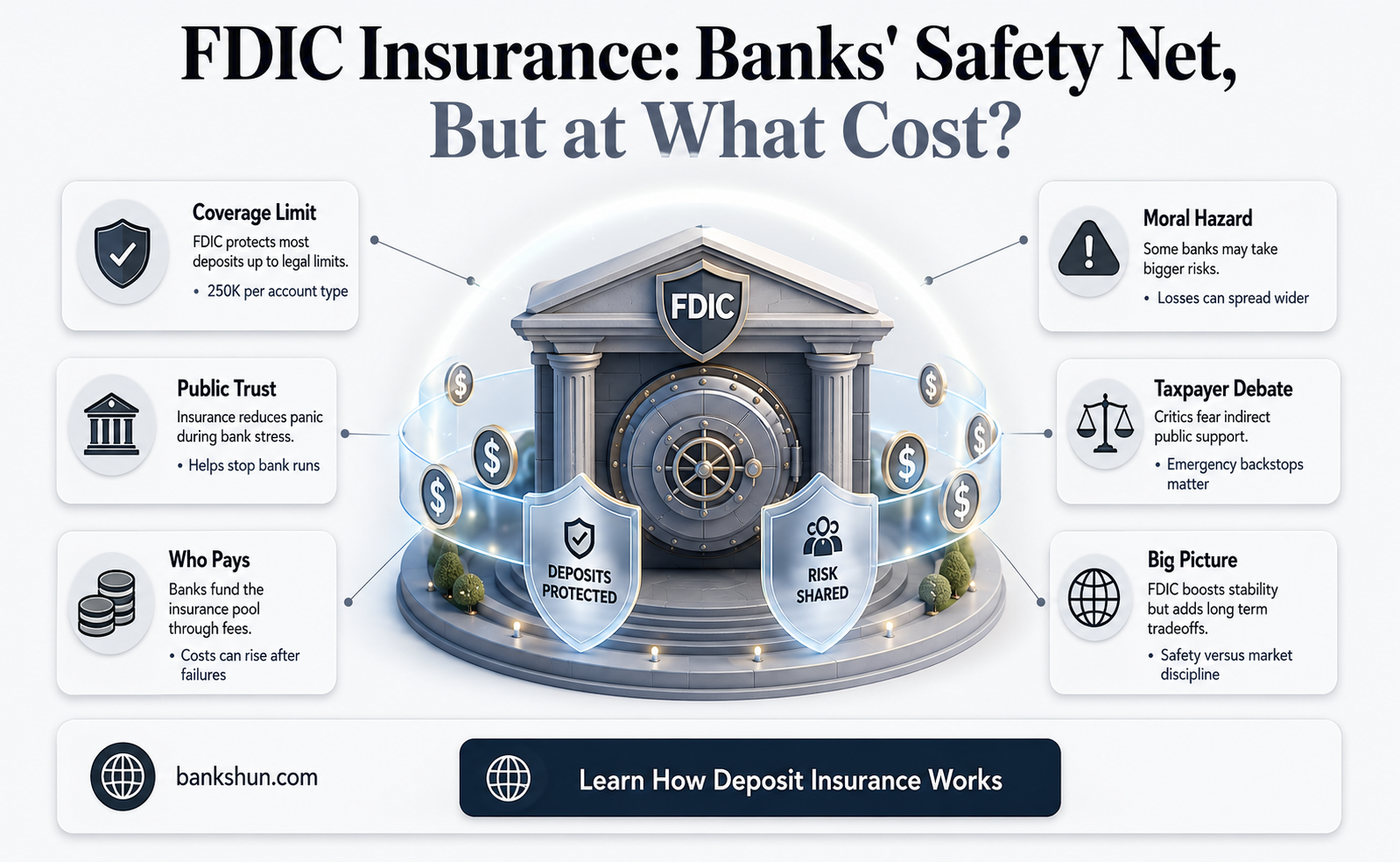

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank customers in the event of a bank failure. FDIC insurance is not free for banks; they apply for FDIC insurance and pay premiums for it. The amount of each bank's premiums is based on its balance of insured deposits and the degree of risk that it poses to the FDIC. The FDIC uses these premiums to pay its operating costs and the depositors of failed banks.

| Characteristics | Values |

|---|---|

| Who pays for FDIC insurance? | Banks pay for FDIC insurance through premiums. |

| Who does FDIC insurance cover? | FDIC insurance covers bank customers with deposit accounts at an FDIC-insured bank. |

| What does FDIC insurance cover? | FDIC insurance covers deposits in all types of accounts at FDIC-insured banks, up to [$250,000] per depositor, per FDIC-insured bank, for each account ownership category. |

| What does FDIC insurance not cover? | FDIC insurance does not cover non-deposit investment products, even those offered by FDIC-insured banks. It also does not cover default or bankruptcy of any non-FDIC-insured institution. |

| How does FDIC insurance work? | FDIC insurance protects bank customers' funds in the event that an FDIC-insured bank fails. The FDIC steps in to pay affected customers up to the insurance limit and assume control of the assets and debts of the bank. |

| How is FDIC funded? | The FDIC is funded through premiums assessed on each member bank, which are accumulated in a Deposit Insurance Fund (DIF). The DIF is invested in Treasury securities, earning interest to supplement the premiums. |

| Is FDIC insurance mandatory for banks? | Banks are not insured by default and must apply for FDIC insurance. |

Explore related products

What You'll Learn

![]()

FDIC insurance protects customers' funds if their bank collapses

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank customers against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. FDIC deposit insurance protects bank customers in the event that an FDIC-insured depository institution fails. Bank customers don’t need to purchase deposit insurance; it is automatic for any deposit account opened at an FDIC-insured bank.

FDIC deposit insurance only covers certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). It does not cover non-deposit investment products, even those offered by FDIC-insured banks. Additionally, FDIC deposit insurance doesn’t cover default or bankruptcy of any non-FDIC-insured institution.

FDIC insurance covers deposits in all types of accounts at FDIC-insured banks, up to at least $250,000 per depositor, per FDIC-insured bank, per ownership category. For example, if a customer had a CD account in her name alone with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured. Deposit insurance is calculated dollar-for-dollar, principal plus any interest accrued or due to the depositor, through the date of default.

Historically, the FDIC pays insurance within a few days after a bank closing, usually the next business day. The FDIC assumes the task of selling/collecting the assets of the failed bank and settling its debts, including claims for deposits in excess of the insured limit. If a depositor has uninsured funds (i.e., funds above the insured limit), they may recover some portion of their uninsured funds from the proceeds from the sale of failed bank assets. However, it can take several years to sell off the assets of a failed bank. As assets are sold, depositors who had uninsured funds usually receive periodic payments on a pro-rata basis on their remaining claim.

Foreign Currency Exchange: Bank Charges and Alternatives

You may want to see also

Explore related products

![The Complete Code Of Federal Regulations Title 12 - BANKS AND BANKING - FDIC, HUD, AND MORE [ALL VOLUMES] 2016](https://m.media-amazon.com/images/I/419WdrnOfrL._AC_UY218_.jpg)

![]()

Banks pay premiums for FDIC insurance

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. FDIC deposit insurance protects bank customers in the event that an FDIC-insured depository institution fails. Bank customers don’t need to purchase deposit insurance; it is automatic for any deposit account opened at an FDIC-insured bank.

The FDIC receives no funding from the federal budget. Instead, it assesses premiums on each member institution, which are accumulated in a Deposit Insurance Fund (DIF) that it uses to pay its operating costs and the depositors of failed banks. The amount of each bank's premiums is based on its balance of insured deposits and the degree of risk that it poses to the FDIC. The DIF is fully invested in Treasury securities and therefore earns interest that supplements the premiums. Under the Dodd–Frank Act of 2010, the FDIC is required to fund the DIF to at least 1.35% of all insured deposits.

The FDIC deposit insurance covers $250,000 per depositor, per FDIC-insured bank, for each account ownership category. All of a depositor's deposits in the same ownership category in the same FDIC-insured bank are added together for the purpose of determining FDIC deposit insurance coverage. For example, a revocable trust account (including living trusts and informal revocable trusts commonly referred to as payable on death (POD) accounts) with one owner naming three unique beneficiaries can be insured up to $750,000.

The FDIC's assessment rates decrease for the issuance of long-term unsecured debt and increase for holdings of long-term unsecured or subordinated debt issued by other insured banks. For large banks that are not well-rated or not well-capitalized, assessment rates increase for significant holdings of brokered deposits. Large banks (generally, those with $10 billion or more in assets) are assigned an individual rate based on a scorecard. The scorecard combines CAMELS component ratings, financial measures used to estimate a bank's ability to withstand asset-related and funding-related stress, and a measure of loss severity that estimates the relative magnitude of potential losses to the FDIC in the event of the bank's failure.

Cheque Writing: Red Ink and Bank Acceptance

You may want to see also

Explore related products

![]()

FDIC insurance covers deposits in all types of accounts

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance covers deposits in all types of accounts at FDIC-insured banks, but it does not cover non-deposit investment products, even those offered by FDIC-insured banks. FDIC deposit insurance also does not cover the default or bankruptcy of any non-FDIC-insured institution.

FDIC deposit insurance covers $250,000 per depositor, per FDIC-insured bank, for each account ownership category. All deposits in the same ownership category in the same FDIC-insured bank are added together for the purpose of determining FDIC deposit insurance coverage. However, you may qualify for more than $250,000 in FDIC deposit insurance coverage if you deposit money in accounts that are in different ownership categories. For example, if you have a single ownership account at an FDIC-insured bank and a joint ownership account with one or more people at the same bank, you will be insured for up to $250,000 for your single ownership account deposits. You will also be insured for up to $250,000 for the combined balance of the funds in the joint ownership account.

FDIC deposit insurance is automatic for any deposit account opened at an FDIC-insured bank. Bank customers don't need to purchase deposit insurance. To determine if a bank is FDIC-insured, you can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool.

The FDIC receives no funding from the federal budget. Instead, it assesses premiums on each member and accumulates them in a Deposit Insurance Fund (DIF) that it uses to pay its operating costs and the depositors of failed banks. The amount of each bank's premiums is based on its balance of insured deposits and the degree of risk that it poses to the FDIC. The DIF is fully invested in Treasury securities and earns interest to supplement the premiums.

Coin Counting: US Bank's Services and Solutions

You may want to see also

Explore related products

![]()

FDIC insurance doesn't cover non-deposit investment products

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event of an FDIC-insured bank or savings association failure. FDIC insurance is backed by the full faith and credit of the US government. Banks have to pay insurance premiums to the FDIC, which are accumulated in a Deposit Insurance Fund (DIF) that the FDIC uses to pay its operating costs and the depositors of failed banks.

FDIC deposit insurance covers deposits in all types of accounts at FDIC-insured banks, but it does not cover non-deposit investment products, even if they are offered by FDIC-insured banks. Non-deposit investment products include mutual funds, annuities, life insurance policies, and stocks and bonds. These products are not insured by the FDIC because their value can go up or down depending on market demand, so investors could lose the money they invested or not gain as much profit as expected.

When shopping for a non-deposit investment product, investors should consider their investment goals and objectives, financial and tax status, risk tolerance, and time horizon for their investment portfolio. Sales representatives of these products must make certain disclosures orally and/or in writing to inform customers if the product is covered by FDIC insurance.

To determine if a bank is FDIC-insured, individuals can ask a bank representative, look for the FDIC sign at the bank, or use the FDIC's BankFind tool, which provides detailed information about all FDIC-insured institutions.

The Real-Life Bank Behind the Margin Call Movie

You may want to see also

Explore related products

![]()

FDIC insurance doesn't cover non-bank institutions

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government.

FDIC deposit insurance covers deposits in all types of accounts at FDIC-insured banks, but it does not cover non-deposit investment products, even those offered by FDIC-insured banks. This means that FDIC insurance does not cover default or bankruptcy of any non-FDIC-insured institution.

FDIC deposit insurance only covers deposits, and only if your bank is FDIC-insured. To determine if a bank is FDIC-insured, you can ask a bank representative, look for the FDIC sign at your bank, or use the FDIC's BankFind tool. BankFind allows you to access detailed information about all FDIC-insured institutions, including branch locations, the bank's official website, and the current operating status of the bank.

FDIC insurance covers $250,000 per depositor, per FDIC-insured bank, for each account ownership category. However, you may qualify for more than $250,000 in FDIC deposit insurance coverage if you deposit money in accounts that are in different ownership categories. For example, if you have a single ownership account at an FDIC-insured bank and a joint ownership account with one or more people at the same bank, you will be insured for up to $250,000 for your single ownership account deposits and also insured separately for your ownership interest up to $250,000 for all of your joint ownership account deposits.

The Board of Governors: Where is its Location?

You may want to see also

Frequently asked questions

Yes, banks have to pay for FDIC insurance. The FDIC (Federal Deposit Insurance Corporation) assesses premiums on each member institution, which are then accumulated in a Deposit Insurance Fund (DIF) that is used to pay operating costs and depositors of failed banks.

The amount of the premium is based on the bank's balance of insured deposits and the degree of risk that the bank poses to the FDIC.

FDIC insurance protects your money in the event of a bank failure. If your bank fails, the FDIC steps in to protect your funds, either by paying you directly or by arranging for a healthy bank to acquire the failed bank and assuming your deposits.

FDIC insurance covers up to \$250,000 per depositor, per FDIC-insured bank, for each account ownership category.