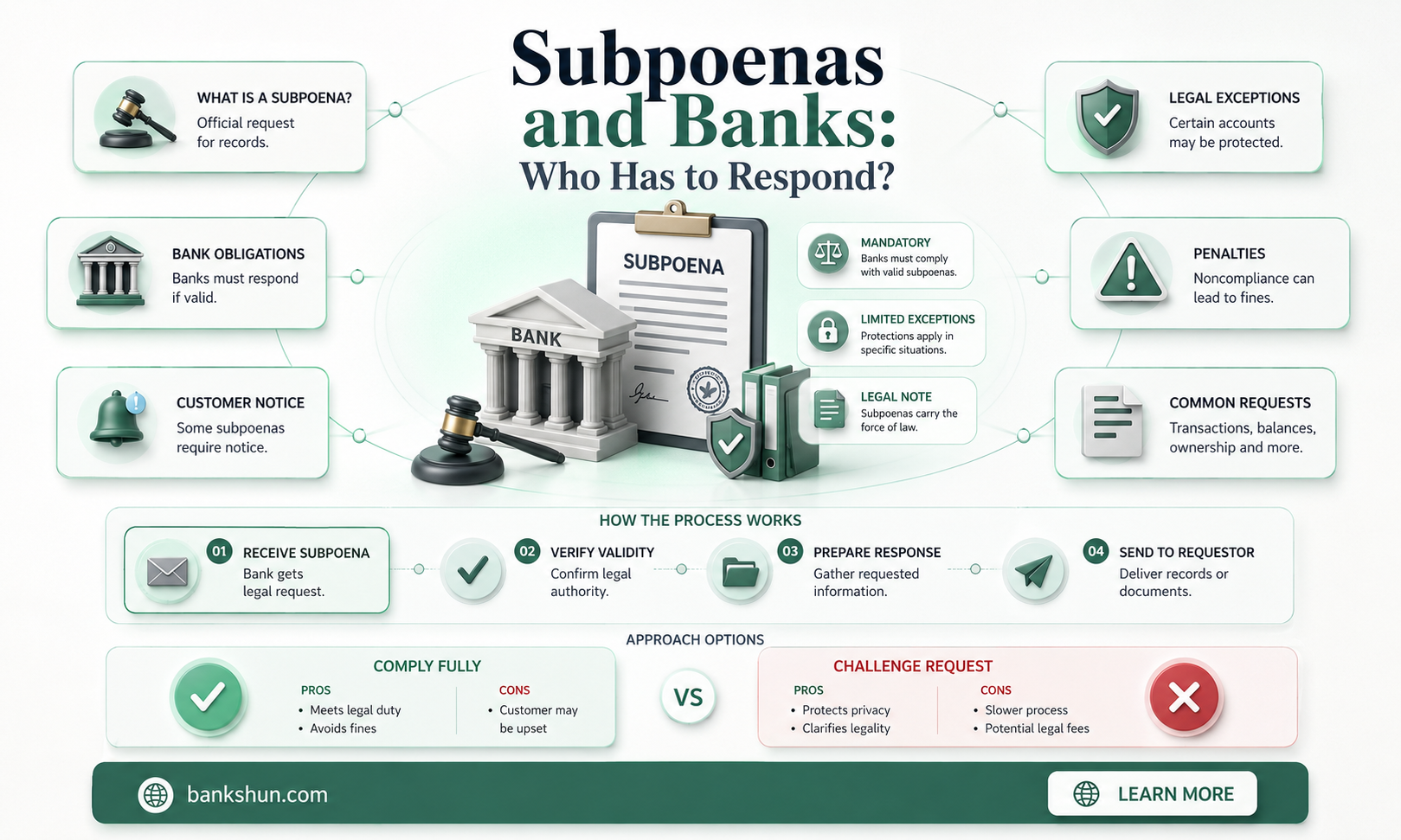

Banks are required to respond to subpoenas, which are legal documents that require the production of documents, testimony, or other evidence. Compliance with subpoenas is mandatory, and failure to respond appropriately can result in serious consequences, including fines or even contempt of court. Banks must comply with subpoenas unless they have valid objections, such as protecting customer privacy and confidentiality. They must also ensure compliance with privacy laws and regulations when responding to subpoenas, especially when dealing with confidential and privileged information such as customer account information. The procedure for responding to a subpoena includes identifying who will handle the response, preserving relevant documents, determining deadlines, and asserting objections or producing responsive documents. Understanding the intricacies of bank subpoena procedures is essential for compliance with legal requirements and ensuring the proper steps are taken to obtain relevant financial information.

| Characteristics | Values |

|---|---|

| Duty to respond | Banks have a duty to respond to subpoenas to maintain confidentiality and protect customer information |

| Compliance | Compliance with subpoenas is mandatory and failure to respond can result in fines or legal sanctions |

| Privacy | Banks must comply with privacy laws and regulations to protect customer data |

| Exceptions | Banks can refuse to disclose Suspicious Activity Reports (SARs) unless requested by federal, state or local law enforcement agencies |

| Objections | Banks can object to subpoenas if they believe they are overly broad, unduly burdensome or violate customer privacy rights |

| Notification | Banks are prohibited from notifying customers of a grand jury subpoena in certain situations |

| Scope | Subpoenas should only request information relevant to the litigation |

Explore related products

What You'll Learn

- Banks must respond to subpoenas unless they have valid objections

- Failure to respond can result in fines or legal sanctions

- Banks must protect customer information and comply with privacy laws

- Subpoenas are legal documents that require the production of documents

- Third-party subpoenas are served on a non-involved financial institution

![]()

Banks must respond to subpoenas unless they have valid objections

Banks are often faced with subpoenas, which are legal documents requesting financial information. Banks have a duty to maintain the confidentiality of their customers' financial information. In the absence of clear and specific consent from the customer, banks should not disclose financial information to anyone who is not a customer unless required by law.

Subpoenas are part of the judicial process, but there is case law that ignores the general exemption and instead limits the scope of the subpoena. Banks must respond to subpoenas unless they have valid objections. For example, banks can challenge a subpoena if it is overly broad, unduly burdensome, or violates customer privacy rights.

Upon receiving a subpoena, banks should determine whether a governmental authority issued it. If a federal government authority issued the subpoena, the Right to Financial Privacy Act (RFPA) applies, and the government must notify the customer and produce a certificate of compliance with RFPA before the bank complies. If a local or state authority issues the subpoena, the Gramm-Leach-Bliley Act (GLBA) applies, and the bank will likely have to answer without notifying the customer.

It is crucial for banks to have robust procedures in place to handle subpoenas promptly and efficiently. Banks must review subpoenas and respond accordingly, which may involve producing the requested documents or appearing in court to explain any objections. Compliance with subpoenas is mandatory, and failure to respond appropriately can result in penalties such as fines or legal sanctions.

To ensure compliance, banks should follow certain procedures when responding to subpoenas. These include identifying who will handle the subpoena response, preserving relevant documents and information, determining applicable deadlines, and asserting objections or producing responsive documents.

The Emergency Banking Act: A Presidential Authorization

You may want to see also

Explore related products

$18.49 $19.95

$12.61 $25.99

![]()

Failure to respond can result in fines or legal sanctions

Subpoenas are legally binding documents that require a response, even if it is just to challenge the subpoena. They are part of the judicial process and can be issued by a judge, clerk, or U.S. attorney. Failure to respond to a subpoena, especially one from a court, can result in being held in contempt, which may lead to fines or other legal sanctions.

In the context of banks and financial institutions, there are specific considerations to keep in mind. For example, the Bank Secrecy Act prohibits financial institutions from disclosing Suspicious Activity Reports (SARs) in response to subpoenas, with certain exceptions for law enforcement and regulatory agencies. Additionally, banks must navigate between complying with subpoenas and protecting customer privacy. In some cases, banks may be prohibited from notifying their customers about subpoenas, especially in grand jury investigations.

While some subpoenas can be challenged, this should be done with the assistance of an attorney. It is important to note that ignoring a subpoena is not advisable and can have legal consequences. If an individual or entity fails to respond, the court can issue a warrant and take further legal action to ensure compliance.

The consequences of ignoring a subpoena can vary depending on the jurisdiction and the nature of the subpoena. In Florida, for example, there is a greater emphasis on protecting an individual's right to privacy, which may impact how subpoenas are handled. Nonetheless, failing to respond to a subpoena without a valid reason can still result in legal repercussions, even if the specifics may differ across states.

In summary, failure to respond to a subpoena can indeed result in fines or legal sanctions. It is important to take subpoenas seriously and, if necessary, seek legal advice to ensure compliance or challenge the subpoena through the appropriate channels.

Tyra Banks' Fresh Prince of Bel-Air Cameo

You may want to see also

Explore related products

![]()

Banks must protect customer information and comply with privacy laws

Banks have a responsibility to protect their customers' information and comply with privacy laws. The Gramm-Leach-Bliley Act (GLBA) requires financial institutions to notify customers about their information-sharing practices and their right to "opt-out" of certain information-sharing with non-affiliated third parties. The GLBA also requires financial institutions to provide consumers with a privacy notice disclosing that a consumer's nonpublic personal information (NPI) is being shared with non-affiliated third parties.

The Federal Trade Commission (FTC) has outlined the Privacy Rule, which applies to financial institutions and businesses that are "significantly engaged" in "financial activities." The Privacy Rule protects nonpublic personal information and requires banks to develop initial and annual privacy notices, even if they do not share information with non-affiliated third parties. The content of these notices includes categories of information collected, disclosed, and shared with affiliates and non-affiliates, as well as information-sharing practices about former customers.

The Right to Financial Privacy Act (RFPA) was enacted in 1978 to protect the privacy of customers' financial records and limit government agencies' access to these records. The RFPA establishes procedures that government authorities must follow when requesting a customer's financial records and imposes requirements on financial institutions before releasing this information.

To comply with privacy laws, banks must also adhere to the Bank Secrecy Act, which prohibits financial services companies from disclosing Suspicious Activity Reports (SARs) or any information that would reveal their existence in response to civil litigation subpoenas. Additionally, banks should be aware of state laws that may provide greater consumer protection than federal privacy rules, as they are obligated to comply with the provisions of those state laws.

In conclusion, banks must prioritize protecting their customers' information and comply with relevant privacy laws and regulations to maintain trust and ensure the security of sensitive financial data.

Coin Counting: Banks and Their Machines

You may want to see also

![]()

Subpoenas are legal documents that require the production of documents

In the United States, subpoenas for bank records are governed by specific laws and regulations, including the Right to Financial Privacy Act (RFPA), the Gramm-Leach-Bliley Act (GLBA), and the Bank Secrecy Act (BSA). The RFPA and the GLBA require banks to notify customers about subpoenas, while the BSA prohibits banks from disclosing Suspicious Activity Reports (SARs) in response to subpoenas.

When a bank receives a subpoena, it should first determine if a governmental authority issued it. If the subpoena is from a federal agency, the RFPA applies, and the government must provide notice to the customer and a certificate of compliance to the bank. If a local or state authority issues the subpoena, the GLBA applies, and the bank may have to comply without notifying the customer.

To protect customer privacy, banks can challenge subpoenas that are overly broad or violate privacy rights. Banks should also ensure that subpoenas are properly served and enforceable before providing any information. Compliance with subpoenas is mandatory, and failure to respond appropriately can result in penalties, including fines or legal sanctions.

The procedure for responding to a subpoena includes identifying a designated team to handle the response, preserving relevant documents, determining deadlines, and producing the requested documents or appearing in court to address objections. Banks should also work with their legal teams and business partners to prepare for any required testimony.

Promissory Notes: Are Banks Legally Bound to Accept Them?

You may want to see also

![]()

Third-party subpoenas are served on a non-involved financial institution

In the United States, subpoenas are part of the judicial process. They are commonly used to obtain confidential and privileged information, such as customer account information and records kept by financial institutions for regulatory purposes.

When a third-party subpoena is served on a non-involved financial institution, the institution should first determine whether the subpoena was issued by a governmental authority. If the subpoena was issued by the federal government, the Right to Financial Privacy Act (RFPA) applies, and the government must notify the customer and provide a certificate of compliance with the RFPA to the institution before the institution can comply. On the other hand, if a local or state authority issues the subpoena, the Gramm-Leach-Bliley Act (GLBA) applies, and the bank will likely have to answer the subpoena without notifying the customer.

It is important to note that financial institutions are not always required to comply with subpoenas. For example, the Bank Secrecy Act prohibits financial services companies from disclosing Suspicious Activity Reports (SARs) or any information that would reveal the existence of a SAR in response to a subpoena. Additionally, financial institutions must comply with applicable privacy laws and regulations, such as the GLBA, which provides certain protections for customer financial information.

In some cases, financial institutions may object to a subpoena if it is deemed unreasonable or oppressive. For example, in Florida, an objection to a subpoena issued upon a bank must be raised promptly, and the court may quash or modify the subpoena if it is deemed unreasonable or oppressive. Similarly, in California, a non-party deponent may refuse to comply with a deposition subpoena, but they may be held in contempt of court and be subject to paying damages.

Overall, while financial institutions are generally required to respond to subpoenas, there are certain exceptions and protections in place to safeguard customer privacy and confidential information.

Bank Wire Inactivity: When Do Canceled Wires Occur?

You may want to see also

Frequently asked questions

Subpoenas are legal documents that require the production of documents, testimony, or other evidence.

Banks must comply with subpoenas unless they have valid objections. Failure to respond appropriately can result in serious consequences, including fines or legal sanctions.

Banks may object to a subpoena if they believe it violates customer privacy rights, is overly broad, or unduly burdensome.

The bank must review the subpoena and respond accordingly, which may involve producing the requested documents or appearing in court to explain any objections.

Banks should have robust procedures in place to handle subpoenas promptly and efficiently. They should also ensure compliance with privacy laws and regulations to protect customer data.