling it "intrusive". They argued that it would create an "unacceptable invasion of privacy" for their customers. Banks also claimed that the proposal would be an invasion of consumer privacy. Some people criticised the proposal as fearmongering, arguing that it protects taxpayers' privacy and enables the IRS to select audits more efficiently, reducing the likelihood of most taxpayers being audited.

However, others defended the proposal, such as Speaker Nancy Pelosi, who stated that it would help catch tax cheats and raise substantial revenue for the Build Back Better agenda, which provides critical investments to increase economic opportunities for American families and communities. The proposal also aimed to increase the visibility of gross receipts and deductible expenses to the IRS, enhancing the effectiveness of enforcement measures and encouraging voluntary compliance. The treasury department estimated that this form of reporting would raise $463 billion over a 10-year budget window, making it the third-largest revenue raiser proposed in the budget.

It's important to note that the proposal never became law and was met with significant opposition. The restoration of the $20,000 threshold for reporting transactions was seen as a win for self-employed individuals, small businesses, and TPSOs (third-party settlement organisations). This higher threshold reduces the burden of regulatory compliance for TPSOs and allows individuals to make transactions without excessive government involvement.

Banks and Inflation: Who Benefits?

You may want to see also

Explore related products

![]()

Third-party payment settlement organisations are impacted

Third-party payment settlement organisations (TPSOs) refer to intermediaries such as PayPal, Venmo, Cash App, Stripe, Square, and Shopify, as well as apps like Airbnb, Uber, and Lyft. These platforms were impacted by the $600 reporting threshold, a provision under Biden's American Rescue Plan. This lowered threshold meant that TPSOs were required to report to the IRS and send tax paperwork for transactions totalling $600 or more over a year. This applied to all transactions, regardless of the number, impacting contractors, small businesses, and individuals using these platforms for personal transactions.

The $600 reporting threshold was an attempt by the IRS to monitor transactions, especially for freelancers and self-employed individuals. However, it was criticised for being invasive and causing unnecessary complications for TPSOs and their users. As a result, there was a delay in the implementation of this lower threshold, and the transition period was extended to facilitate a smoother adjustment for TPSOs and payees.

The delay in implementation meant that the existing 1099-K reporting threshold of $20,000 in payments from over 200 transactions remained in effect. This higher threshold benefits TPSOs, self-employed individuals, and small businesses, as they no longer need to report or comply with the more stringent $600 threshold.

It is important to note that while the $600 reporting threshold specifically targeted TPSOs, banks and financial institutions have separate reporting requirements. They are generally required to report cash purchases of cashier's checks, treasurer's checks, bank drafts, traveller's checks, and money orders exceeding $10,000. Additionally, any person or entity receiving over $10,000 in cash in a single transaction or related transactions must file a Form 8300.

Who Holds the Reins at the World Bank?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![]()

The rule would have applied to transactions from 2023 onwards

In 2021, the Internal Revenue Service (IRS) proposed a rule that would require financial institutions to report all transactions from personal and business accounts worth more than $600. This was part of the Biden Administration's American Families Plan. The proposal indicated that the administration would be flexible on raising the minimum account balance/inflow/outflow above $600.

The proposal faced criticism and opposition, with some calling it an "invasion of privacy" and a "bureaucratic nightmare". The Independent Community Bankers of America (ICBA) campaigned against the proposal, arguing that it would make banks report "all transactions" above the limit. However, it is important to note that the IRS would not have had information on all transactions, but rather aggregate numbers of gross inflows and outflows.

The rule would have impacted third-party settlement organizations (TPSOs) like PayPal, Venmo, and Cash App, as well as intermediaries used by small businesses and apps facilitating side gigs. It is worth noting that the $600 reporting threshold has since been scrapped, and the threshold has been restored to a more reasonable level of $20,000.

Best Banks Without Monthly Fees: A Comprehensive Guide

You may want to see also

Frequently asked questions

No, banks do not have to report $600 transactions. This was just a proposal by the Biden Administration as part of the American Families Plan, which did not pass.

No, banks do not have to report transactions over $600. This was a proposal by the Biden Administration to target low-income earners and small businesses, which did not pass.

Yes, banks have to report cash transactions over $10,000 by filing a Currency Transaction Report (CTR) with the Internal Revenue Service (IRS).

Yes, third-party payment settlement organizations (TPSOs) have to report transactions over $600 to the IRS. However, this rule has been delayed and is currently set to go into effect in 2025.

No, individuals do not have to report transactions over $600 on their taxes. However, it is always a good idea to keep records of all financial transactions in case of an audit.

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)