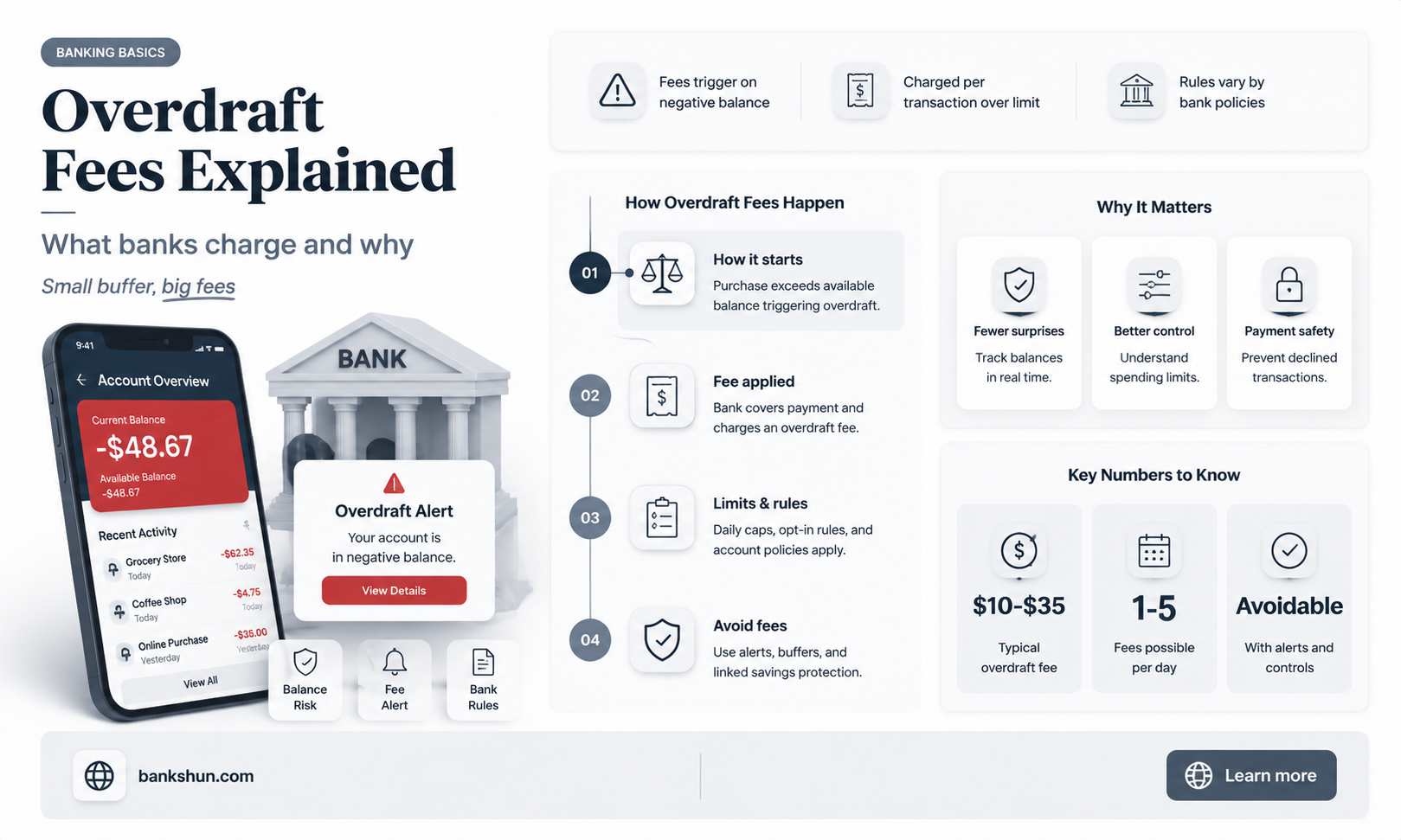

Overdraft fees are charges incurred by bank customers when they don't have enough money in their account to cover transactions. While some banks do not charge overdraft fees, others charge fees ranging from $30 to $35 per transaction. These fees can be costly, especially if multiple transactions are made in a day, and some banks also charge continuous overdraft fees. Overdraft protection is an option offered by banks to prevent overdrafts, but it often comes with a significant fee and interest. Customers can opt in or out of overdraft coverage, and some banks provide overdraft protection transfers and buffer programs to help customers avoid fees.

| Characteristics | Values |

|---|---|

| Overdraft fee amount | Typically $30-$35 per transaction, but some banks charge $10 per day or less, and some charge nothing |

| Overdraft protection fee | Charged by some banks for transferring funds from a savings account to cover an overdraft |

| Opt-in | Required for overdraft coverage for debit card and ATM transactions |

| Non-sufficient funds (NSF) fee | Charged for writing a check for more than the account balance |

| Monthly fee | Charged by some banks for maintaining deposit accounts |

| Continuous overdraft fees | Charged by some banks for each day the account is overdrawn |

Explore related products

What You'll Learn

- Overdraft fees vary by bank, typically ranging from $15 to $37 per transaction

- Overdraft protection is optional and can be costly, but it prevents embarrassment and returned checks

- Customers can opt-in or opt-out of overdraft coverage for debit card transactions

- Banks can charge a monthly fee for maintaining deposit accounts, but this can be waived in certain situations

- Overdraft laws determine whether a bank can charge fees for overdrawing transactions

![]()

Overdraft fees vary by bank, typically ranging from $15 to $37 per transaction

Overdraft fees are typically among the most expensive fees charged by banks, and they can add up quickly. While some banks charge low or no overdraft fees, others can charge up to $35 per transaction. The cost varies depending on the bank and the type of account. For example, some banks offer a small buffer, such as $5, that customers can overdraft without incurring a fee.

By law, banks cannot charge overdraft fees for certain types of transactions, such as one-time debit card transactions and ATM withdrawals, unless the customer has opted into overdraft coverage. However, banks can charge overdraft fees for checks and recurring electronic payments, even if the customer has not opted into overdraft coverage. Additionally, some banks may charge continuous or daily overdraft fees.

Overdraft protection is a service that links a checking account to a savings account, another checking account, or a line of credit to prevent an overdraft. While this service can be helpful in avoiding overdraft fees, it often comes with a significant fee and interest. Customers should be mindful of these costs and use overdraft protection sparingly and only in emergencies.

It is important to note that customers have the right to opt-in or opt-out of overdraft coverage and protection. Keeping track of account balances and staying current with transactions can help individuals avoid overdraft fees.

Exploring Red Bank, NJ: Fun Things to Do

You may want to see also

Explore related products

![]()

Overdraft protection is optional and can be costly, but it prevents embarrassment and returned checks

Overdraft protection is an optional service offered by banks to help customers avoid the consequences of insufficient funds in their accounts. It acts as a temporary loan, allowing customers to continue making transactions even when their account balance is zero. This service is particularly useful for preventing the embarrassment of a declined transaction or a bounced check.

While overdraft protection can provide a short-term solution during emergencies, it often comes with significant fees and interest charges. The cost of overdraft fees varies by bank, typically ranging from \$30 to \$35 per transaction. Some banks may also charge daily overdraft fees, resulting in multiple fees accumulating in a single day. These fees can add up quickly and create a financial burden for the account holder.

To enrol in overdraft protection, customers usually need to request it and link their checking account to a savings account, another checking account, or a line of credit. This linked account serves as a backup source of funds, ensuring that transactions are covered even when the primary account has insufficient funds. However, it's important to note that overusing overdraft protection can lead to its removal by the financial institution.

Although overdraft protection is optional, customers should carefully consider the costs involved. By opting in, customers give their bank permission to process transactions with insufficient funds and transfer funds from the linked account. While this can prevent declined transactions and returned checks, the associated fees and interest can be costly. Therefore, it is advisable to use overdraft protection sparingly and only in emergencies.

To avoid overdraft fees, customers can maintain a careful record of their transactions and account balance. Additionally, some banks offer accounts with no overdraft fees or provide options like free overdraft protection transfers and buffer programs to help customers manage their finances effectively.

Direct Express: Which Bank is Behind the Card?

You may want to see also

Explore related products

![]()

Customers can opt-in or opt-out of overdraft coverage for debit card transactions

Banks typically charge a fee for overdrafts, which occur when you don't have enough money in your account to cover a transaction. Overdraft fees can be expensive, often ranging from $30 to $35 per transaction, and can add up quickly. Some banks may also charge continuous or daily overdraft fees.

Overdraft coverage is optional, and customers can choose to opt-in or opt-out of this service for debit card transactions. If you opt-in, your bank will pay for the transaction, but you will be charged an overdraft fee. This fee is typically incurred for each transaction that results in a negative account balance, and multiple fees may be charged in a single day.

If you do not opt-in for overdraft coverage, your bank will decline or refuse the transaction if it will overdraw your account, and you will not be charged a fee. However, you may be charged a fee by the payee, such as a late fee.

It is important to note that banks are required by law to disclose any fees they charge for deposit accounts, including overdraft fees. Additionally, customers who have opted into overdraft protection can change their minds at any time and opt-out by contacting their bank.

Bank Mobile: Signing Up for an Account

You may want to see also

Explore related products

![]()

Banks can charge a monthly fee for maintaining deposit accounts, but this can be waived in certain situations

Banks typically charge a monthly fee for maintaining deposit accounts. These fees may range from $5 to $25 per month, with accounts offering more features, such as rewards accounts, charging higher fees. However, these fees can often be waived or reduced under certain circumstances.

Firstly, some banks may waive the monthly maintenance fee if you maintain a minimum balance in your account. This not only helps you avoid the monthly fee but also prevents overdraft fees, as you ensure that your account balance can cover your transactions. Banks may also offer low-balance alerts to help you stay above the minimum balance requirement.

Secondly, direct deposits can also help you avoid monthly maintenance fees. Setting up direct deposits, such as your paycheck, can eliminate some of these charges. Additionally, direct deposits can help prevent overdraft fees by ensuring that funds are consistently and automatically deposited into your account.

Thirdly, opting for paperless statements can be another way to reduce monthly fees. Banks may waive certain fees if you choose to receive your statements electronically instead of through paper mail. This not only helps reduce costs for the bank but also promotes environmentally friendly practices.

Furthermore, utilising multiple products or services from the same bank can lead to fee waivers. Banks may offer incentives for customers who maintain multiple accounts or services with them. By consolidating your banking needs, you may be able to negotiate or qualify for waivers on specific monthly maintenance fees.

It is important to note that the specific requirements for fee waivers may vary between different banks. Therefore, it is always a good idea to research and compare the offerings of various banks before choosing an account that best suits your needs. Understanding the fee structure and requirements for waivers can help you make informed decisions and effectively manage your finances.

Banks' Confidentiality: Commercial Lending and Customer Privacy

You may want to see also

![]()

Overdraft laws determine whether a bank can charge fees for overdrawing transactions

Overdraft fees are incurred when an individual does not have enough money in their account to cover their transactions. The cost of overdraft fees varies by bank, typically ranging from $30 to $35 per transaction. These fees can add up quickly, and some banks also charge daily overdraft fees.

Customers have the choice to opt in or opt out of overdraft coverage for debit card transactions. However, they may not have a choice when using paper checks or other payment methods. If a customer does not opt in to overdraft protection, their bank will reject transactions that exceed their account balance.

Some banks offer overdraft protection plans, which link a checking account to a backup savings account, credit card, or line of credit. This allows customers to access funds from the linked account in the event of an overdraft. While overdraft protection can be a useful tool to prevent shortfalls, it often comes with significant fees and interest charges.

It is important to note that banks are required to disclose any fees associated with deposit accounts, including overdraft fees. Customers should carefully review the account opening disclosure and fee schedule provided by the bank to understand the potential charges.

Protecting Your Money: Bank Insurance Against Wire Fraud

You may want to see also

Frequently asked questions

Yes, banks usually charge a fee for an overdraft, which can be costly. The fee varies by bank but typically ranges from $30 to $35 per transaction. Some banks also charge daily overdraft fees.

An overdraft fee is a charge incurred when you don't have enough money in your account to cover a transaction. Overdraft protection allows banks to process transactions when customers have insufficient funds.

Yes, you can avoid overdraft fees by opting out of overdraft coverage. If you do not opt in, your bank will decline transactions that exceed your available balance, and you will not be charged a fee.

Some banks offer overdraft protection, which links your checking account to a savings account, another checking account, or a line of credit. This allows you to access funds from the linked account to cover transactions that would otherwise result in an overdraft.