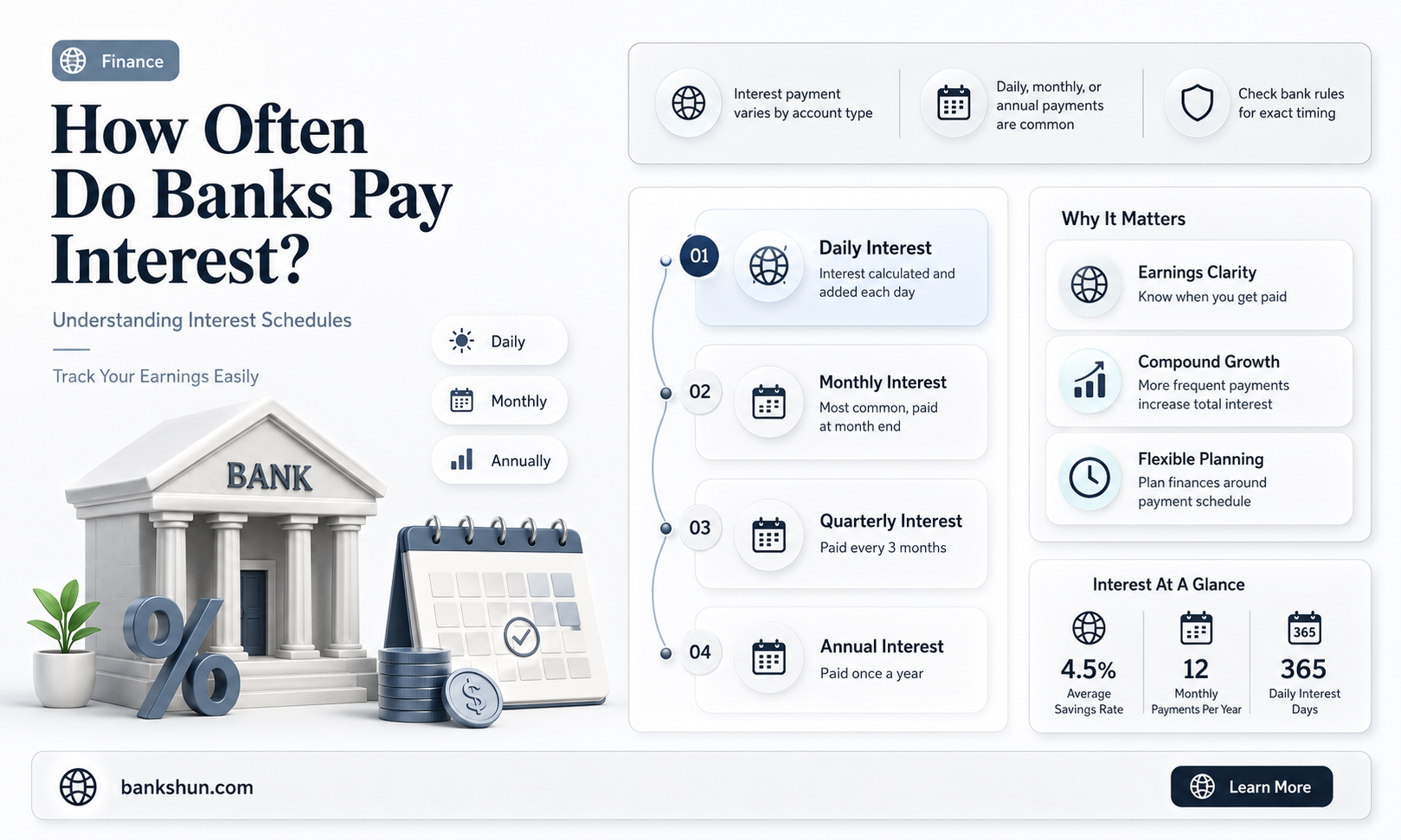

Banks pay interest on savings accounts either monthly or yearly, depending on the type of account and the bank's policies. Some banks offer high-yield savings accounts that provide competitive interest rates, which can be significantly higher than the national average. These accounts often have features like no monthly fees, no minimum balance requirements, and easy access to funds. On the other hand, some savings accounts may have lower interest rates but offer the flexibility of withdrawing funds without penalties. Understanding the different options available and choosing the right type of savings account is essential to align with one's financial goals and preferences.

| Characteristics | Values |

|---|---|

| Frequency of interest payments | Monthly or yearly, depending on the type of account and the bank |

| Types of accounts | Savings accounts, money market accounts, CDs, and other types of deposit accounts |

| Interest calculation | Simple or compound interest |

| Annual percentage yield (APY) | Varies by bank and account type, with high-yield savings accounts typically offering higher APYs |

| Fees | Some banks charge monthly service fees, while others offer no-fee accounts |

| Minimum balance requirements | Varies by bank and account type, with some accounts offering $0 minimum balance requirements |

| Withdrawal options | May include ATM, peer-to-peer money transfer, or ACH transfer; some accounts may limit withdrawals to a maximum of six per month |

| Location | Online-only banks or traditional brick-and-mortar banks |

Explore related products

What You'll Learn

![]()

Banks lend your money to borrowers and pay interest

Banks get the money they lend out primarily from customer deposits. They also have other funding sources, such as interbank borrowing, central bank loans, bond issuance, securitization, wholesale and brokered deposits, foreign deposits, and equity capital. Banks expand the money supply through lending and redepositing cycles, playing a critical role in economic activity and growth.

The interest rate is an important factor in banking, as it determines the revenue generated by loans and deposits. In the short term, central banks set interest rates to regulate the economy and control inflation. In the long term, interest rates are set by supply and demand pressures. When interest rates are low, there is more incentive for companies and individuals to borrow, increasing loan demand. On the other hand, when rates are high, loans become more expensive, and loan demand tends to fall.

Banks also generate revenue through non-interest fees for their services, such as monthly account fees, wealth management services, and investment products. These fee-based income sources are stable and attractive for banks, especially during economic downturns when interest rates may be low. Overall, banks play a crucial role in the economy by lending money to borrowers and creating new money in the form of loans.

Financing Fifth Wheels and Trucks: What Banks Offer?

You may want to see also

Explore related products

![]()

Simple interest is calculated using the original sum

Banks pay interest either monthly or yearly, depending on the type of account. When it comes to savings accounts, banks typically use compound interest, which takes into account both the original sum and any interest accrued over time. However, some banks may use simple interest for certain accounts.

Simple interest is a calculation of interest that does not involve compounding. It is based solely on the original principal amount of a loan or deposit, also known as the principal balance or the original sum. This means that you will always pay less interest on a simple interest loan than a compound interest loan if the loan term is more than a year.

The formula for calculating simple interest is:

> Simple Interest = Principal Amount × Interest Rate × Time

Using this formula, you can calculate interest over different periods, such as daily or monthly. For example, if you want to calculate the monthly interest rate, you can input the monthly interest rate as "r" and multiply it by the "n" number of periods.

Let's say you take out a $10,000 loan with a 5% annual simple interest rate to be repaid over five years. To calculate the total interest, you would multiply the principal amount ($10,000) by the interest rate (0.05) by the number of years (5):

> Simple Interest = $10,000 × 0.05 × 5 = $2,500

So, the total interest paid over the five-year period would be $2,500. This can be added to the principal amount to get the total amount repaid:

> Total Repayment = $10,000 + $2,500 = $12,500

Simple interest is often used for short-term loans or single-period loans, while compound interest is more common for longer-term loans, investments, and financial products. Simple interest provides borrowers with a straightforward idea of the cost of borrowing, making it a useful calculation method for certain scenarios.

US Bank's Union Bank Buyout: What's the Deal?

You may want to see also

Explore related products

![]()

High-yield savings accounts earn more interest

Banks pay interest on savings accounts annually, but the frequency of compounding varies. It could be daily, monthly, quarterly, or yearly. The annual percentage yield (APY) is the amount of compound interest an account earns in a year. It is based on the account's interest rate and the number of times interest is paid during the year.

High-yield savings accounts offer a much greater APY than traditional savings accounts. Traditional accounts often earn around 0.01% APY, while high-yield savings accounts can earn upwards of 4% APY. This higher APY means your bank balance can grow faster over time without any additional effort on your part. For example, with a 4% APY, a savings balance of $10,000 would earn over $400 after a year, compared to just $40 with a 0.40% APY.

Some high-yield savings accounts with competitive rates include:

- TAB Bank's TAB Save account

- Bask Bank's Interest Savings account

- Capital One's high-yield savings account

- Synchrony's High-Yield Savings account

- Openbank Savings account

- CIT's Platinum Savings account

When choosing a high-yield savings account, it is important to consider the APY, fees, minimum deposit and balance requirements, and the convenience of withdrawing money. These accounts are safe if they are offered by an FDIC-insured bank or a National Credit Union Administration (NCUA) credit union and within federal insurance limits and guidelines.

The Best Bank Names: What Makes Them Unique?

You may want to see also

Explore related products

![]()

Annual percentage yield (APY) varies by bank

The annual percentage yield (APY) is the effective rate of return on an investment for one year, taking compounding interest into account. In other words, it is the interest rate earned on an investment in one year, including compounding interest. APY is the annualized rate that shows how much money can be earned in interest on an account over a year. Banks in the US are required to include the APY when they advertise their interest-bearing accounts, making it easy to compare high-yield savings accounts.

APY is calculated using the interest rate and the compounding frequency. It is the sum of the interest earned on the original sum invested and the interest earned on the accumulated interest over time. The more funds in the account, the more money will be made. APY is usually higher for savings accounts than for checking accounts because consumers tend to leave the money in savings accounts for longer, allowing the bank to use it to make loans and earn interest.

The APY varies by bank and by the type of account. For example, the Openbank Savings account is an online high-yield savings option that offers competitive interest rates that vary based on the account balance. Amounts below $250,000 earn 3.90% APY, while rates at or above $250,000 earn 4.10% APY. In contrast, CIT's Platinum Savings account pays 4.00% APY on balances of $5,000 or more.

Some banks offer high-yield savings accounts with no minimum deposit requirements or monthly fees. For example, the Capital One high-yield savings account has no minimum deposit requirements and no monthly fees. It earns a 3.65% APY, which is higher than the national average for a savings account, which is 0.41% according to the FDIC.

Gold Coin Investment: Banks and Buying Guide

You may want to see also

Explore related products

![]()

Notice saver accounts require advance notice for withdrawal

Banks pay interest on savings accounts because they lend your money to borrowers in the form of loans, mortgages, or credit cards. The interest you receive is calculated using either simple or compound interest, depending on your account. Simple interest is calculated using only your principal balance, while compound interest is calculated using both your principal balance and any interest that has accumulated over time. Compound interest is added to your account at the end of every compounding period, which is typically every day or every month. The annual percentage yield (APY) is the amount of compound interest an account earns in a year, and it is based on the account's interest rate and the number of times interest is paid during the year.

Now, let's discuss notice saver accounts, which are a type of savings account that requires you to notify your bank or financial institution in advance of making a withdrawal. This advance notice period is a key feature of these accounts and can vary significantly from one bank to another, typically ranging from 30 to 180 days. Some accounts may also impose restrictions on the number of withdrawals you can make annually or per month, so it is important to carefully read the terms and conditions before opening an account. The notice period is intended to help prevent spontaneous withdrawals, which can be beneficial for long-term budgeting and saving.

While the required notice period may seem inconvenient, notice saver accounts offer some advantages. Firstly, they often provide higher interest rates compared to easy access savings accounts. Secondly, notice saver accounts usually allow ongoing deposits, so you can continue adding to your savings over time. Additionally, some accounts offer high introductory interest rates, although these may expire after a set period, such as 12 months. It is worth noting that if you need to access your funds before the notice period ends, you may face penalties such as forfeited interest or even account closure. Therefore, it is crucial to choose an account with a notice period that suits your financial needs and to be comfortable with the potential consequences of early withdrawal.

It is important to understand the full terms and conditions of a notice saver account before opening one. In addition to the notice period and withdrawal restrictions, pay attention to any minimum balance requirements, introductory rates, and associated fees and charges. Also, be aware that some accounts may offer higher interest rates for larger balances, so consider your savings goals when selecting an account. While notice saver accounts can be a great option for those who plan their finances in advance, they may not be suitable for everyone, especially if you require more immediate access to your funds.

In summary, notice saver accounts require advance notice for withdrawals, with notice periods typically ranging from 30 to 180 days. These accounts can help with long-term budgeting and saving by discouraging impulse spending. They often provide higher interest rates and allow ongoing deposits. However, early withdrawals may result in penalties, and certain restrictions may apply. Therefore, it is essential to carefully review the terms and conditions of a notice saver account before opening one to ensure it aligns with your financial goals and needs.

Leased Car Bank Fees: What's Standard?

You may want to see also

Frequently asked questions

Banks pay interest either monthly or yearly, depending on the type of account. Some banks pay interest at a simple rate, while others use compound interest, which is calculated at the end of every compounding period, typically every day or month.

Simple interest is calculated using only the principal balance, or the original sum deposited into the account. Compound interest is calculated on both the original sum and any interest accumulated over time.

Here are some banks that offer competitive interest rates as of September 2025:

- Bask Bank

- Jenius Bank

- Popular Direct

- Upgrade

- UFB Direct

- Live Oak Bank

- Openbank

- Capital One

- Synchrony

- Squirrel (New Zealand)