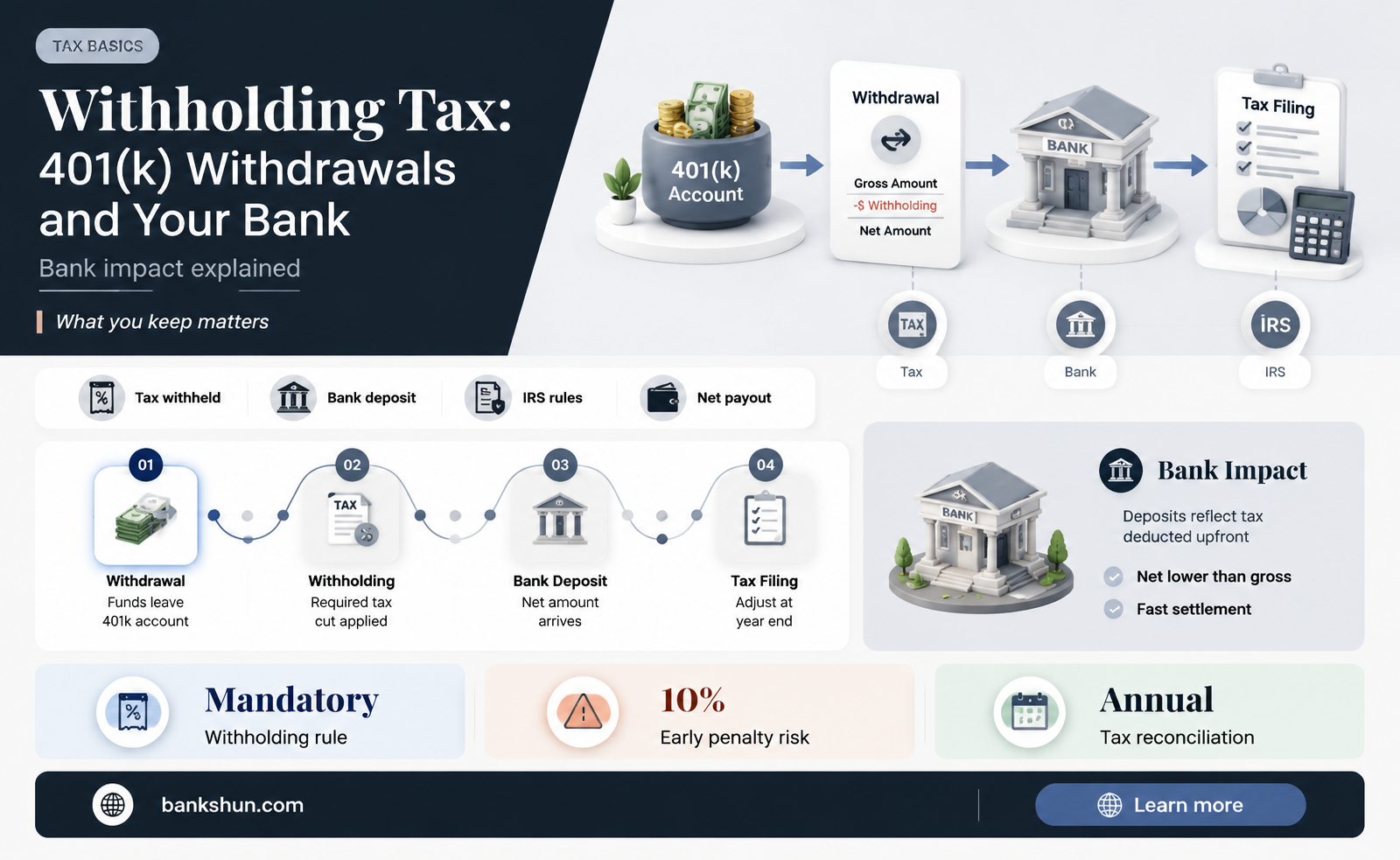

When it comes to 401(k) withdrawals, there are a few things to keep in mind regarding taxes. Firstly, 401(k) withdrawals are typically considered taxable income, and you will generally need to pay taxes on the money you withdraw. The tax rate will depend on your federal tax bracket at the time of withdrawal, and there may be additional taxes or penalties for early withdrawals before the age of 59½. Some 401(k) plans automatically withhold a portion of the withdrawal, usually 20%, to cover taxes, but this may not be enough to cover your full tax liability. It's important to understand the tax implications to make informed decisions and avoid unnecessary taxes. Consulting a financial advisor or tax expert can help navigate the complexities and design a tax-efficient withdrawal strategy.

Explore related products

What You'll Learn

![]()

Taxes on 401(k) withdrawals are considered taxable income

There are some exceptions to this rule. For example, if you have a Roth 401(k), you won't pay taxes on your withdrawals in retirement because the money you put in was already taxed. However, you can still be assessed taxes and penalties for taking out your money before the age of 59 1/2. If you are under the age of 59 1/2 when you withdraw funds from your 401(k), you may have to pay a 10% additional tax on the distribution, though there are exemptions to this rule.

If you are retired, you have to start taking a required minimum distribution from your Traditional 401(k) account at a certain age. The age at which these withdrawals become mandatory varies by source but is generally given as 72 or 73. If you don't take the required minimum distribution, the Internal Revenue Service can assess a penalty of 25% of the amount not distributed. This penalty may be reduced to 10% if you take a corrective distribution and meet other requirements.

Some 401(k) plans will automatically withhold 20% of your distribution to pay for taxes, though this is not always enough to cover your full tax liability. In that case, you'll have to pay the rest of the tax when you file your return. If you've paid more than you owe, you'll get a refund at tax time.

ACH Banking: How Does It Work?

You may want to see also

Explore related products

![]()

20% tax withholding on 401(k) withdrawals

When it comes to 401(k) withdrawals, it's important to understand the tax implications to make informed decisions. Here are some key points about the 20% tax withholding on 401(k) withdrawals:

Understanding 20% Tax Withholding

With a traditional 401(k), contributions are typically made with pre-tax dollars, which lowers your taxable income for that year. However, when you eventually withdraw funds from your 401(k), you will need to pay income taxes on those distributions. Some 401(k) plans will automatically withhold 20% of the distribution to cover a portion of the taxes you owe. This 20% withholding is like a prepayment of your taxes, and it helps simplify your tax filing process.

Early Withdrawals and Penalties

It's important to note that retirement plans are generally designed for you to use the money during retirement. If you make withdrawals from your 401(k) before the age of 59 and a half, you may incur an additional 10% tax penalty on the distribution. This early withdrawal penalty can be avoided if you meet certain exceptions, such as an emergency withdrawal of up to $1,000, if permitted by your plan.

Rollovers and Tax Implications

If you are moving your 401(k) funds to a new retirement plan, such as an Individual Retirement Account (IRA) or a different 401(k), through a direct rollover, no tax withholding is necessary since the rollover is not taxable. However, in an indirect rollover, where the funds are sent to you first, tax withholding may come into play. Any taxable distribution you receive is subject to mandatory withholding of 20%, even if you plan to roll over the distribution later.

Adjusting Withholding Amounts

In some cases, the 20% withholding may not accurately reflect your actual tax liability. If the 20% withheld is more than what you owe, you will receive a refund when you file your tax return. On the other hand, if the withheld amount is not enough to cover your tax liability, you will need to pay the remaining amount when filing your taxes. It's worth noting that you can also choose to withhold more or less than 20%, depending on your expected tax bracket in retirement.

Tax Strategies for Retirement

To optimize your tax strategy in retirement, consider consulting a financial advisor or tax professional. They can help you navigate the complexities of retirement tax credits and deductions and strategies to manage your taxable income. By planning ahead, you may be able to minimize your tax burden and maximize your retirement savings.

Catching Crappie from the Bank: Techniques and Strategies

You may want to see also

Explore related products

![]()

10% additional tax on early withdrawals (before 59 1/2 years)

Retirement plans are designed so that you can use the money when you reach retirement age. For this reason, rules restrict you from taking distributions before the age of 59 and a half. While you can take money out before you reach that age, you will generally have to pay a 10% additional tax penalty, unless you meet one of the exceptions.

If you are taking out funds from your retirement account before you turn 59 and a half, you must use IRS Form 5329 to report the amount of 10% additional tax you owe on an early distribution or to claim an exception to the 10% additional tax. You can find additional exceptions to the early withdrawal penalty in the Form 5329 instructions. When you take a distribution from your 401(k), your retirement plan will send you a Form 1099-R. This tax form shows how much you withdrew overall and the federal and state taxes withheld from the distribution if applicable. This form is sent when you've made a distribution of $10 or more.

Some of the exceptions to the 10% additional tax on early distributions include:

- Distributions made to a beneficiary (or to the estate of the participant) on or after the death of the participant.

- Distributions made because the participant has a qualifying disability.

- Distributions made as part of a series of substantially equal periodic payments beginning after separation from service and made at least annually for the life or life expectancy of the participant or the joint lives or life expectancies of the participant and their designated beneficiary.

- Distributions made to a participant after separation from service if the separation occurred during or after the calendar year in which the participant reached the age of 55.

- Distributions made to an alternate payee under a qualified domestic relations order (QDRO).

- Distributions made to a participant for medical care up to the amount allowable as a medical expense deduction.

- Distributions made because of an IRS levy on the plan.

- Distributions made on account of certain disasters for which IRS relief has been granted.

How Often Do Banks Pay Interest?

You may want to see also

Explore related products

![]()

Loans on 401(k) balance

A 401(k) loan is when you borrow money from your retirement savings account. The amount you can borrow depends on your employer's plan, but it's typically up to 50% of your vested account balance or $50,000, whichever is less. Some plans allow you to borrow up to $10,000 if 50% of your vested account balance is less than that amount.

You must repay the loan within five years, unless the loan is used to purchase your primary residence. Loan repayments must be made in substantially equal payments, at least quarterly, over the life of the loan. You can usually repay the loan faster without a prepayment penalty. Most plans allow for loan repayment through payroll deductions, using after-tax dollars.

Unlike 401(k) withdrawals, you don't have to pay taxes and penalties when taking a 401(k) loan. The interest you pay on the loan goes back into your retirement plan account. However, there are still opportunity costs associated with this type of loan. During the loan period, you will miss out on the potential growth of those funds. Additionally, some plans prohibit contributions to your account until you repay the loan balance, and you may miss out on any employer-matched contributions.

If you leave your job with an unpaid loan, you will have to repay the loan in full. If you don't, the full unpaid loan balance will be considered a taxable distribution, and you may face a 10% federal tax penalty on the unpaid balance if you are under 59 and a half years old.

Before taking a loan from your 401(k), consider speaking to an investment advice fiduciary, who is required to act in your best interests.

Federal Reserve Banks: Where Are They Located?

You may want to see also

Explore related products

![]()

Rollovers from 401(k) plans

When it comes to rollovers from 401(k) plans, there are a few different options to consider. Firstly, it's important to understand the difference between a direct and indirect rollover. A direct rollover occurs when the funds are transferred directly from one retirement plan to another without you receiving the money first. In this case, no tax withholding is necessary since the rollover isn't taxable.

On the other hand, an indirect rollover happens when the money is sent to you first before being rolled over to another plan. In this scenario, taxes may be withheld from the distribution, and you will need to use other funds to make up for the amount withheld if you decide to roll over the full amount. You typically have 60 days from the date of receiving the distribution to complete the rollover.

Another option is to roll over your 401(k) into a rollover IRA, which is a retirement account that allows you to move money from your former employer-sponsored plan to an IRA. This option is tax and penalty-free, and your money can continue to grow tax-deferred. However, if you roll pre-tax 401(k) funds into a traditional IRA, you may not be able to roll those funds back into an employer-sponsored retirement plan. Additionally, if you convert pre-tax 401(k) funds into a Roth IRA, it will be considered a taxable event.

If you are self-employed, you may also have the option to roll over your 401(k) into your own small business retirement plan, such as a SEP IRA or a self-employed 401(k). It's important to note that not all employers will accept a rollover from a previous employer's plan, so it's recommended to check with your new employer before making any decisions.

Lastly, if you have appreciated company stock in your 401(k) plan, you may want to consider the potential impact of net unrealized appreciation (NUA) before deciding to roll over the stock to another plan. Rolling over the stock into another tax-advantaged plan will eliminate any NUA.

Explore Mortgage Options: 10% Down Payment Possibilities

You may want to see also

Frequently asked questions

Yes, banks withhold a mandatory tax of 20% on 401k withdrawals. However, this may not be enough to cover your full tax liability, in which case you will have to pay the remaining amount when filing your tax return.

Withdrawing from a 401k before the age of 59 1/2 is considered an early distribution and may result in a 10% additional tax penalty. You will need to report this additional tax using IRS Form 5329.

Yes, one way to reduce taxes on 401k withdrawals is to delay withdrawals until after you have retired. This can potentially lower your taxable income in retirement. Additionally, you may qualify for certain tax credits or deductions in retirement that can further reduce your taxable income.