The phrase how do shoes New Balance show in bank appears to be a mix of unrelated concepts, as New Balance shoes are a popular athletic footwear brand, while banks typically deal with financial transactions and accounts. It’s unclear whether the question refers to purchasing New Balance shoes using banking services, tracking such purchases in bank statements, or if there’s a specific context like a bank’s marketing partnership with New Balance. To clarify, New Balance shoes would typically appear in a bank statement as a debit or credit transaction under the retailer’s name (e.g., New Balance Store or Amazon) if purchased online or in-store, reflecting the amount spent. If the question pertains to a different scenario, further details would be needed for a precise explanation.

Explore related products

What You'll Learn

- New Balance Purchase Alerts: Banks notify customers of New Balance shoe transactions via SMS or email

- Shoe Brand Spending Tracking: Monitor New Balance purchases through bank statements or budgeting tools

- Fraud Detection for Shoes: Banks flag suspicious New Balance transactions to protect accounts

- Rewards for Shoe Purchases: Earn cashback or points on New Balance buys with bank rewards

- Installment Plans for Shoes: Banks offer payment plans for high-cost New Balance shoe purchases

![]()

New Balance Purchase Alerts: Banks notify customers of New Balance shoe transactions via SMS or email

In today's digital age, banks have implemented sophisticated systems to monitor and notify customers of their transactions, including purchases from popular brands like New Balance. When you make a purchase of New Balance shoes using your debit or credit card, your bank's transaction monitoring system flags the activity, specifically identifying the merchant category code (MCC) associated with New Balance or its authorized retailers. This triggers the bank's notification system to send you an alert, either via SMS or email, informing you of the transaction. The alert typically includes details such as the transaction amount, the merchant's name (e.g., New Balance or a specific retailer), and the time of purchase. This real-time notification helps you stay informed about your spending and quickly detect any unauthorized or suspicious activities related to your New Balance shoe purchases.

The process of receiving New Balance purchase alerts begins with the bank's integration of payment networks, which categorize transactions based on the merchant's MCC. For New Balance, the MCC falls under the footwear or retail category, allowing the bank's system to specifically identify and flag these transactions. Once a New Balance shoe purchase is detected, the bank's notification system generates a personalized alert tailored to your preferred communication channel, whether SMS or email. This alert is designed to be immediate, ensuring you receive the information within seconds or minutes of the transaction. By providing this timely notification, banks empower customers to take prompt action if they notice any discrepancies or unauthorized charges related to their New Balance purchases.

To ensure the effectiveness of New Balance purchase alerts, banks often allow customers to customize their notification preferences. You can typically choose the types of transactions you want to be notified about, including purchases from specific brands like New Balance. Additionally, you can select the frequency of alerts, such as receiving notifications for every transaction or only for purchases above a certain threshold. Some banks also offer the option to set up alerts for specific categories, like footwear or retail, ensuring you receive notifications for all New Balance shoe purchases. By tailoring these settings, you can optimize the alert system to suit your needs and enhance your overall banking experience when purchasing New Balance products.

It's essential to note that New Balance purchase alerts serve not only as a convenience but also as a security feature. By promptly notifying you of transactions, banks enable you to quickly identify and report any unauthorized purchases, potentially minimizing financial loss and preventing fraud. For instance, if you receive an alert for a New Balance shoe purchase you didn't make, you can immediately contact your bank to dispute the transaction and secure your account. Furthermore, these alerts contribute to better financial management by providing a real-time overview of your spending habits, helping you track expenses related to New Balance shoes and other purchases. As a result, staying informed about your New Balance transactions through bank alerts is a valuable tool for both security and financial planning.

Lastly, to make the most of New Balance purchase alerts, it's crucial to keep your contact information updated with your bank. Ensure your mobile number and email address are accurate and active, as these are the primary channels through which alerts are sent. Regularly reviewing your alert settings and adjusting them according to your preferences can also enhance the effectiveness of this feature. By staying proactive and engaged with your bank's notification system, you can enjoy a seamless and secure experience when purchasing New Balance shoes, knowing that you'll be promptly informed of every transaction. This level of transparency and control not only builds trust in your banking relationship but also reinforces the convenience of shopping for your favorite New Balance products.

Does the West Bank Belong to Jordan? Historical and Legal Analysis

You may want to see also

Explore related products

![]()

Shoe Brand Spending Tracking: Monitor New Balance purchases through bank statements or budgeting tools

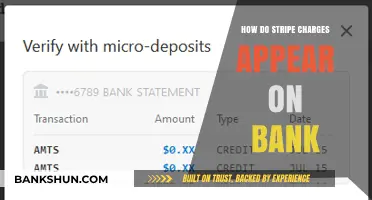

Tracking your spending on New Balance shoes can be a crucial part of managing your personal finances, especially if you're an enthusiast or frequent buyer of the brand. One effective way to monitor these purchases is by scrutinizing your bank statements or utilizing budgeting tools. When you buy New Balance shoes, the transaction will typically appear on your bank statement with a descriptor that includes the brand name or the retailer from which you made the purchase. For instance, if you bought directly from the New Balance website, the charge might show up as "NEW BALANCE" or "NB WEB PURCHASE." If you purchased from a retailer like Foot Locker or a department store, the retailer's name will likely appear instead, though you can cross-reference the amount and date to identify the purchase.

To begin tracking New Balance purchases through bank statements, log in to your online banking account and navigate to the transaction history section. Use the search or filter function to look for keywords like "New Balance," "NB," or the names of common retailers where New Balance shoes are sold. Make a note of each transaction, including the date, amount, and retailer, to create a comprehensive record of your spending. If your bank allows, you can also download your transaction history into a spreadsheet for easier analysis. Highlight or categorize these entries specifically as "New Balance" purchases to distinguish them from other expenses.

Budgeting tools can further streamline the process of monitoring New Balance spending. Apps like Mint, YNAB (You Need A Budget), or Excel spreadsheets can be configured to categorize transactions automatically. In these tools, set up a specific category for "New Balance" or "Footwear" and link it to your bank account. Most budgeting apps allow you to manually tag transactions or use rules to categorize them based on keywords. For example, you can create a rule that any transaction containing "New Balance" or "NB" is automatically assigned to the "New Balance" category. This way, you can generate reports or view charts that show how much you’re spending on New Balance shoes over time.

Another useful feature of budgeting tools is the ability to set spending limits or alerts. If you’re trying to curb your New Balance spending, you can set a monthly or annual budget for this category and receive notifications when you’re approaching or exceeding the limit. This proactive approach helps you stay accountable and make informed decisions about future purchases. Additionally, some apps offer insights into spending trends, allowing you to identify patterns, such as whether your New Balance purchases spike during sales or certain seasons.

For those who prefer a more hands-on approach, maintaining a dedicated notebook or digital document for tracking New Balance purchases can be effective. Each time you make a purchase, jot down the details, including the date, amount, retailer, and specific shoe model if possible. This method, while manual, ensures you have a clear and personalized record of your spending. Combining this with periodic reviews of your bank statements or budgeting tool data can provide a comprehensive overview of your New Balance expenditures.

In conclusion, monitoring New Balance purchases through bank statements or budgeting tools is a practical way to stay on top of your spending. Whether you rely on manual tracking, automated categorization, or a combination of both, the key is consistency. By regularly reviewing and analyzing your transactions, you can make more mindful purchasing decisions and ensure that your spending aligns with your financial goals. With the right tools and habits, tracking your New Balance expenditures becomes a seamless part of your overall financial management strategy.

Marshall's Vote: The Impact on Import-Export Bank

You may want to see also

Explore related products

![]()

Fraud Detection for Shoes: Banks flag suspicious New Balance transactions to protect accounts

In the realm of fraud detection, banks are increasingly employing sophisticated algorithms and monitoring systems to identify suspicious transactions, including those related to popular shoe brands like New Balance. When a customer purchases New Balance shoes, the transaction typically appears on their bank statement with a descriptive label, such as "New Balance Store" or "NB Online Purchase." However, fraudsters often exploit this familiarity to disguise unauthorized transactions. To combat this, banks analyze spending patterns, transaction amounts, and merchant categories to flag anomalies. For instance, a sudden high-value purchase from a New Balance outlet in a location where the account holder has no known connection can trigger an alert. This proactive approach ensures that potential fraud is detected early, safeguarding customers' accounts.

Banks utilize machine learning models to enhance their fraud detection capabilities, particularly for transactions involving well-known brands like New Balance. These models learn from historical data to identify unusual behavior, such as multiple purchases from different New Balance stores within a short timeframe or transactions occurring in geographically distant locations. When such patterns emerge, the bank’s system automatically flags the activity for further review. Account holders are then notified via text, email, or in-app alerts to verify the legitimacy of the transaction. This real-time monitoring not only protects customers but also helps banks maintain trust and reduce financial losses associated with fraudulent activities.

Another critical aspect of fraud detection for New Balance transactions is the collaboration between banks and merchants. Banks often work with New Balance and payment processors to share data on known fraud schemes, such as stolen credit card information being used for bulk purchases of shoes. By cross-referencing this data with their own transaction records, banks can more accurately identify and block fraudulent activities. Additionally, banks may implement velocity checks, which monitor the frequency and volume of purchases from specific merchants like New Balance. If an account exhibits unusual buying behavior, such as purchasing multiple pairs of shoes in rapid succession, the bank can temporarily freeze the account or request additional verification from the customer.

Customer education plays a vital role in complementing banks' fraud detection efforts for New Balance transactions. Banks often advise account holders to regularly review their statements and report any unrecognized charges immediately. They also encourage customers to enable transaction alerts and use secure payment methods, such as virtual credit cards or tokenized payments, when shopping for New Balance shoes online. By empowering customers to take an active role in monitoring their accounts, banks create an additional layer of defense against fraud. This collaborative approach between banks and customers is essential in staying ahead of increasingly sophisticated fraud tactics.

Finally, banks continuously update their fraud detection systems to address emerging threats related to New Balance transactions and other retail purchases. As fraudsters adapt their methods, banks must evolve their algorithms to detect new patterns of suspicious activity. For example, the rise of "buy now, pay later" schemes has introduced additional risks, as fraudsters may use stolen identities to purchase high-value items like New Balance shoes without immediate payment. Banks respond by integrating more comprehensive data sources, such as social media activity and device fingerprinting, into their fraud detection models. This holistic approach ensures that even the most cunning fraud attempts are identified and thwarted, protecting both customers and financial institutions alike.

Hands Off My Daughter, Jonathan Banks: A Father's Fierce Warning

You may want to see also

Explore related products

![]()

Rewards for Shoe Purchases: Earn cashback or points on New Balance buys with bank rewards

When it comes to maximizing your spending on New Balance shoes, leveraging bank rewards programs can be a game-changer. Many banks offer cashback or points-based rewards systems that can significantly offset the cost of your purchases. To start, check with your bank to see if they have partnerships with New Balance or if they offer general rewards for shopping at sporting goods stores or online retailers. For instance, some banks provide higher cashback rates for purchases made at specific categories, including footwear or athletic gear. By using your bank’s credit or debit card for New Balance buys, you can automatically earn rewards without any additional effort.

Another way to earn rewards on New Balance purchases is by utilizing bank-specific shopping portals. Many banks have online platforms where you can shop at partner retailers, including New Balance, and earn extra cashback or points. For example, if your bank has a shopping portal, log in and search for New Balance. You might find offers like "Earn 5% cashback on all New Balance purchases" or "Get 3x points per dollar spent." These portals often require you to click through their link before making a purchase to activate the rewards, so ensure you follow the instructions carefully to maximize your earnings.

If you’re a frequent New Balance shopper, consider applying for a bank credit card that offers enhanced rewards on retail or athletic wear purchases. Some cards provide introductory bonuses or higher reward rates for specific categories, which can include New Balance buys. For instance, a card might offer 6% cashback on department store purchases, which could include New Balance if bought through a partnered retailer. Additionally, certain credit cards have rotating categories where New Balance purchases might qualify for elevated rewards during specific quarters. Always review the terms and conditions to ensure your purchases align with the reward criteria.

To further optimize your rewards, stack bank offers with New Balance promotions or discounts. For example, if New Balance is offering a sitewide sale or free shipping, use your bank’s rewards card to pay and earn cashback or points on the discounted price. Some banks also allow you to combine rewards with coupon codes or cashback apps, though this varies by institution. By layering these savings, you can get the most value out of your New Balance purchases while earning rewards that can be redeemed for statement credits, gift cards, or travel.

Lastly, keep track of your rewards and redemption options to make the most of your New Balance purchases. Most banks provide a dashboard where you can monitor your cashback or points balance. Set reminders to redeem your rewards regularly, as some programs have expiration dates or caps on earnings. Additionally, consider using your accumulated points or cashback to offset future New Balance purchases, creating a cycle of savings. By strategically using bank rewards, you can turn your love for New Balance shoes into a rewarding financial habit.

Master Mobile Banking: A Step-by-Step Setup Guide for Beginners

You may want to see also

Explore related products

![]()

Installment Plans for Shoes: Banks offer payment plans for high-cost New Balance shoe purchases

When it comes to purchasing high-end New Balance shoes, the cost can sometimes be a barrier for buyers. However, many banks have recognized this challenge and now offer installment plans specifically tailored for such purchases. These plans allow customers to spread the cost of their New Balance shoes over several months, making it more manageable and budget-friendly. By partnering with retailers or offering credit card installment options, banks enable shoe enthusiasts to own their desired pairs without the burden of paying the full amount upfront.

To take advantage of these installment plans, customers typically need to meet certain eligibility criteria set by the bank. This may include having a good credit score, a stable income, and an existing account with the bank. Once approved, buyers can select the installment plan that best suits their financial situation, often choosing between different repayment periods and interest rates. Some banks even offer promotional periods with zero or low interest, making the deal even more attractive for New Balance shoe purchases.

The process of applying for an installment plan is usually straightforward. Customers can either apply directly through their bank’s website, mobile app, or by visiting a branch. Alternatively, some shoe retailers have integrated bank installment options into their checkout process, allowing buyers to select the plan during purchase. It’s important for customers to read the terms and conditions carefully, understanding any fees, interest rates, and repayment schedules associated with the plan to avoid unexpected costs.

One of the key benefits of using a bank installment plan for New Balance shoes is the flexibility it provides. Instead of depleting savings or relying on high-interest credit cards, buyers can enjoy their new shoes while making smaller, predictable payments over time. This approach not only makes luxury footwear more accessible but also helps customers maintain financial stability. Additionally, timely repayments can positively impact a buyer’s credit score, further enhancing their financial health.

For banks, offering installment plans for high-cost items like New Balance shoes is a strategic move to attract and retain customers. It positions them as customer-centric institutions that understand and cater to modern spending habits. Moreover, these plans often encourage higher-value purchases, benefiting both the bank and the retailer. As the demand for premium footwear continues to rise, such financial solutions are likely to become even more prevalent, bridging the gap between desire and affordability for shoe enthusiasts.

In conclusion, installment plans offered by banks for New Balance shoe purchases provide a practical and flexible solution for buyers. By breaking down the cost into manageable payments, these plans make high-end footwear more accessible without straining finances. Whether applied for through a bank or directly at the point of sale, these options empower customers to invest in quality shoes while maintaining financial control. As this trend grows, it’s clear that banks and retailers are working together to meet the evolving needs of consumers in the footwear market.

Does US Bank Offer High Yield Savings Accounts? A Review

You may want to see also

Frequently asked questions

New Balance shoe purchases typically appear on your bank statement as "New Balance," "NB Store," or the name of the retailer where the purchase was made, followed by the transaction amount.

No, bank statements usually do not specify the shoe model. They only display the merchant name and transaction details like date, time, and amount.

Yes, online New Balance purchases often appear as "NewBalance.com" or "NB Online" on your bank statement, depending on the payment processor used.

If the purchase doesn’t appear, check if the transaction is pending or contact your bank. It may take 1-3 business days for the charge to reflect on your statement.