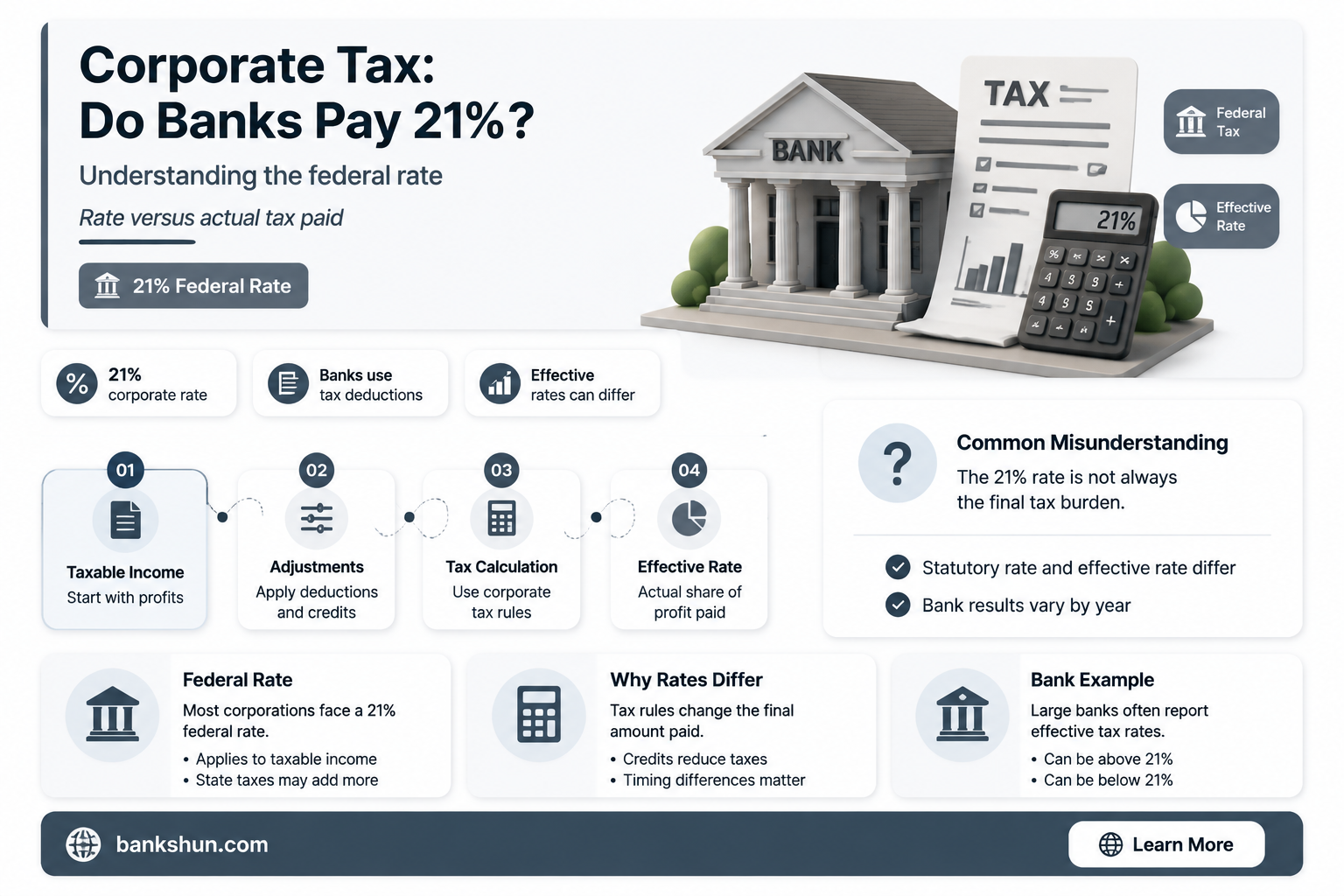

As of 2025, the federal corporate tax rate in the United States is a flat rate of 21%. This rate applies to a corporation's profits, which is calculated as revenue minus expenses. The corporate tax rate was changed from 35% to 21% by the Tax Cuts and Jobs Act (TCJA), enacted on December 22, 2017, and went into effect on January 1, 2018. While this is the federal rate, individual states may impose separate corporate taxes, which can vary widely. For example, North Carolina has a lower corporate tax rate, while New Jersey's rate is in the double digits. In 2021, President Biden proposed raising the corporate tax rate from 21% to 28%.

Explore related products

What You'll Learn

![]()

US corporate tax history

The US federal corporate tax rate is currently 21%, applying to a corporation's profits. This flat rate came into effect in 2018 following the Trump administration's Tax Cuts and Jobs Act (TCJA) of 2017, which significantly revised the US federal income tax regime. The Act moved taxation in the US from a '

Prior to the 2017 Act, the corporate tax rate was 35%. The 2017 changes also meant that corporations could take advantage of various tax credits and deductions to reduce federal, state, or local income tax. These include credits for certain wage payments, investments in certain types of assets, and the use of alternative fuels. Companies can also deduct employee salaries, health benefits, and bonuses from their tax obligations.

In addition to federal taxes, nearly all states and some localities impose a tax on corporate income. These taxes vary widely from state to state, with some not imposing corporate income tax but instead levying a business and occupation tax, which can be a larger burden as it is calculated as a percentage of revenue.

In 2021, President Biden proposed that Congress raise the corporate rate from 21% to 28%.

Transitioning from Banking Analyst to Private Equity Associate

You may want to see also

Explore related products

![The Complete LLC & S-Corp Beginner's Guide: [2 books in 1] The Easy Way to Create & Manage Your Limited Liability Company or S Corporation so You Can Focus on What Matters Most (Start a Business)](https://m.media-amazon.com/images/I/71h5MqU4cvL._AC_UY218_.jpg)

![]()

State corporate tax

In the United States, the federal corporate tax rate is currently a flat rate of 21%. This rate applies to a corporation's profits and taxable income, which includes revenue minus expenses. While this is the federal rate, state corporate tax rates vary across the country.

State and local governments collected a combined $99 billion in revenue from corporate income taxes in 2021. Most US businesses, including sole proprietorships, partnerships, and certain eligible corporations, do not pay federal or state corporate income taxes. Instead, their owners include an allocated share of the businesses' profits ("pass-through" income) in their taxable income under individual income tax.

In 2023, top state corporate income tax rates ranged from 2.5% in North Carolina to 9.8% in Minnesota. States like Arizona, Colorado, Indiana, Kansas, Missouri, North Carolina, North Dakota, Oklahoma, and Utah had top corporate tax rates lower than 5%. On the other hand, Alaska, Illinois, Minnesota, and New Jersey had top tax rates of 9% or higher.

Converting Apple Cash: Transfer to Your Bank Easily

You may want to see also

Explore related products

![]()

Corporate tax deductions

In the United States, corporate tax deductions are allowed for various expenses and investments. The corporate income tax rate in the US is currently 21%, applicable to the profits of US resident corporations. This flat rate was introduced by the Tax Cuts and Jobs Act (TCJA) in 2017, which replaced the previous rate of 35%.

There are several deductions and incentives available to corporations, including banks and financial institutions, to reduce their tax liability. One such deduction is the Net Operating Loss (NOL) deduction, which allows corporations to carry forward or carry back losses to offset taxable income in other years. Additionally, the TCJA introduced the Base Erosion and Anti-abuse Tax (BEAT), which targets base-eroding payments made to related foreign persons. Certain banks and securities dealers are subject to a lower BEAT rate of 2% instead of the standard 3%.

The One Big Beautiful Bill Act of 2025 (OBBBA) introduced several changes relevant to corporate tax deductions. It extended the IRC § 199A qualified business income deduction, allowing non-corporate taxpayers (including shareholders of S-corporations) to deduct 20% of their qualified business income. The OBBBA also increased the flat cap for excluding capital gains on the disposition of QSBS (Qualified Small Business Stock) from $10 million to $15 million, benefiting smaller investors. Additionally, the OBBBA introduced tax-advantaged savings vehicles and incentives for inbound investment, such as the short-term debt exception and the bank deposit exception.

Furthermore, corporations can deduct certain expenses related to research and development under Section 174. The ODD (Overall Domestic Cap) credit must be reduced by the amount of the ODC expenditure deduction unless an election is made on Form 8820. The OBBBA also added adjustments for certain intangible drilling and development costs. Corporations can also benefit from minimum tax credits, such as the Corporate AMT Foreign Tax Credit (FTC), which can be carried forward and claimed against regular tax in future years.

It is important to note that corporate tax deductions vary across different states in the US, and certain states may impose taxes similar to corporate income tax, such as the business and occupation tax (B&O tax) in Washington state. Overall, corporate tax deductions aim to encourage investment, support specific industries, and provide tax relief to corporations in the United States.

Banks' Response to Auto Dealer Forgery: What You Need to Know

You may want to see also

Explore related products

![]()

Corporate tax on foreign earnings

In the United States, the corporate tax rate is 21% for US resident corporations. This flat rate was introduced by the Tax Cuts and Jobs Act (TCJA) in 2017, which replaced the previous rate of 35%. The TCJA also eliminated the graduated corporate rate schedule and the corporate alternative minimum tax.

The US taxes the foreign income of domestic corporations using a hybrid system that combines territorial and worldwide systems. Certain categories of foreign income, such as passive or highly mobile income (Subpart F income), are taxed at the full statutory corporate rate. However, the global intangible low-taxed income (GILTI) minimum tax is taxed at a reduced rate. GILTI refers to foreign income exceeding 10% of foreign tangible assets. US-based corporations owned by foreign multinational companies are generally subject to the same tax rules as US-owned corporations regarding their profits from US business activities.

The US tax code also addresses the taxation of foreign corporations connected with US business operations. Foreign corporations engaged in trade or business within the US are taxed on their taxable income, which is effectively connected to their business activities within the country. This includes gross income derived from sources within the US and may include special tax treatments for certain situations, such as the disposition of US real property interests.

The US Department of the Treasury has proposed a 21% minimum tax on the foreign earnings of US corporations, which is currently set at 10.5%. This proposal, known as the Made in America Tax Plan, aims to reduce the incentive for corporations to shift profits and jobs abroad. It is intended to create a more level playing field for domestic businesses and workers, ensuring that corporations pay their fair share of taxes.

Documents Needed for CTR: What Banks Require?

You may want to see also

Explore related products

![]()

Corporate tax on banks and securities dealers

In the United States, the corporate tax rate is a flat rate of 21% as of January 2025. This rate came into effect starting on January 1, 2018, following the passage of the Tax Cuts and Jobs Act on December 20, 2017. The Act significantly revised the federal income tax regime, moving it from a '\co: 3,14,17>worldwide' system of corporate taxation to a 'territorial' system.

Prior to the enactment of the Tax Cuts and Jobs Act, the corporate tax rate in the US was 35%. The new flat rate of 21% applies to a corporation's profits and is based on net taxable income as defined by federal or state law. It is worth noting that certain banks and securities dealers are taxed at different rates, with some sources indicating rates of 11% and 6%, or 10.5% for taxable income after 31 December 2025.

In addition to federal corporate taxes, some states in the US impose separate corporate taxes on companies. These state-level corporate income taxes can vary from a few percentage points to double digits. For example, North Carolina has a lower corporate tax rate, while New Jersey falls into the double-digit range.

In New York City, there is a specific Banking Corporation Tax (BCT) that applies to certain banking corporations. This tax rate is the largest of the following four options:

- 9% of the entire net income allocated to the city

- 0.1 of a mill for every dollar of taxable assets allocated to New York City (with certain adjustments for corporations with high mortgage ratios or those holding certain net worth certificates)

- 3% of alternative entire net income allocated to the city

- A percentage of the issued capital stock

The specific rate applied depends on the corporation's circumstances and allocations, with the NYC Department of Finance keeping records of the issuer's allocation percentages for all general and banking corporations.

Zelle Accessibility: Which Banks Can Use Zelle?

You may want to see also

Frequently asked questions

Yes, banks are subject to a 21% corporate tax rate in the US. This rate applies to a bank's profits, which is calculated as revenue minus expenses.

As of January 2025, the corporate tax rate in the US is a flat rate of 21%.

No, before the Tax Cuts and Jobs Act (TCJA) was passed in 2017, the corporate tax rate was 35%. The new rate of 21% came into effect on January 1, 2018.

Yes, in 2021, President Biden proposed raising the corporate tax rate from 21% to 28%.