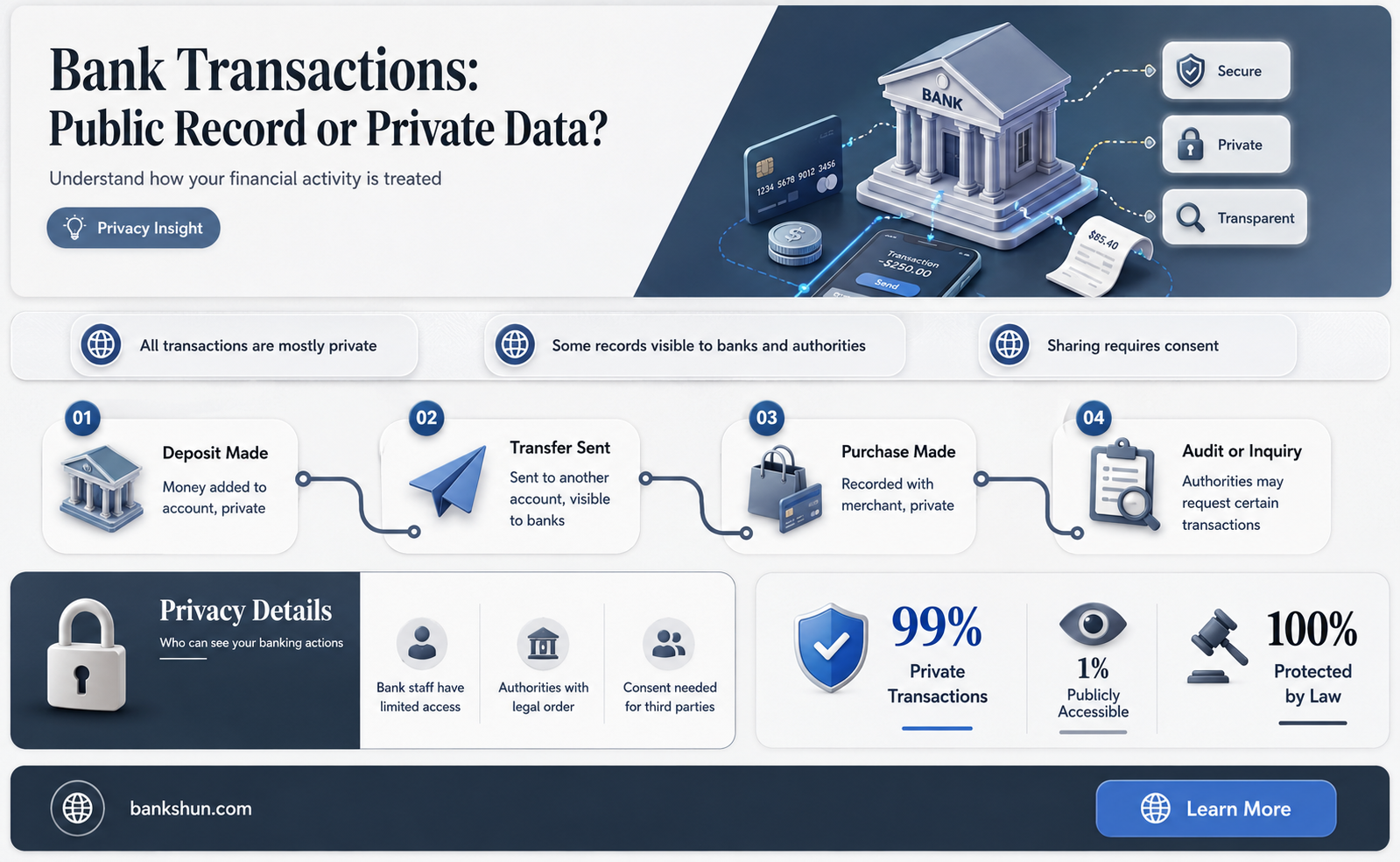

Banks are required to list every EFT transaction in their customers' monthly bank statements, including the dollar amount, the date the transaction cleared, and the name of the recipient. However, banks do not expose their primary or secondary databases to end users, and customers may have to pay a fee to access their full transaction history. In the United States, the Gramm-Leach-Bliley Act of 1999 prohibits financial institutions from disclosing consumers' nonpublic personal information to unaffiliated third parties. However, banks are allowed to share information with various types of third-party vendors, including financial companies, retailers, and government agencies.

| Characteristics | Values |

|---|---|

| Bank's obligation to list transactions | Banks are required to list every EFT transaction in monthly statements, including the amount, date, and recipient. |

| Customer access to transaction history | Customers can usually access their transaction history online, but the range of data available may be limited. Some banks may charge a fee for providing a file with a more extended history. |

| Customer privacy | Banks are prohibited from disclosing nonpublic personal information to unaffiliated third parties for marketing purposes. However, exceptions exist, and customers may not opt out of all information sharing. |

| Paper checks | Banks are not legally required to provide customers with their canceled checks. However, customers can request copies of specific checks or their canceled checks, and banks will usually be able to provide them. |

| Reporting large cash transactions | Banks must report cash purchases of certain financial instruments, such as cashier's checks and money orders, exceeding $10,000 by filing currency transaction reports. |

Explore related products

What You'll Learn

![]()

Banks must list every EFT transaction on monthly statements

Banks are required to list every Electronic Funds Transfer (EFT) transaction in their customers' monthly bank statements. This includes the dollar amount, the date the transaction cleared, and the name of the recipient. Electronic transactions may be grouped together, separate from regular check transactions. This allows customers to track their EFT payments and verify that they have been executed correctly.

EFT tracking involves monitoring electronic funds transfers between bank accounts. It uses unique identifiers, like trace numbers or transaction IDs, to monitor the payment from start to finish. This ensures that funds are transferred accurately and allows for verification of the transaction's status. This tracking helps both businesses and individuals confirm that transactions are processed accurately and efficiently. It also assists in resolving any issues that may arise, such as delays or errors in payment.

While banks are required to list EFT transactions, they are not obligated to provide customers with their cancelled checks or even copies of them. In some cases, banks may provide substitute checks, which are special paper copies created under the Check 21 Act. These substitute checks serve as legal proof of payment, just like the original check.

It is important to note that customers have the right to dispute any mistakes or unauthorized transactions on their bank statements. Banks are required to investigate reported errors and temporarily credit the disputed amount while conducting their investigation.

The West Bank: Home to Palestinians?

You may want to see also

Explore related products

![]()

Customers can request copies of original or cancelled checks

Banks are not required to send customers their cancelled checks or check images. If you receive your checks or copies of checks, that is usually because of your customer agreement with your bank and your bank's policies. Many consumers do not receive their checks or even copies of their checks.

However, customers can request copies of original or cancelled checks from their bank. In most cases, the bank will be able to provide a copy of the check. However, the bank might not always be able to, especially if the check was processed electronically, in which case the original paper check is typically destroyed.

If a customer requests their original check from their bank, the bank may provide them with the original check, a substitute check, or a copy of the check. A substitute check is a special paper copy created under the Check 21 Act, using images of the front and back of an original check. It is legally the same as the original check and can be used as proof of payment. Banks must provide customers with a disclosure about substitute checks when they request an original or copy of a check and receive a substitute check.

It is important to note that even without a cancelled check, customers can prove they made a payment with their bank statement, which shows the date and amount of the payment. They might also have a receipt from a retail transaction. The law does not require customers to have the original paper check, or even a copy of it, to resolve a problem with a bank.

Are B. Simone and Desi Banks More Than Friends?

You may want to see also

Explore related products

![]()

Banks can share personal information with third-party vendors

Banks can and do share personal information with third-party vendors. This is done for business and marketing purposes. The third-party vendors that banks share personal information with are also regulated. They include financial companies like mortgage bankers, securities brokers-dealers, and insurance agents; retailers (e.g. home improvement stores), magazine publishers, airline companies, and direct marketers; companies that deliver services on behalf of the lender (e.g. mortgage servicers), and government agencies and nonprofits. Banks are prohibited from providing nonpublic information to any person or company that is not affiliated with the bank, such as car dealers.

The primary law that governs how banks can share personal information about consumers is the Gramm-Leach-Bliley (GLB) Act of 1999, which prohibits the disclosure of certain private information like Social Security numbers, income, and some outstanding debt. The Act, which is federally mandated, consists of three sections: the Financial Privacy Rule, which regulates the collection and disclosure of private information; the Safeguards Rule, which requires financial institutions to protect the confidentiality and security of nonpublic personal information; and the Limits on Reuse and Rediscovery Rule, which limits the reuse and redisclosure of nonpublic personal information received from a nonaffiliated financial institution or disclosed to a nonaffiliated third party.

The GLB Act seeks to protect consumer financial privacy. Its provisions limit when a "financial institution" may disclose a consumer's "nonpublic personal information" to nonaffiliated third parties. The law covers a broad range of financial institutions, including many companies not traditionally considered to be financial institutions because they engage in certain "financial activities." Financial institutions must notify their customers about their information-sharing practices and tell consumers of their right to "opt-out" if they don't want their information shared with certain nonaffiliated third parties.

There are exceptions to the opt-out rule. First, the privacy rule does not govern information sharing among affiliated parties. Second, the rule contains exceptions to allow transfers of nonpublic personal information to unaffiliated parties to process and service a consumer's transaction, and to facilitate other normal business transactions. For example, consumers cannot opt out when nonpublic personal information is shared with a nonaffiliated third party to market the bank's own financial products or services, market financial products or services offered by the bank and another financial institution (joint marketing), process and service transactions the consumer requests or authorizes, or protect against potential fraud or unauthorized transactions.

Reversing Bank Wire Transfers: Is It Possible?

You may want to see also

Explore related products

![]()

Banks must comply with privacy rules set by supervisory agencies

Banks are entrusted with their customers' personal and financial information, and as such, they are expected to protect their customers' privacy. While the Federal Deposit Insurance Corporation (FDIC) rule only applies to certain banks and some of their subsidiaries, all financial institutions must comply with similar privacy rules set by their supervisory agencies. These supervisory agencies include the Federal Trade Commission (FTC), the Federal Reserve Board, the Office of Thrift Supervision, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the National Credit Union Administration, the Securities and Exchange Commission, and the Commodity Futures Trading Commission.

The privacy rule protects "consumers," and all consumers are entitled to the same privacy protections. However, a subset of consumers defined as "customers" must receive certain disclosures, such as an annual privacy notice, that need not be provided to consumers who are not customers. A customer is a consumer with whom a bank has a continuing relationship. A continuing relationship is established when a consumer typically receives some measure of continued service following, or in connection with, a transaction. Examples of transactions that are considered continuing relationships include when consumers obtain a deposit account, obtain a loan, or obtain an investment advisory service.

The privacy rule embodies two principles: notice and opt-out. All banks must develop initial and annual privacy notices, even if they do not share information with nonaffiliated third parties. The notices must describe the bank's information-sharing practices. Banks that share nonpublic personal information about consumers with nonaffiliated third parties (outside of opt-out exceptions delineated in the privacy rule) must also provide consumers with a description of their information-sharing practices and a list of the parties that receive the shared information. The privacy rule prohibits banks from disclosing an account number or access code for credit card, deposit, or transaction accounts to any nonaffiliated third party for marketing use. However, there are two exceptions to this rule. Banks may share account numbers when marketing their own products, as long as the service provider is not authorized to directly initiate charges to the accounts. They may also disclose account numbers to participants in a private label or affinity credit card program when the participants are identified to the customer.

There are exceptions to the opt-out, where a consumer cannot opt out of all information sharing. The privacy rule contains exceptions to allow transfers of nonpublic personal information to unaffiliated parties to process and service a consumer's transaction, to facilitate other normal business transactions, and to protect against potential fraud or unauthorized transactions. A bank may have to satisfy disclosure and other requirements to make the rule's opt-out exceptions applicable.

The Education Banking System: A Financial Model for Learning

You may want to see also

Explore related products

![]()

Banks don't expose primary databases to end users

Banks are required to list every EFT transaction in their customers' monthly bank statements, including the dollar amount, the date the transaction cleared, and the name of the recipient. However, there is no requirement for banks to send cancelled cheques to their customers. If a customer receives their cheques or copies of cheques, it is usually due to their customer agreement with the bank and the bank's policies.

Banks do not expose their primary (or secondary) databases to end users. They only store a limited number of days of data in the customer-facing database and restrict the range of any one query. This is to prevent system-wide slowness and to ensure that the database is not overwhelmed by millions of customers' transactions. Banks do maintain database archives, which are kept offline, and employee-facing databases, which allow employees to query larger ranges of data.

From a security standpoint, it is generally advised not to expose primary keys to end users. This is because, if exposed, users may start to use the primary key as their 'account number', which it is not. Additionally, if the primary key is the user's personal information, it should not be exposed to anyone other than the user. Exposing primary keys may also allow people to find out information that they should not know, such as the demographics of a user base or the exact number of users on a website.

Furthermore, the cost of storing large amounts of data is high, and banks would have to pay even more to store thousands of backups of the same data. Banks also have to consider the complexity of their systems, which may involve multiple data centres, apps, business lines, and legacy systems, each with their own database.

What Laws Govern Banks?

You may want to see also

Frequently asked questions

Banks are required to list every EFT transaction in your monthly statement, including the dollar amount, date, and recipient. However, they don't expose their primary or secondary database to end users, and you may have to pay a fee to access your full transaction history.

No law requires your bank to send you your cancelled cheques. If you receive them, it is due to your customer agreement with your bank and their policies. You can request copies of specific original or cancelled cheques, and your bank will usually be able to provide them.

Banks are required to have processes in place to protect the personal information they collect, use, and share with third parties. The primary law that governs this is the Gramm-Leach-Bliley Act of 1999, which prohibits the disclosure of nonpublic personal information to unaffiliated companies. However, there are exceptions, and consumers cannot opt out of all information sharing.