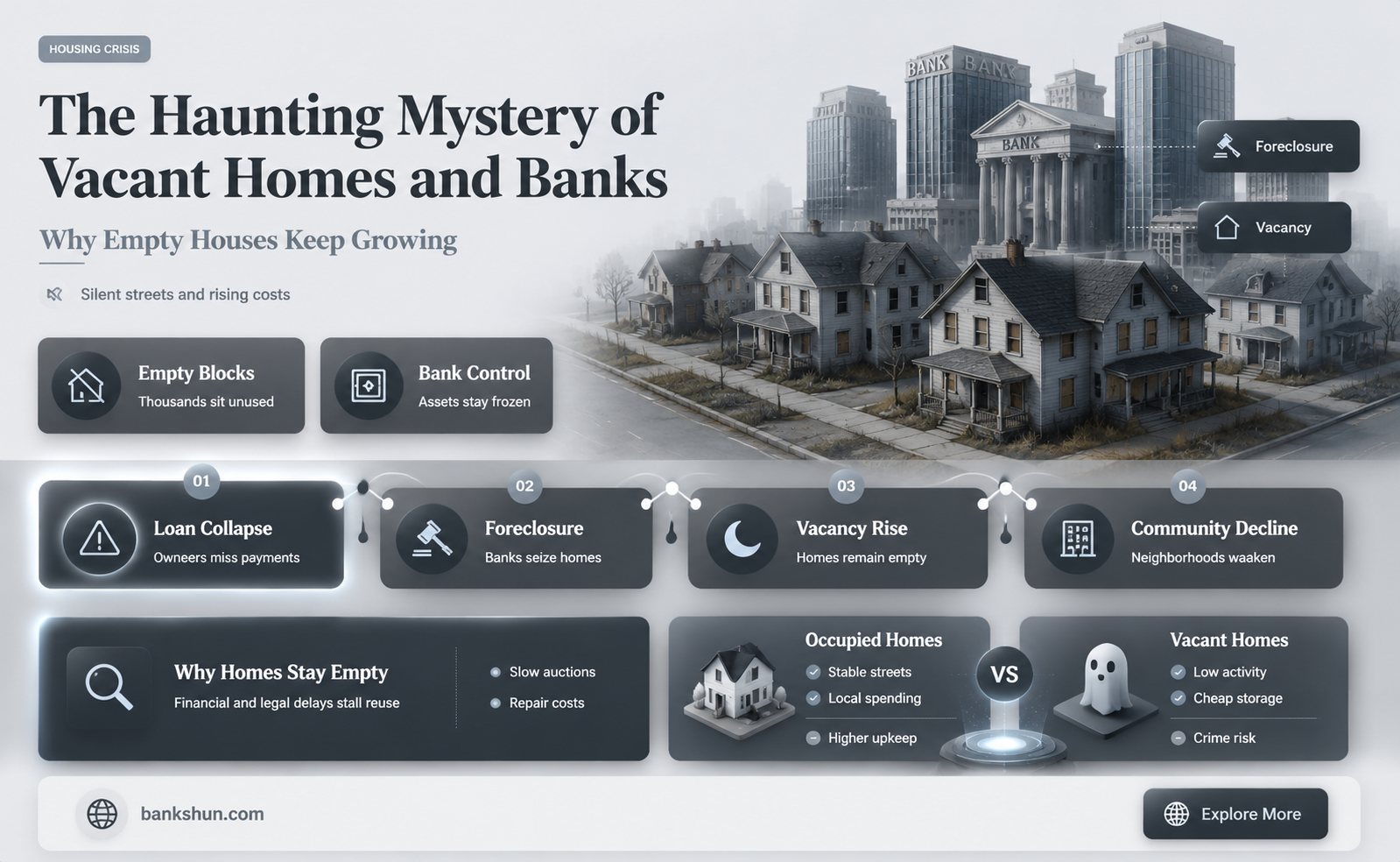

There is an ongoing debate about whether banks should be responsible for maintaining empty homes. While some argue that banks should ensure that vacant properties are secure and well-maintained, others believe that this responsibility should fall on the owners or the city. In some cases, banks have been accused of deceptive foreclosure practices, such as wrongfully locking people out of their homes and treating occupied homes as vacant. Additionally, banks may not have incentives to maintain empty homes, as they may not want to rush the selling process and may be able to claim these assets for leverage. On the other hand, vacant and abandoned properties can negatively impact local communities by lowering property values, attracting criminal activity, and creating health and safety hazards. As a result, some cities, like Chicago, have implemented ordinances that require lenders to secure and maintain abandoned properties. However, these regulations have faced legal challenges from the federal government and lenders, who argue that they unfairly shift the burden of responsibility.

| Characteristics | Values |

|---|---|

| Banks' responsibility for vacant homes | In Chicago, banks are required to secure and maintain vacant homes. However, the federal government is suing the city over this ordinance. |

| Challenges in determining vacancy | Lenders may face difficulties in establishing whether a property is vacant, as mentioned by Richard Gottlieb, who directs a financial industry group. |

| Deceptive foreclosure practices | There are reports of property preservation companies and field service companies treating occupied homes as vacant, resulting in abuses such as breaking into homes and removing occupants' belongings. |

| Impact on neighbourhoods | Bank-owned vacant homes can negatively affect neighbourhood values and attract undesirable activities, such as gang activity. |

| Delayed foreclosures | Banks may take a long time to complete foreclosures, contributing to the issue of vacant homes. |

| Financial considerations | Banks may have financial incentives to delay selling foreclosed homes, such as claiming assets for leverage and realising losses at a later date. |

Explore related products

What You'll Learn

![]()

The responsibility of maintaining empty homes

The issue of who is responsible for maintaining empty homes is a complex one, with various factors and stakeholders involved. It is a problem that many cities across the United States are grappling with, particularly in the wake of the 2008 financial crisis and the subsequent wave of foreclosures. While it may seem logical to place the onus on banks and lenders to secure and maintain vacant properties, the reality is often more nuanced.

In the past, the responsibility for maintaining empty homes fell solely on the owners. However, in recent years, cities like Chicago have implemented ordinances that require lenders to share the burden. Under Chicago's new rules, if a homeowner is delinquent on their mortgage payments for 45 days, the lender must inspect the property to determine if it has been abandoned. If the home is vacant, the lender is responsible for securing it, registering it with the city for a fee, and ensuring it meets city code standards. These regulations aim to address the issues of neglected, foreclosed properties that can attract criminal activity and negatively impact neighbourhoods.

However, this approach has also faced legal challenges. In Chicago's case, the federal government, on behalf of mortgage giants Fannie Mae and Freddie Mac, sued the city, arguing that lenders should not be held accountable before the property is legally theirs. Additionally, the financial industry has pushed back against these ordinances, claiming that determining whether a property is vacant is challenging and puts lenders in an impossible position.

The situation is further complicated by the involvement of property preservation companies, which work on behalf of lenders and servicers. While their role is to ensure that vacant properties in foreclosure are secure and properly maintained, these companies have been accused of committing abuses, such as breaking into occupied homes, stealing personal belongings, and damaging properties. Homeowners have legal recourse in such cases, and some states and local governments are taking steps to protect homeowners' rights and hold these companies accountable.

Ultimately, the responsibility for maintaining empty homes is a multifaceted issue that involves banks, lenders, government entities, and property preservation companies. While there is a growing recognition of the need to address the problem of neglected vacant homes, finding a balanced solution that protects all stakeholders' rights and ensures the safety and well-being of communities remains a challenge.

Grand Banks: Glacial Moraine Mystery

You may want to see also

Explore related products

![]()

The impact of vacant homes on neighbourhoods

Vacant homes can have a detrimental impact on neighbourhoods in several ways. Firstly, they can pose health and safety risks to residents. Vacant properties that are not properly secured can attract illegal activities such as gang activity, drug use, and prostitution, leading to increased crime rates and compromising the safety of the community. Additionally, vacant homes can contribute to the buildup of trash, attract rodents, and create an environment conducive to the growth of dangerous toxins such as mold, lead, and asbestos, posing risks to the physical health of those living nearby.

The presence of vacant homes can also have a negative impact on the mental health and well-being of residents. Visual reminders of neighbourhood disinvestment, such as boarded-up properties and overgrown lots, can cause anxiety, stigma, and a sense of fracture between neighbours. The perception of high vacancy rates can also affect community well-being by overshadowing positive aspects of the community and creating a sense of decline or failure to improve.

Vacant homes can also have economic implications for neighbourhoods. They lead to a decrease in property values, negatively impacting the financial assets and equity of homeowners in the area. This can result in higher insurance premiums or even policy cancellations for nearby residents due to the perceived instability of the neighbourhood. Additionally, vacant properties result in a reduction in property tax revenue for local governments, hindering their ability to provide essential resources and maintain infrastructure, further affecting the overall well-being of the community.

Furthermore, vacant homes can create challenges for property owners who struggle to maintain their homes due to financial strain. This can lead to a cycle of neglect and increased vacancies, as seen in areas facing urban blight. Addressing vacant homes requires a collaborative effort involving community organisations, residents, and local governments. Initiatives such as property tax reform, local land banks, code enforcement, and vacant building registries can help mitigate the negative impacts, but a comprehensive approach that tackles the root causes of vacancy is necessary for sustainable solutions.

Banking Websites: Tracking Your Mac Address?

You may want to see also

Explore related products

$26.99 $26.99

![]()

The role of property preservation companies

Property preservation companies play a critical role in the housing and mortgage lifecycle. They are hired by lenders or servicers to secure and maintain vacant properties during the foreclosure process and prepare them for returning to the market. This includes tasks such as changing locks, boarding up windows, and performing routine maintenance and repairs.

While property preservation companies are intended to protect vacant properties, they have been associated with several abuses against homeowners. There have been reports of property preservation workers breaking into occupied homes, stealing personal belongings, and causing damage. In some cases, they have also been accused of illegally locking occupants out of their homes and misrepresenting the occupants' rights. As a result of these abusive practices, homeowners have sought legal action against property preservation companies and their servicers.

To address these issues, some states and homeowners are taking steps to protect homeowners' rights. For example, the Attorney General of Illinois filed a lawsuit against the largest company in the industry for illegal practices, including breaking into occupied homes and removing personal property. Additionally, Maine has enacted a law specifically targeting the misconduct of property preservation companies.

To avoid legal issues and ensure compliance, property preservation companies must navigate complex regulatory requirements at the state, county, city, and township levels. They also face challenges due to market conditions, such as labour shortages, increasing costs, and declining inventories. Despite these challenges, the property preservation sector remains crucial for maintaining vacant properties and preventing urban blight.

Emergency Banking Relief Act: FDR's Quick Fix

You may want to see also

Explore related products

![]()

Deceptive foreclosure practices by banks

In response to the financial crisis and the surge in foreclosures, banks and their subcontractors have been scrutinized for their role in deceptive practices. Subcontractors, also known as field service companies, are responsible for determining the occupancy status of homes during delinquency. However, they have been known to inaccurately designate properties as vacant, leading to unlawful actions such as changing locks and removing occupants' possessions. This has resulted in legal battles, with the Attorney General of Illinois filing a lawsuit against the largest company in the industry for abuses, including illegal break-ins and misrepresentation to homeowners about their rights.

To address these issues, some cities have implemented ordinances holding lenders accountable for securing and maintaining vacant homes. Chicago, for instance, requires lenders to inspect properties if owners are delinquent on their mortgages for over 45 days. If the home is deemed abandoned, the lender must secure it, register it with the city, and maintain it according to city codes. This approach has sparked controversy, with the federal government suing Chicago on behalf of mortgage giants Fannie Mae and Freddie Mac, arguing that the city's regulations are unfair.

The deceptive foreclosure practices by banks have also been addressed through regulatory actions and legal defenses. Federal banking agencies conducted simultaneous reviews of the top fourteen servicers, identifying unsafe or unsound practices, including lax foreclosure documentation and ineffective controls. Additionally, legal defenses against foreclosure include challenging false affidavits submitted by banks, invoking state unfair and deceptive practices acts (UDAP), and utilizing the federal Fair Housing Act (FHA) to combat predatory lending practices.

While banks have a responsibility to protect their interests in properties during foreclosure, deceptive practices that harm homeowners cannot be condoned. The issues highlighted above have prompted legal, regulatory, and municipal responses, aiming to protect homeowners' rights and hold financial institutions accountable for their actions.

Bank Stocks: Effective Inflation Hedge?

You may want to see also

Explore related products

![]()

The legal obligations of banks regarding empty homes

According to the Chicago ordinance, if a homeowner is delinquent on their mortgage payments for up to 45 days, the lender must inspect the property to determine if it has been abandoned. If the home is found to be vacant, the lender is required to secure it, register it with the city for a fee, and maintain it according to city code. Non-compliance can result in hefty daily fines.

However, this ordinance has faced opposition from the federal government, which is suing Chicago on behalf of mortgage backers Fannie Mae and Freddie Mac. They argue that the city is unfairly requiring them to act as owners before the property is legally theirs and that Congress designated the Federal Housing Finance Agency (FHFA) as their sole regulator. The outcome of this legal dispute could set a precedent for other cities grappling with similar issues.

In general, when a homeowner defaults on their mortgage, the bank or lender has the right to initiate foreclosure proceedings and take possession of the property. At this point, most mortgages and deeds of trust grant the lender the authority to take reasonable and appropriate actions to protect their interest in the property. This includes securing and maintaining the vacant home to prevent damage and deterioration.

While banks have a responsibility to properly manage and dispose of foreclosed properties, there have been concerns about deceptive foreclosure practices and abuses committed by property preservation companies working on their behalf. These companies have been accused of breaking into still-occupied homes, wrongfully locking out homeowners, stealing personal belongings, and misrepresenting the rights of occupants. As a result, some states and homeowners are taking steps to protect the rights of homeowners and hold these companies accountable for their actions.

Who is Kaysan? Unraveling the Mystery of His Identity with Banks

You may want to see also

Frequently asked questions

Vacant homes are properties that have been abandoned by their owners, often due to foreclosure. These homes can fall into disrepair and create issues for the surrounding community, such as lowered property values and increased criminal activity.

Banks, as lenders, are responsible for securing and maintaining vacant homes in some cities, such as Chicago. This includes inspecting, registering, and maintaining the property to ensure it meets city codes and does not pose a safety risk to the community.

Banks may face challenges in determining whether a property is vacant, especially if the owner is only temporarily delinquent on mortgage payments. There are also financial considerations, as maintaining vacant homes can be costly, and banks may not have the incentive to incur these expenses.

If vacant homes are not properly maintained, they can have negative consequences for the surrounding community, including lowered property values, increased criminal activity, and health and safety hazards. In some cases, local governments may have to step in and incur additional costs to address these issues.

Local governments can implement ordinances that hold lenders responsible for securing and maintaining vacant properties. Homeowners can also take steps to communicate their occupancy status to lenders and seek legal assistance if they are wrongfully treated as vacant by their lender or property preservation companies.