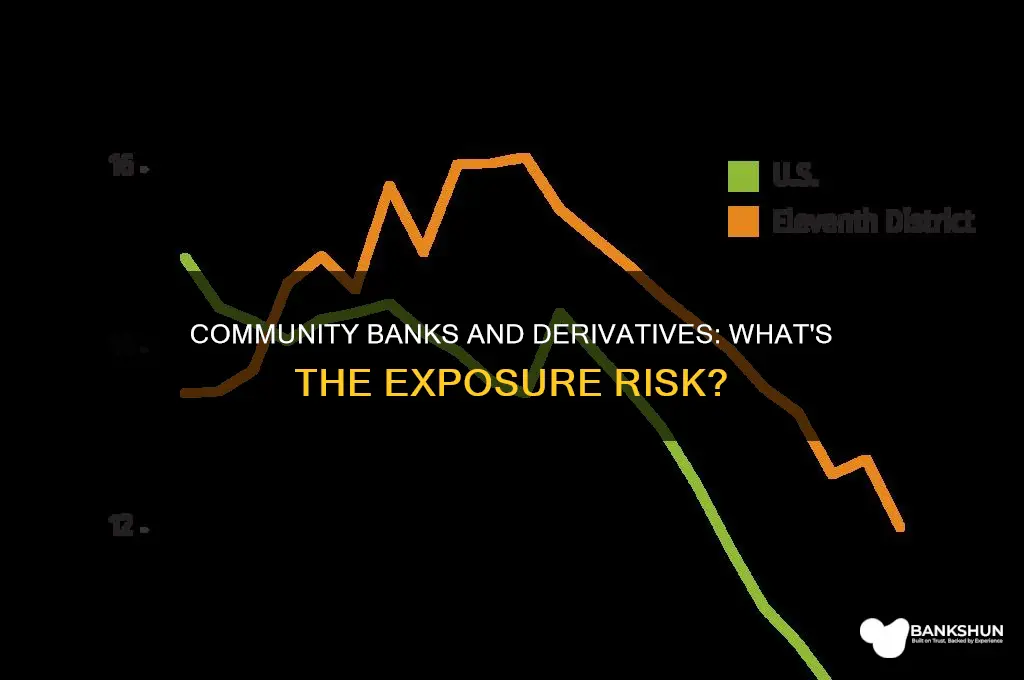

The use of derivatives by banks has grown dramatically, with the notional value of all derivatives contracts used by US commercial banks reaching almost $33 trillion in 1998, a 178% increase over five years. However, only about 5% of banks are involved in the derivatives market, and there is a stark difference between large and small banks in this respect. While large banks held 83-87% of the total banking industry's notional amount of derivatives, small community banks, for the most part, do not participate in this market. This is due to various factors, including the cost of participating in the derivatives market, which smaller banks often cannot justify. Additionally, community banks have access to alternative risk management tools, such as the Standardized Approach for Counterparty Credit Risk (SA-CCR), which helps them manage credit risk exposure without relying heavily on derivatives.

| Characteristics | Values |

|---|---|

| Percentage of banks involved in the market for derivatives | 5% |

| Dramatic increase in the use of derivatives by banks | 178% increase from 1993 to 1998 |

| Notional value of all derivatives contracts used by U.S. commercial banks in 1998 | $33 trillion |

| Holding companies that held $277.57 trillion in derivatives | JPMorgan Chase, Bank of America, Goldman Sachs Group, Morgan Stanley, Citigroup |

| Number of federally-insured commercial banks and savings associations in the U.S. | 8,249 |

| Percentage of all derivatives at 4,600 banks held by five Wall Street banks | 83% |

| Total amount of derivatives held by five Wall Street banks | $223 trillion |

| Net current credit exposure increase in the third quarter of 2023 | $35.0 billion |

| Total net current credit exposure in the third quarter of 2023 | $308.0 billion |

| Total derivative notional amounts in the third quarter of 2023 | $204.2 trillion |

| Percentage of total derivative notional amounts that are interest rate products | 71.4% |

Explore related products

$69

What You'll Learn

- Why do small community banks avoid derivatives?

- How do small community banks manage risk without derivatives?

- What are the regulatory requirements for small community banks regarding derivatives?

- How do small community banks benefit from association with bank-holding companies?

- What are the implications of higher capital requirements for small community banks?

![]()

Why do small community banks avoid derivatives?

Small community banks avoid derivatives due to a variety of factors. Firstly, the use of derivatives is closely associated with riskier capital structures, including more notes and debentures and less equity capital. This implies that smaller banks may not have the financial capacity to engage in derivatives without putting themselves in a precarious position.

Secondly, the cost of participating in the derivatives market is often unjustifiable for small banks. They lack the scale and scope of activities to offset the expenditure required to manage a derivatives program effectively. This is further compounded by the fact that derivatives are classified as off-balance-sheet activities (OBSAs), which means their explosive growth may not be accurately reflected in the bank's balance sheets, potentially leading to unforeseen complications.

Additionally, small community banks often benefit from being associated with bank-holding companies. These companies provide resources and support that enable smaller banks to participate in the derivatives market. However, not all small banks are part of such holding companies, and those that are independent may find it more challenging to justify derivative engagements.

The concentration of derivatives is also a factor. A small number of Wall Street mega banks hold a significant portion of all derivatives, with five bank-holding companies holding up to 95% of all derivatives in US banks as of 2009. This concentration of power and influence in a few large institutions can make it challenging for small community banks to compete or even consider entering the derivatives market.

Lastly, the regulatory environment and public perception play a role. The backlash against proposed capital rule increases by Wall Street mega banks, as seen in the Dodd-Frank financial reform legislation of 2010, indicates a potential shift in how derivatives are viewed and regulated. Small community banks may want to avoid the negative publicity and potential regulatory scrutiny that comes with engaging in derivatives.

Lady Banks Roses: Trellis or No Trellis?

You may want to see also

Explore related products

![]()

How do small community banks manage risk without derivatives?

Small community banks are considered to be in a different industry than big banks, with the most evident difference being their use of derivatives. Currently, only about 5% of banks are involved in the market for derivatives, and these are largely the largest banks. Small community banks tend not to use derivatives due to the cost of participating in the market.

Small community banks can manage risk without derivatives by focusing on their relationships with customers. Local decision-making and strong relationships with customers are hallmarks of small community banks, and these can help them to grow a healthy institution. Community banks can also benefit from being associated with bank-holding companies, which can provide corporate-level resources and enable them to be more likely to use derivatives.

To manage credit risk, small community banks can diversify their investments and loans. By loaning money to people with good credit histories, transacting with high-quality counterparties, and owning collateral to back up the loans, they can lower their exposure to credit risk. They can also reduce market risk by diversifying their investments and hedging them with other, inversely related investments.

To manage operational risk, small community banks should invest in cybersecurity to protect against fraud and the loss of customer information and money. They should also ensure compliance with government regulations to manage risk and protect depositors. Effective technology can also help small community banks to grow their portfolio without necessarily adding staff.

How Do Banks' Earnings Affect Their Tax Payments?

You may want to see also

Explore related products

$49.95 $88

![Financial Risk Management Modeling [AI]: Identifying, Assessing, and Mitigating Uncertainty for Stability and Success](https://m.media-amazon.com/images/I/71KDGR-XHdL._AC_UY218_.jpg)

$9.99 $24.99

![]()

What are the regulatory requirements for small community banks regarding derivatives?

Small community banks are generally considered to be in a different industry than big banks, particularly when it comes to their use of derivatives. Only about 5% of banks are involved in the market for derivatives, and smaller banks often cannot justify the cost of participating in this market.

The Commodity Futures Trading Commission (CFTC) is the primary regulator of the derivatives markets in the US, while the Securities Exchange Commission (SEC) regulates the security-based derivatives markets. The CFTC and SEC have issued key regulations that impact swaps and security-based derivatives and the markets in which they are traded. For example, the De Minimis Exception to the Swap Dealer Definition amends the definition of "swap dealer" by setting an $8 billion threshold for swap dealing activity over 12 months.

The Federal Reserve has proposed amendments to simplify regulatory capital requirements for community banks, giving them the option to calculate a simple leverage ratio. The Standardized Approach for Calculating the Exposure Amount of Derivative Contracts (SA-CCR) is a voluntary methodology that community banks can use to calculate the exposure amount of derivative contracts. The SA-CCR is intended to help community banks understand and manage counterparty credit risk.

Additionally, the Interagency Supervisory Guidance on Counterparty Credit Risk Management outlines practices for an effective counterparty credit risk management framework, and the Regulatory Capital Treatment of Certain Centrally-Cleared Derivative Contracts provides guidance on the treatment of cleared derivatives.

Bank Shots: Halo 3's Uncommon Skill

You may want to see also

Explore related products

![]()

How do small community banks benefit from association with bank-holding companies?

Small community banks are considered to be in a different industry than big banks, with the difference being evident in their use of derivatives. Only about 5% of banks are involved in the market for derivatives, and small banks often cannot justify the cost of participating in this market. However, small banks that are part of a bank-holding company (BHC) are more likely to be users of derivatives as they can benefit from corporate-level resources.

Most banks in the US are owned by BHCs, with about 80% of commercial banks being part of a BHC structure. This percentage is even higher for small banks, with over 75% of small banks with assets of less than $100 million being owned by BHCs. Small BHCs have certain advantages, such as being exempt from consolidated BHC capital guidelines and having less burdensome regulatory reporting requirements. They also have structural flexibility, which can be advantageous for merging with or acquiring additional banks. Additionally, BHCs can provide tax advantages through filing consolidated tax returns.

Small community banks that are part of a BHC can benefit from increased access to resources and reduced costs associated with being part of a larger organization. They can also take advantage of the structural flexibility and tax advantages that BHCs offer. By being part of a BHC, small community banks may be able to participate in the derivatives market, which could provide them with additional financial opportunities.

Overall, small community banks can benefit from association with bank-holding companies through increased resources, structural flexibility, tax advantages, and potential access to the derivatives market. These benefits can help small community banks better serve their customers and compete with larger financial institutions.

Why Banks Provide 1098 Forms and Who Needs Them

You may want to see also

Explore related products

![]()

What are the implications of higher capital requirements for small community banks?

Higher capital requirements for small community banks could have a range of implications, depending on the specific context and the nature of the requirements. Here are some potential consequences:

Impact on Profitability: Higher capital requirements may affect the profitability of small community banks. Meeting these requirements could result in increased costs for these banks, as they may need to hold more capital relative to their assets. This could reduce their return on equity and make it challenging to compete with larger banks that have easier access to diverse funding sources and economies of scale.

Limited Growth and Lending Capacity: Small community banks might face constraints on their growth and lending capacity. If they are required to maintain higher levels of capital, they may have less funds available for lending, which is a primary source of revenue for community banks. This could slow down their growth and potentially limit their ability to expand their customer base or enter new markets.

Risk Management and Stability: Increased capital requirements can contribute to the overall stability of small community banks by providing a larger buffer against potential losses. Higher capital levels can enhance their resilience during economic downturns or unexpected events. This stability can also positively impact their credit ratings and attract more deposits from customers seeking safer financial institutions.

Competitiveness and Market Share: The implications of higher capital requirements could extend to the competitive landscape of the banking industry. Small community banks might find it more challenging to compete with larger institutions that have easier access to diverse funding sources and can offer a wider range of financial products. This could potentially lead to a consolidation in the industry, with larger banks acquiring smaller ones or smaller banks merging to gain economies of scale.

Impact on Local Communities: Small community banks often serve local communities and small businesses, filling a vital role in the local economy. Higher capital requirements might influence their lending decisions and strategies, potentially affecting the availability of credit for local businesses and individuals. This could have a ripple effect on the economic development and growth of the communities they serve.

It is important to note that the impact of higher capital requirements on small community banks should also consider the regulatory environment, the specific details of the requirements, and the individual characteristics of these banks. Striking the right balance between ensuring financial stability and promoting healthy competition in the banking sector is crucial for policymakers and regulators.

Julie Bowen and Elizabeth Banks: Are They Related?

You may want to see also

Frequently asked questions

Small community banks generally have less exposure to derivatives than larger banks. Only about 5% of banks are involved in the market for derivatives, and smaller banks often cannot justify the cost of participating in this market.

Smaller banks have less exposure to derivatives because they often lack the scale and scope of activities necessary to justify the expenditure of resources to manage a derivatives program.

Banks use the Standardized Approach for Counterparty Credit Risk (SA-CCR) to calculate their exposure amount. This approach is available for use by community banks on a voluntary basis.

As of 2024, five Wall Street banks (JPMorgan Chase, Bank of America, Goldman Sachs Group, Morgan Stanley, and Citigroup) held $223 trillion in derivatives, or 83% of all derivatives at 4,600 banks.

The use of derivatives by banks has grown dramatically, with a 178% increase in the total notional value of derivatives contracts used by U.S. commercial banks between 1993 and 1998. However, this growth has not been uniform across all banks, with smaller community banks less likely to use derivatives.