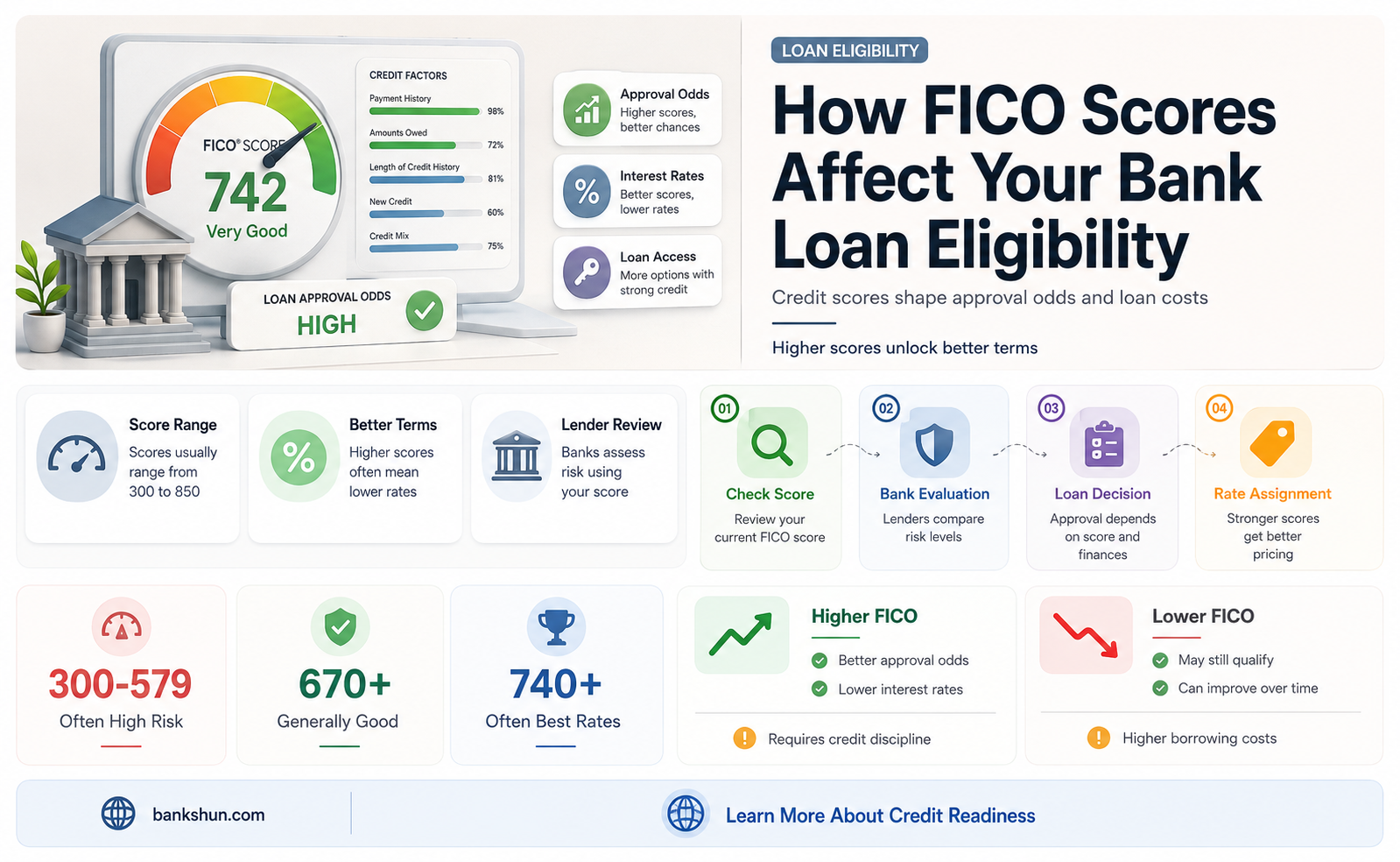

FICO scores are an important factor in determining an individual's eligibility for loans and other forms of credit. The FICO score is the most widely used credit scoring model, with scores ranging from 300 to 850. When applying for a loan, lenders may consider an applicant's FICO scores and credit reports from all three major credit bureaus: Equifax, Experian, and TransUnion. Each of these bureaus uses the FICO Score algorithm to generate a credit score based on an individual's credit history. Lenders may also consider other factors, such as income, assets, and employment history, which are not included in credit reports or factored into credit scores. In the case of mortgage applications, lenders typically request FICO scores from all three bureaus but use only one when making their final decision.

| Characteristics | Values |

|---|---|

| FICO score range | 300-850 |

| Good FICO score | 670 or above |

| Importance of payment history | 35% of FICO score |

| Importance of outstanding debt | 30% of FICO score |

| Importance of credit history length | 15% of FICO score |

| Credit bureaus | Experian, Equifax, TransUnion |

| FICO score versions | FICO Score 8, FICO Score 5, FICO Score 2, FICO Score 4 |

| FICO score used by mortgage lenders | FICO Score 5, FICO Score 2, FICO Score 4 |

| FICO score used by auto lenders | FICO Auto Score |

| FICO score used by credit card issuers | FICO Bankcard Score, FICO Score 8 |

Explore related products

What You'll Learn

![]()

FICO scores for mortgages

FICO scores are an important factor when it comes to mortgages, and understanding how they work is crucial if you're planning to buy a home. Firstly, it's worth noting that FICO scores are a global standard for measuring credit risk in the mortgage industry. Most financial institutions use FICO scores to make lending decisions, so it's important to know your score before applying for a mortgage.

When applying for a mortgage, lenders typically request FICO scores from two or three major credit bureaus: Equifax, TransUnion, and Experian. These bureaus use different versions of the FICO scoring model, including FICO 2, FICO 4, and FICO 5. These models are tailored to evaluate your risk as a mortgage borrower and predict the likelihood of defaulting on a mortgage. They consider factors such as payment history, credit use, credit mix, and the age of your accounts, weighing them differently than a credit card evaluation.

Mortgage lenders usually use the middle score, or the median, of the three bureau scores as the qualifying credit score. This is known as a "tri-merge". If you're applying for a mortgage with a co-signer, each applicant's scores are pulled, and the lower middle score of the two is used. A higher credit score can help you secure a lower interest rate on your mortgage. For example, a borrower with a FICO score of 760 can expect an interest rate of 6.47% on a 30-year fixed mortgage, while a borrower with a score between 620 and 639 may receive a rate of 8.05%.

It's worth noting that FICO scores are constantly being updated to reflect evolving consumer credit behaviours. Mortgage lenders may also use newer FICO models, such as FICO 10 T and VantageScore 4.0, to evaluate your creditworthiness. These newer models can consider rental payments, trends in your credit history, and treat medical collections differently. Therefore, it's important to stay informed about the specific FICO models used by lenders and monitor your credit score regularly.

Flagstar Bank Headquarters: Where is it Located?

You may want to see also

Explore related products

![]()

FICO scores for auto loans

FICO auto scores are industry-specific credit scores that auto lenders use to evaluate loan applications. They are calculated based on factors such as credit history and payment behaviour, with a particular focus on auto loan payments. These scores range from 250 to 900, and a higher score indicates a lower risk of missing a loan payment. While there is no minimum credit score required for auto loans, a FICO score of 670 or higher is generally considered good.

When applying for an auto loan, lenders may use different scoring models, such as FICO Score 8 and 9, or industry-specific FICO Auto Scores. These scores can be accessed by purchasing credit reports or through a paid FICO subscription. Lenders consider various factors in addition to the FICO score, such as income, down payment amount, and debt-to-income ratio. The specific requirements may vary across lenders, and they may use proprietary internal scoring systems.

It is important to note that FICO scores are not the only factor considered by auto lenders. They also take into account an individual's history of auto loan payments and overall payment behaviour. Additionally, they assess other financial factors, such as income and the size of the down payment. By considering these factors, lenders can determine the interest rates offered to borrowers.

To improve your chances of obtaining an auto loan with favourable terms, it is recommended to start working on your credit score well in advance. Maintaining good credit behaviour, such as consistently paying bills on time and lowering debt, is essential. Additionally, getting a creditworthy cosigner, making a sizable down payment, and building a relationship with your bank or credit union can also enhance your approval odds.

While FICO scores are crucial, auto lenders may also consider other factors, including an individual's debt-to-income ratio and previous auto loan history. A good Finance and Insurance (F&I) manager will analyse these factors and work with different banks to secure the best rate for their customers. Therefore, it is beneficial to shop around and explore various lenders to find the most suitable auto loan option.

Your Money, Your Right: Banks Must Refund Unauthorised Transactions

You may want to see also

Explore related products

![]()

FICO scores for credit cards

FICO scores are an important component for lenders and credit decisions. While your credit score does not constitute the only factor in lending decisions, it is a crucial piece of information. FICO scores range from 300 to 850, with anything 670 or above considered good. A good score indicates that you are likely to be able to borrow money at favourable interest rates. A lower score may mean that you will struggle to borrow money, or will have to pay higher interest rates.

Your FICO score is determined by the information on your credit report. Lenders will look at your payment history, credit use, credit mix, and the age of your accounts. Payment history is the single most important factor, accounting for 35% of your score. Other factors include the amount of debt you currently owe as a percentage of all the credit available to you (30%), the length of your credit history (15%), new credit (10%), and your credit mix (10%). Lenders like to see that applicants have experience with multiple types of credit, such as credit cards and car loans.

If you are applying for a credit card, it is a good idea to check your FICO score. Most major card issuers now give cardholders free access to their credit score. For example, Citi cardholders can check their FICO score for free on the Citi Mobile app or on Citi Online. Discover also gives free FICO scores to anyone. Checking your FICO score will give you a good indication of whether you will be approved for a credit card, and it is also a good way to spot identity theft or credit reporting errors.

Armored Trucks and Traffic Laws: Who's Above the Rules?

You may want to see also

Explore related products

![]()

FICO scores from credit bureaus

FICO scores are widely used by lenders to help them make accurate and fast credit risk decisions. FICO scores are calculated based on information in a consumer's credit report maintained by the three major credit bureaus: Experian, Equifax, and TransUnion. Each credit bureau may have different information on file about a consumer, so FICO scores may differ across the three credit bureaus.

When applying for a mortgage, lenders request FICO scores from all three bureaus but typically use only one score when making their final decision. If all three scores are the same, lenders will use that score. If there are differences in the scores, the median score is used, and if two of the three scores are identical, lenders will use that one, regardless of whether it is higher or lower than the third score.

FICO scores are calculated based on various factors, including payment history, credit utilisation ratio, length of credit history, and credit mix. Payment history is the single most important factor, accounting for 35% of the score. A good credit score is generally considered to be 670 or above, while a score of 670-739 is considered "good".

It is important to note that FICO scores are not the only factor lenders consider when making lending decisions. They also consider factors such as income, assets, and employment history, which are not included in credit reports or factored into credit scores.

Sallie Mae CDs: FDIC Insurance and You

You may want to see also

Explore related products

![]()

Improving your FICO score

FICO scores are used by lenders to evaluate applicants for almost any type of loan. Banks and credit card companies usually provide free access to your FICO score. You can also access your free FICO score and credit report online via any of the three main credit reporting agencies: Experian, Equifax, and TransUnion.

- Payment history is the single most important factor, accounting for 35% of your score. Make sure to pay your credit and bills on time. Late payments on credit cards, mortgages, auto loans, or student loans can significantly impact your score.

- The amount of debt you currently owe as a percentage of all the credit available to you is another important factor, accounting for 30% of your score. Lenders want to see that you are able to responsibly handle debt. Reduce the amount of debt you currently owe and keep your outstanding balances below 30% of your total credit limit.

- The length of your credit history makes up 15% of your FICO score. Lenders prefer to see that you have maintained some credit accounts in good standing for a significant period of time. Avoid opening too many new accounts in a short span of time, as this can negatively impact your score.

- Credit mix accounts for 10% of your score. Lenders like to see that applicants have experience using multiple types of credit, such as credit cards, car loans, mortgages, and student loans.

- Review your credit report regularly to ensure that all the information is accurate and dispute any errors that may be affecting your score.

Locating the Oxygen Sensor: Bank 1

You may want to see also

Frequently asked questions

FICO scores are credit scores that range from 300 to 850, with anything 670 or above considered good. Payment history, credit use, credit mix, and the age of accounts are some factors that influence your FICO score.

Yes, banks do look at your FICO score when evaluating loan applications. They may request your FICO scores from all three bureaus (Equifax, Transunion, and Experian) but will only use one when making their final decision.

A FICO score of 670 or above is considered good for obtaining loans with favourable interest rates. However, lenders may also consider other factors such as income, assets, and employment history.

Maintaining a good track record of making on-time payments is crucial for improving your FICO score. Additionally, keeping your credit utilisation ratio low, having a mix of different types of credit, and establishing a long credit history can positively impact your score.

Services like MyFICO provide access to your FICO scores calculated for credit cards, loans, and more. Experian IdentityWork Premium also offers alerts and reports for changes to your FICO score and credit profile.